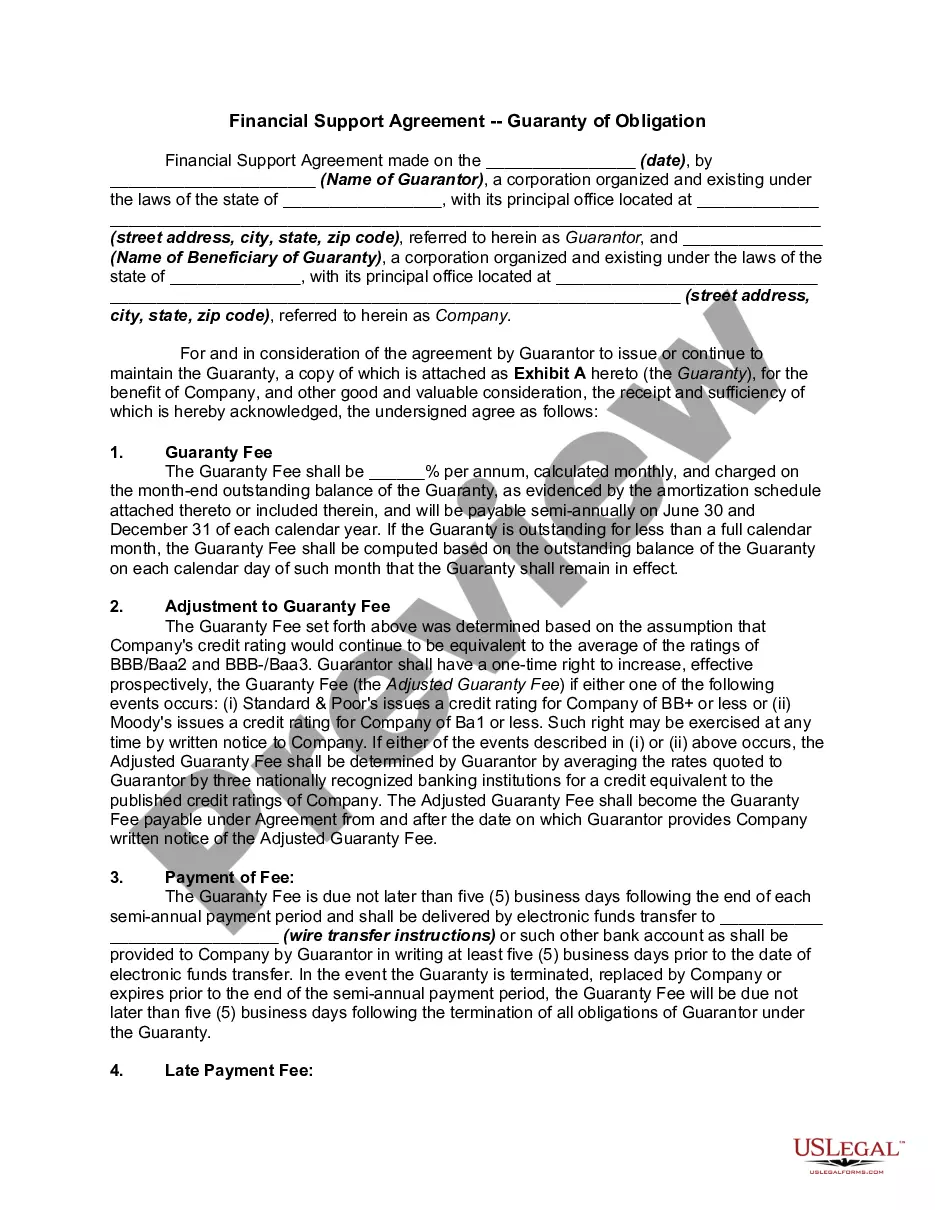

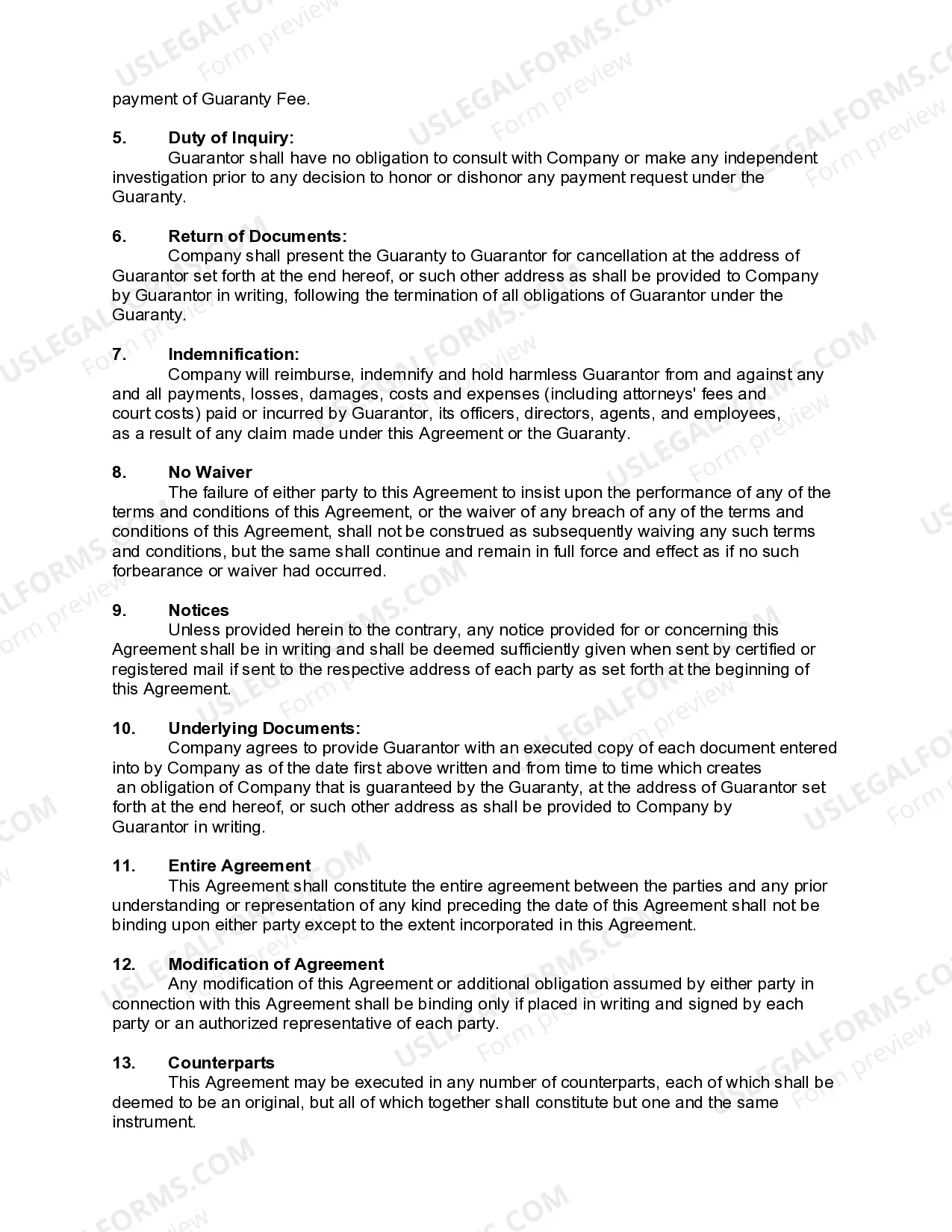

In this agreement, one corporation (the Guarantor) is providing financial assistance to another Corporation (the Corporation) by guaranteeing certain indebtedness for the Company in exchange for a guaranty fee.

This form is a generic example that may be referred to when preparing such a form for your particular state. It is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a form in a particular jurisdiction.

Hawaii Financial Support Agreement — Guaranty of Obligation is a legally binding document that outlines the terms and conditions for providing financial support to individuals or businesses in Hawaii. This agreement serves as a guarantee for the repayment of debts or obligations undertaken by the borrower. It is essential in situations where the borrower's ability to meet their obligations might be in question, ensuring the lender's interests are adequately protected. The Hawaii Financial Support Agreement — Guaranty of Obligation establishes a clear relationship between the lender (often a financial institution or creditor) and the guarantor (an individual or entity assuming responsibility for the debt repayment). By signing this agreement, the guarantor agrees to fulfill the borrower's obligations if they default on their financial commitments. This arrangement provides an additional level of security to the lender and encourages them to offer financial support to borrowers who may not have a strong credit history or adequate collateral. There are several types of Hawaii Financial Support Agreement — Guaranty of Obligation, each designed to suit specific circumstances. These may include: 1. Individual Guaranty: This agreement involves a single person acting as the guarantor on behalf of the borrower. The guarantor's personal assets may be used as collateral to secure the loan, and they will be solely responsible for fulfilling the obligations if the borrower defaults. 2. Corporate Guaranty: In cases where the borrower is a business entity, a corporate guaranty may be required. This agreement involves the corporation assuming the responsibilities and obligations of the borrower, providing an additional layer of assurance to the lender. 3. Limited Guaranty: A limited guaranty specifies the extent to which the guarantor will be liable for the borrower's obligations. It may restrict the guarantor's liability to a certain amount or a specific timeframe, providing a degree of protection against unlimited liability. 4. Continuing Guaranty: This type of agreement remains in effect until the borrower fulfills all their obligations or the guarantor revokes the guaranty. It ensures that the guarantor's liability remains intact even if the borrower enters into additional financial agreements in the future. In conclusion, the Hawaii Financial Support Agreement — Guaranty of Obligation is a critical tool for facilitating financial support in Hawaii. It establishes a legally binding agreement between the lender and guarantor, ensuring the repayment of debts in case of default. Various types of guaranties exist to accommodate different scenarios, including individual, corporate, limited, and continuing guaranties. These agreements provide vital protection and reassurance for lenders while enabling borrowers to access the financial assistance they need.Hawaii Financial Support Agreement — Guaranty of Obligation is a legally binding document that outlines the terms and conditions for providing financial support to individuals or businesses in Hawaii. This agreement serves as a guarantee for the repayment of debts or obligations undertaken by the borrower. It is essential in situations where the borrower's ability to meet their obligations might be in question, ensuring the lender's interests are adequately protected. The Hawaii Financial Support Agreement — Guaranty of Obligation establishes a clear relationship between the lender (often a financial institution or creditor) and the guarantor (an individual or entity assuming responsibility for the debt repayment). By signing this agreement, the guarantor agrees to fulfill the borrower's obligations if they default on their financial commitments. This arrangement provides an additional level of security to the lender and encourages them to offer financial support to borrowers who may not have a strong credit history or adequate collateral. There are several types of Hawaii Financial Support Agreement — Guaranty of Obligation, each designed to suit specific circumstances. These may include: 1. Individual Guaranty: This agreement involves a single person acting as the guarantor on behalf of the borrower. The guarantor's personal assets may be used as collateral to secure the loan, and they will be solely responsible for fulfilling the obligations if the borrower defaults. 2. Corporate Guaranty: In cases where the borrower is a business entity, a corporate guaranty may be required. This agreement involves the corporation assuming the responsibilities and obligations of the borrower, providing an additional layer of assurance to the lender. 3. Limited Guaranty: A limited guaranty specifies the extent to which the guarantor will be liable for the borrower's obligations. It may restrict the guarantor's liability to a certain amount or a specific timeframe, providing a degree of protection against unlimited liability. 4. Continuing Guaranty: This type of agreement remains in effect until the borrower fulfills all their obligations or the guarantor revokes the guaranty. It ensures that the guarantor's liability remains intact even if the borrower enters into additional financial agreements in the future. In conclusion, the Hawaii Financial Support Agreement — Guaranty of Obligation is a critical tool for facilitating financial support in Hawaii. It establishes a legally binding agreement between the lender and guarantor, ensuring the repayment of debts in case of default. Various types of guaranties exist to accommodate different scenarios, including individual, corporate, limited, and continuing guaranties. These agreements provide vital protection and reassurance for lenders while enabling borrowers to access the financial assistance they need.