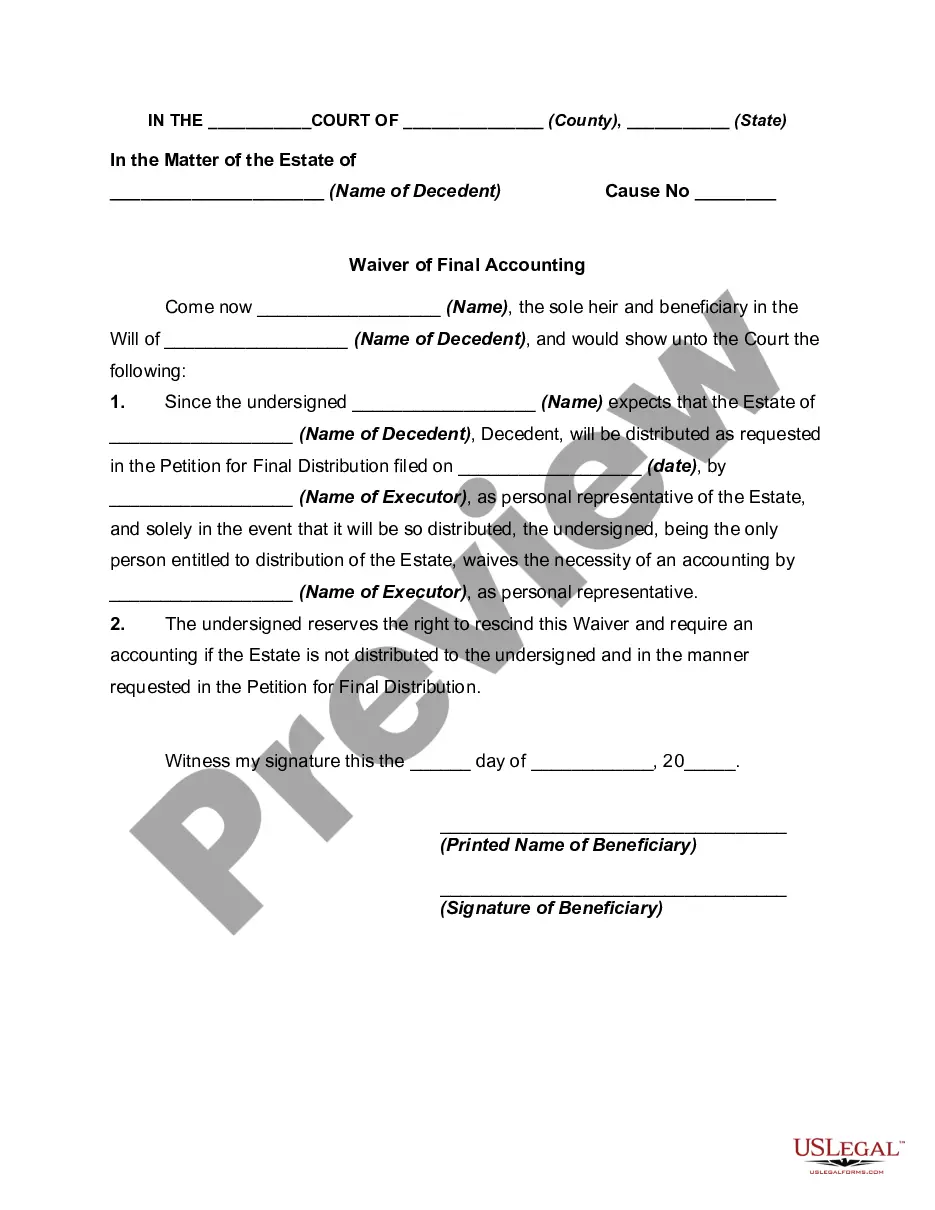

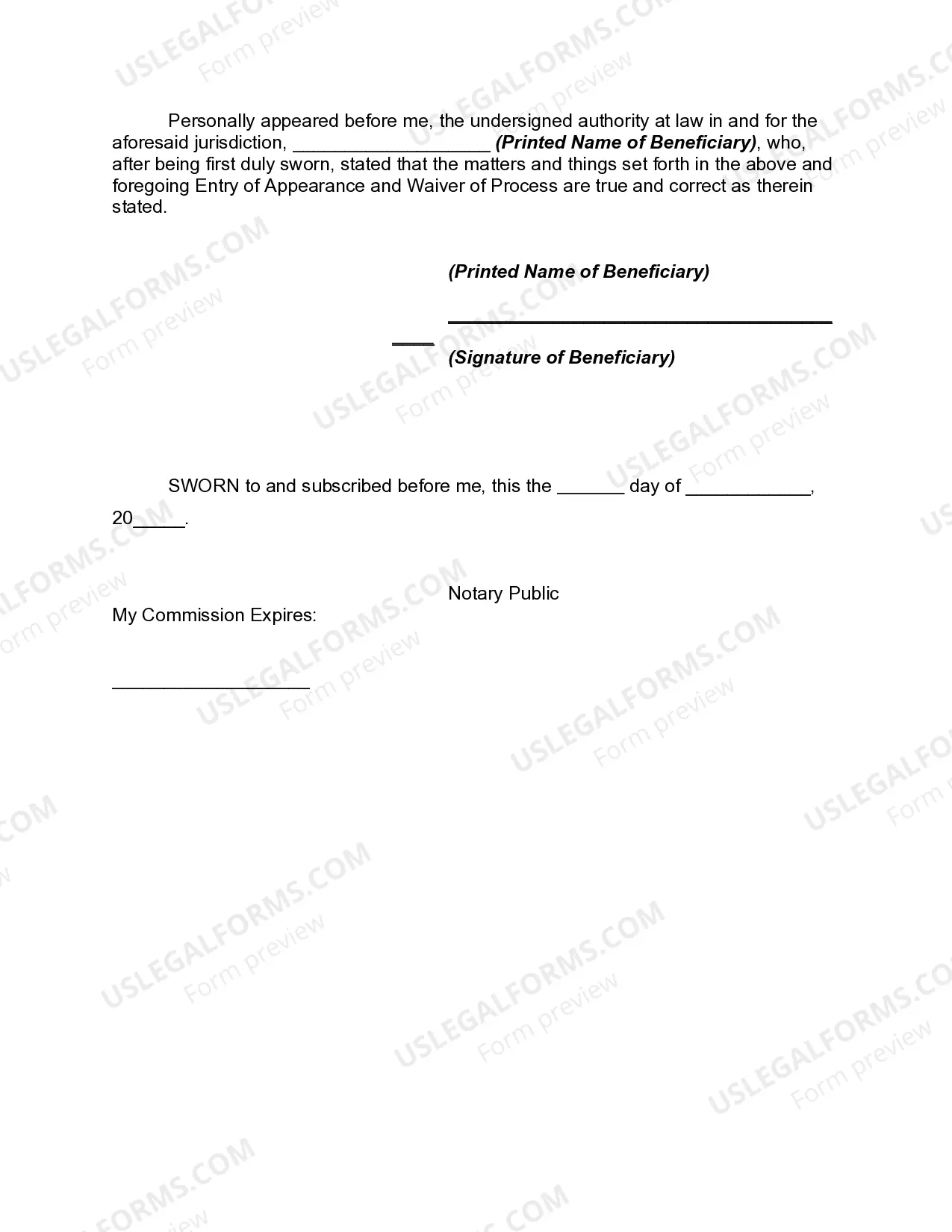

In order to close an estate a petition for final distribution should be filed before the court showing that the estate can be closed and requesting distribution to be made to the beneficiaries. Usually when a petition for final distribution is filed, the court requires detailed accounting of all the monies and other items received and all monies paid out during administration. However, the accounting may be waived when all persons entitled to receive property from the estate have executed a written waiver of accounting. Waiver simplifies the closing of the estate. When all the beneficiaries are friendly obtaining waiver is not a problem.

Hawaii Waiver of Final Accounting by Sole Beneficiary is a legal document commonly used in estate planning and administration processes. This waiver serves as a legal instrument through which a sole beneficiary relinquishes their right to request a final accounting of an estate's assets and distributions. By signing this document, the sole beneficiary acknowledges that they have received their entitled inheritance and allows the executor or personal representative to proceed with the estate's closing without the need for a detailed financial report. The Hawaii Waiver of Final Accounting by Sole Beneficiary provides several benefits for both the beneficiary and the estate administration process. Firstly, it expedites the settlement of the estate, allowing for a quicker distribution of assets and closure of the decedent's affairs. This waiver alleviates the burden on the executor by eliminating the need to prepare a comprehensive financial report and provides efficiency in the estate's administration. It is important to note that there are variations of the Hawaii Waiver of Final Accounting by Sole Beneficiary tailored to specific situations. These may include: 1. Hawaii Waiver of Final Accounting by Sole Beneficiary for Intestate Estates: This waiver is applicable when the deceased individual passed away without leaving a valid will (intestate). The sole beneficiary, in this case, agrees to waive their right to request a final accounting despite the absence of a will. 2. Hawaii Waiver of Final Accounting by Sole Beneficiary for Testate Estates: This waiver is used when the decedent had a valid will. The sole beneficiary, named in the will, agrees to waive their right to request a comprehensive financial report from the executor, acknowledging their satisfaction with the distribution of assets outlined in the will. 3. Hawaii Waiver of Final Accounting by Sole Beneficiary for Trust Estates: In cases where the estate is organized as a trust, this waiver is utilized. The sole beneficiary relinquishes their right to demand a final accounting from the trustee, acknowledging their agreement with the trust's administration and asset distribution. Executing a Hawaii Waiver of Final Accounting by Sole Beneficiary is a crucial step in the estate settlement process. It is strongly advisable to consult an attorney or seek legal advice to ensure that the waiver is properly drafted, executed, and aligned with the beneficiary's best interests. It is important for all parties involved to understand the implications and consequences of signing such a waiver, as it may limit their rights to future inquiries or challenges regarding the estate's administration and distribution.