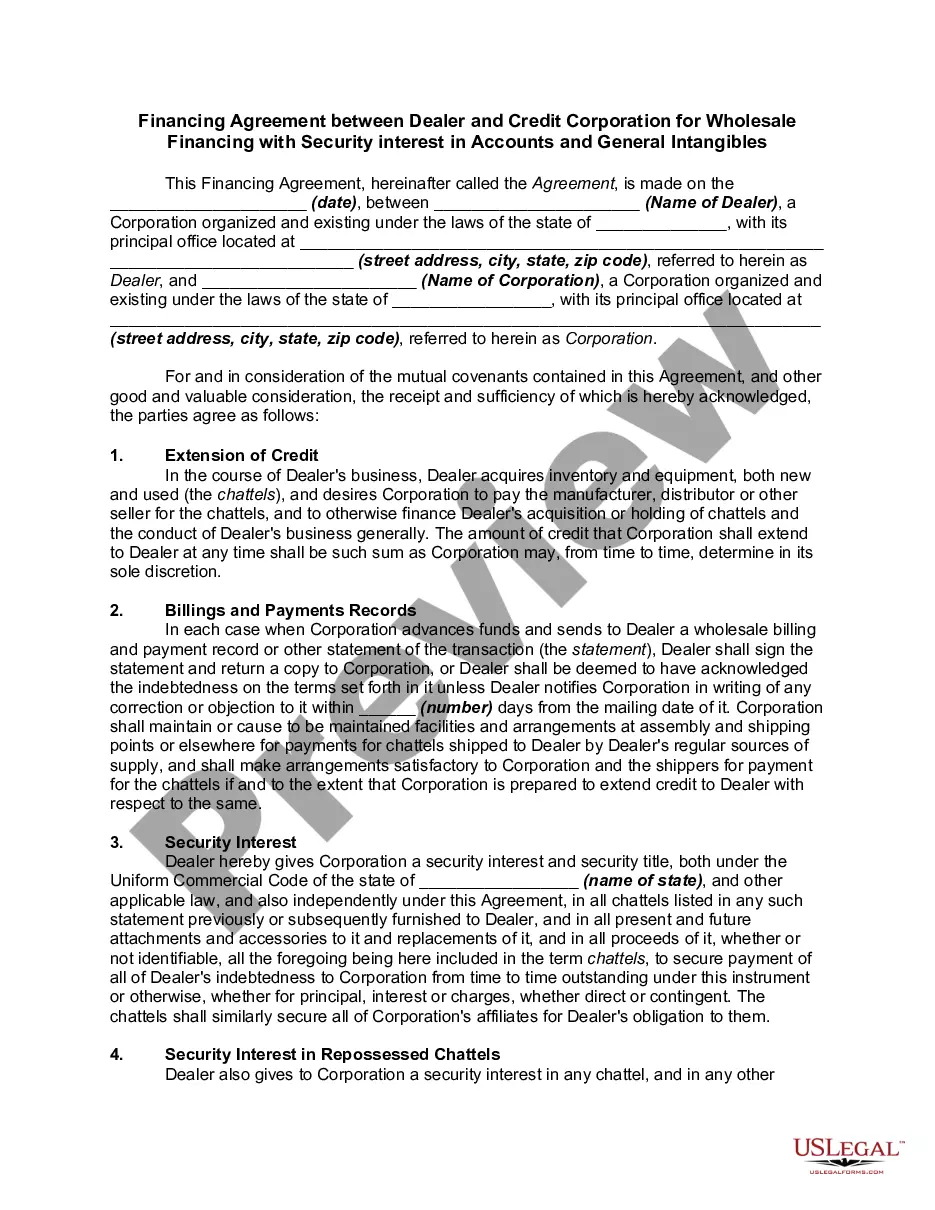

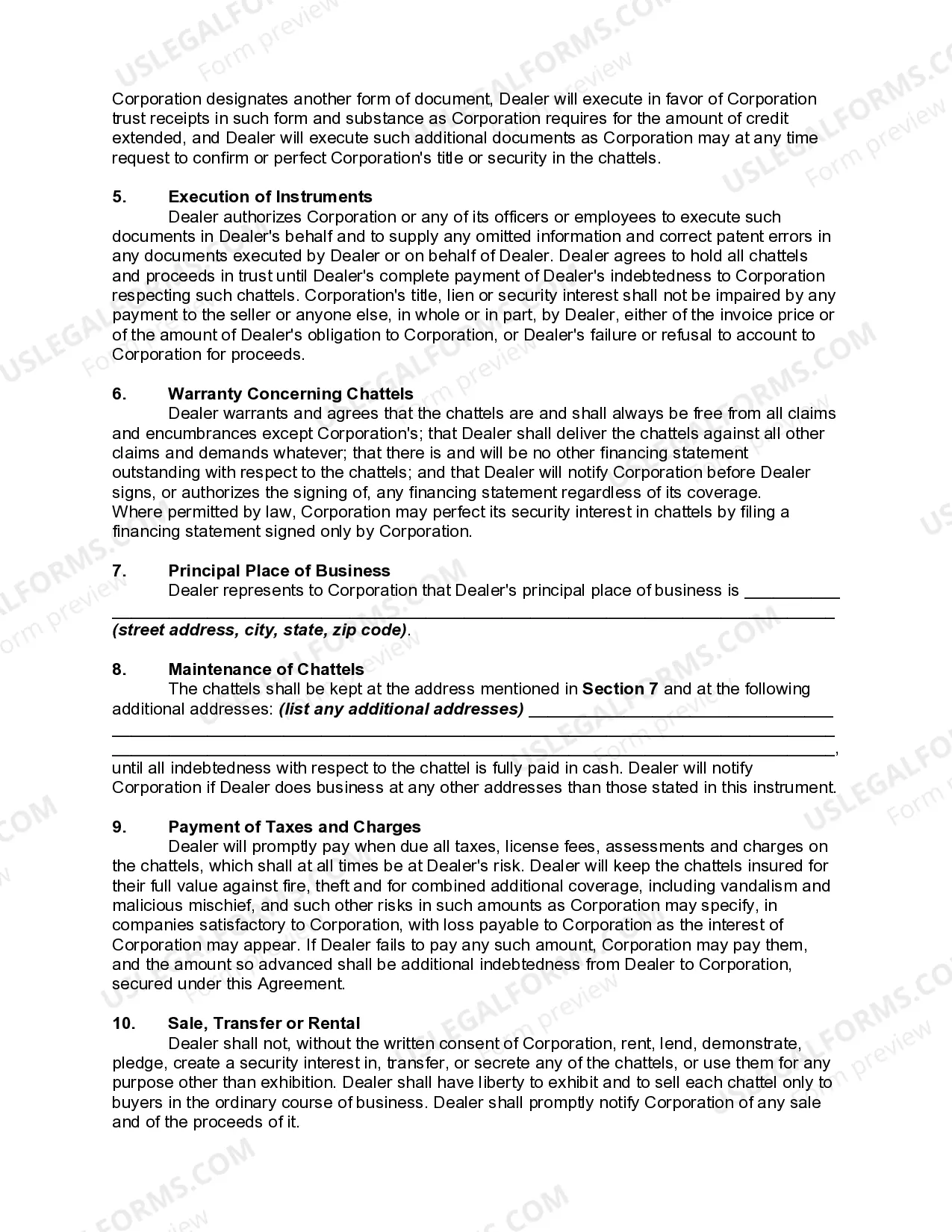

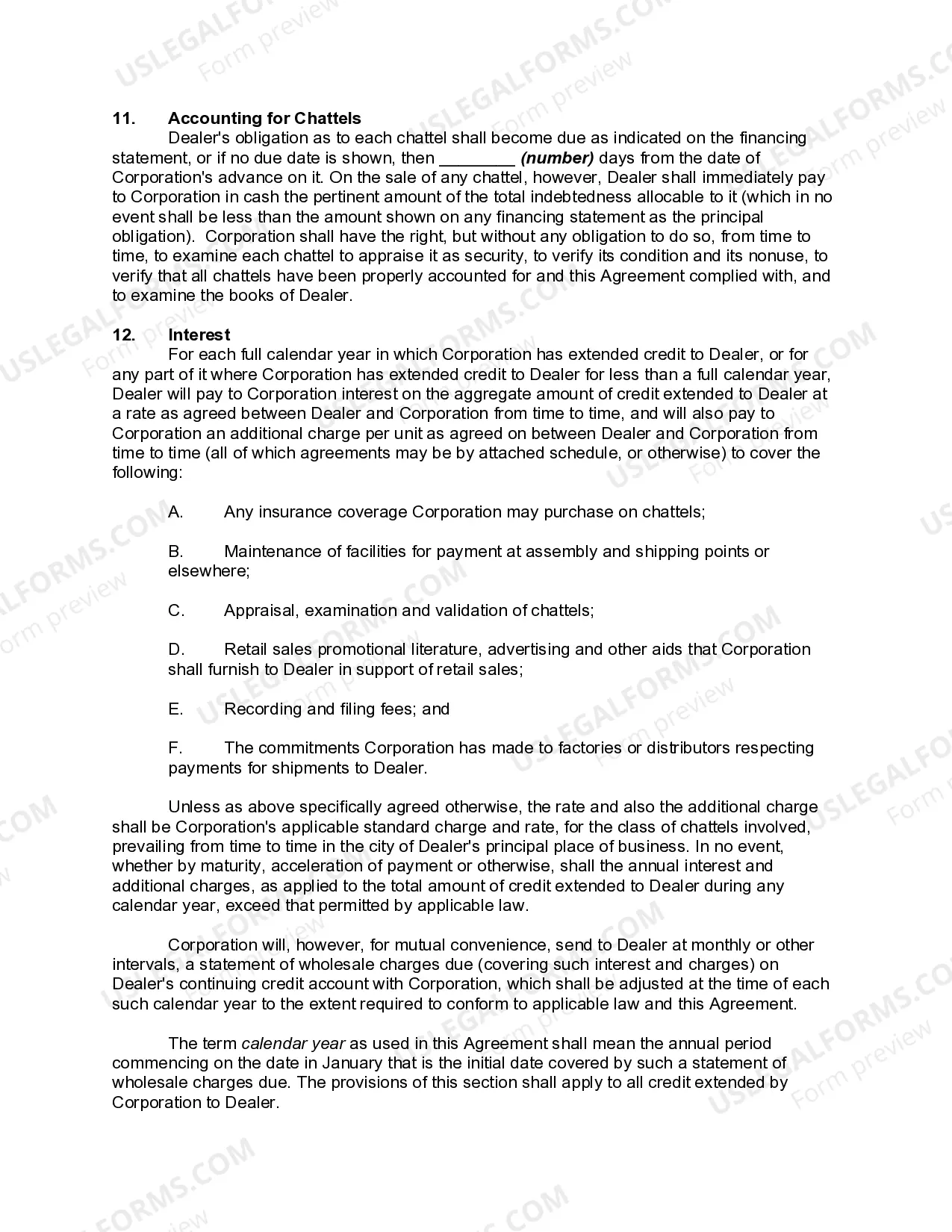

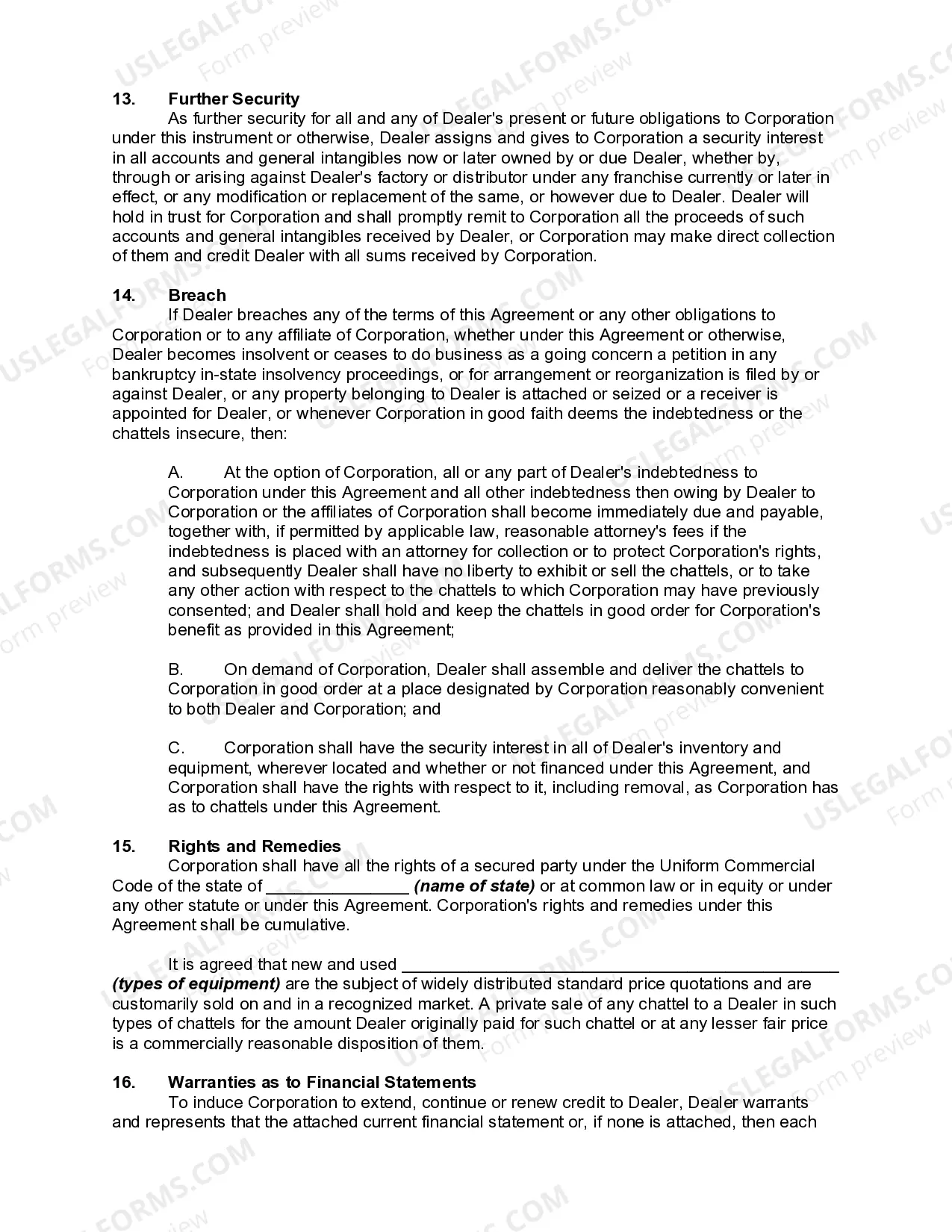

This form is a type of asset-financing arrangement in which a company uses its receivables (money owed by customers) as collateral in a financing agreement. The company receives an amount that is equal to a reduced value of the receivables pledged. The age of the receivables have a large effect on the amount a company will receive. The older the receivables, the less the company can expect.

This type of financing helps companies free up capital that is stuck in accounts receivables. Accounts receivable financing transfers the default risk associated with the accounts receivables to the financing company. This transfer of risk can help the company using the financing to shift focus from trying to collect receivables to current business activities.

This form is a generic example that may be referred to when preparing such a form for your particular state. It is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a form in a particular jurisdiction.

Title: Understanding the Hawaii Financing Agreement between Dealer and Credit Corporation for Wholesale Financing with Security Interest in Accounts and General Intangibles Introduction: The Hawaii Financing Agreement between Dealer and Credit Corporation for Wholesale Financing with Security Interest in Accounts and General Intangibles is a legal instrument that facilitates a mutually beneficial relationship between a dealer and a credit corporation. This agreement enables dealers to obtain financial support for their wholesale operations, while providing credit corporations with collateral in accounts and general intangibles. In this article, we will elaborate on the key elements and different types of financing agreements in Hawaii, using relevant keywords to offer a comprehensive understanding. Key Elements of the Hawaii Financing Agreement: 1. Wholesale Financing: The agreement involves the provision of funds by a credit corporation to a dealer engaged in wholesale activities. Wholesale financing assists in covering operational costs, inventory procurement, marketing efforts, and other expenses related to wholesale operations. 2. Dealer and Credit Corporation Relationship: The agreement establishes a formal relationship between the dealer and the credit corporation. Both parties have specific roles and responsibilities to ensure a smooth wholesale financing process and timely repayments. 3. Security Interest in Accounts: A significant aspect of this financing agreement is the provision of security interest in accounts. Credit corporations may legally claim an interest in the accounts receivable generated by the dealer. This security interest provides the necessary collateral to mitigate the credit corporation's financial risks. 4. Security Interest in General Intangibles: Alongside accounts, credit corporations may also secure their interest in general intangibles such as intellectual property rights, patents, copyrights, trademarks, and other non-physical assets that contribute to the dealer's business value. This adds another layer of protection for the credit corporation. 5. Repayment Terms: The agreement outlines the terms and conditions of repayment, including the amount borrowed, interest rates, repayment schedule, payment methods, and consequences of default on the part of the dealer. By adhering to these repayment terms, the dealer can strengthen their creditworthiness, improving future borrowing opportunities. Types of Hawaii Financing Agreements: 1. Revolving Line of Credit: This type of financing agreement allows the dealer to obtain funds as needed within a predetermined credit limit. It provides flexibility to manage varying wholesale financial requirements and pays interest only on the borrowed amount. 2. Term Loan Agreement: A term loan agreement involves a fixed loan amount issued for a specific period, either short-term or long-term. The dealer repays this loan through regular installments over an agreed-upon period. 3. Floor Planning Agreement: Floor planning agreements are commonly utilized in the automotive industry. It allows the dealer to finance their vehicle inventory specifically, offering funds for car purchases and covering holding costs until the vehicles are sold. Conclusion: The Hawaii Financing Agreement between Dealer and Credit Corporation for Wholesale Financing with Security Interest in Accounts and General Intangibles facilitates financial support to dealers and reduces the risks for credit corporations by providing security interests. Understanding the key elements and various types of this agreement can guide dealers in making informed decisions while seeking wholesale financing options. By upholding the agreement's terms and responsibilities, both parties can establish a mutually beneficial relationship that fosters long-term growth and success.Title: Understanding the Hawaii Financing Agreement between Dealer and Credit Corporation for Wholesale Financing with Security Interest in Accounts and General Intangibles Introduction: The Hawaii Financing Agreement between Dealer and Credit Corporation for Wholesale Financing with Security Interest in Accounts and General Intangibles is a legal instrument that facilitates a mutually beneficial relationship between a dealer and a credit corporation. This agreement enables dealers to obtain financial support for their wholesale operations, while providing credit corporations with collateral in accounts and general intangibles. In this article, we will elaborate on the key elements and different types of financing agreements in Hawaii, using relevant keywords to offer a comprehensive understanding. Key Elements of the Hawaii Financing Agreement: 1. Wholesale Financing: The agreement involves the provision of funds by a credit corporation to a dealer engaged in wholesale activities. Wholesale financing assists in covering operational costs, inventory procurement, marketing efforts, and other expenses related to wholesale operations. 2. Dealer and Credit Corporation Relationship: The agreement establishes a formal relationship between the dealer and the credit corporation. Both parties have specific roles and responsibilities to ensure a smooth wholesale financing process and timely repayments. 3. Security Interest in Accounts: A significant aspect of this financing agreement is the provision of security interest in accounts. Credit corporations may legally claim an interest in the accounts receivable generated by the dealer. This security interest provides the necessary collateral to mitigate the credit corporation's financial risks. 4. Security Interest in General Intangibles: Alongside accounts, credit corporations may also secure their interest in general intangibles such as intellectual property rights, patents, copyrights, trademarks, and other non-physical assets that contribute to the dealer's business value. This adds another layer of protection for the credit corporation. 5. Repayment Terms: The agreement outlines the terms and conditions of repayment, including the amount borrowed, interest rates, repayment schedule, payment methods, and consequences of default on the part of the dealer. By adhering to these repayment terms, the dealer can strengthen their creditworthiness, improving future borrowing opportunities. Types of Hawaii Financing Agreements: 1. Revolving Line of Credit: This type of financing agreement allows the dealer to obtain funds as needed within a predetermined credit limit. It provides flexibility to manage varying wholesale financial requirements and pays interest only on the borrowed amount. 2. Term Loan Agreement: A term loan agreement involves a fixed loan amount issued for a specific period, either short-term or long-term. The dealer repays this loan through regular installments over an agreed-upon period. 3. Floor Planning Agreement: Floor planning agreements are commonly utilized in the automotive industry. It allows the dealer to finance their vehicle inventory specifically, offering funds for car purchases and covering holding costs until the vehicles are sold. Conclusion: The Hawaii Financing Agreement between Dealer and Credit Corporation for Wholesale Financing with Security Interest in Accounts and General Intangibles facilitates financial support to dealers and reduces the risks for credit corporations by providing security interests. Understanding the key elements and various types of this agreement can guide dealers in making informed decisions while seeking wholesale financing options. By upholding the agreement's terms and responsibilities, both parties can establish a mutually beneficial relationship that fosters long-term growth and success.