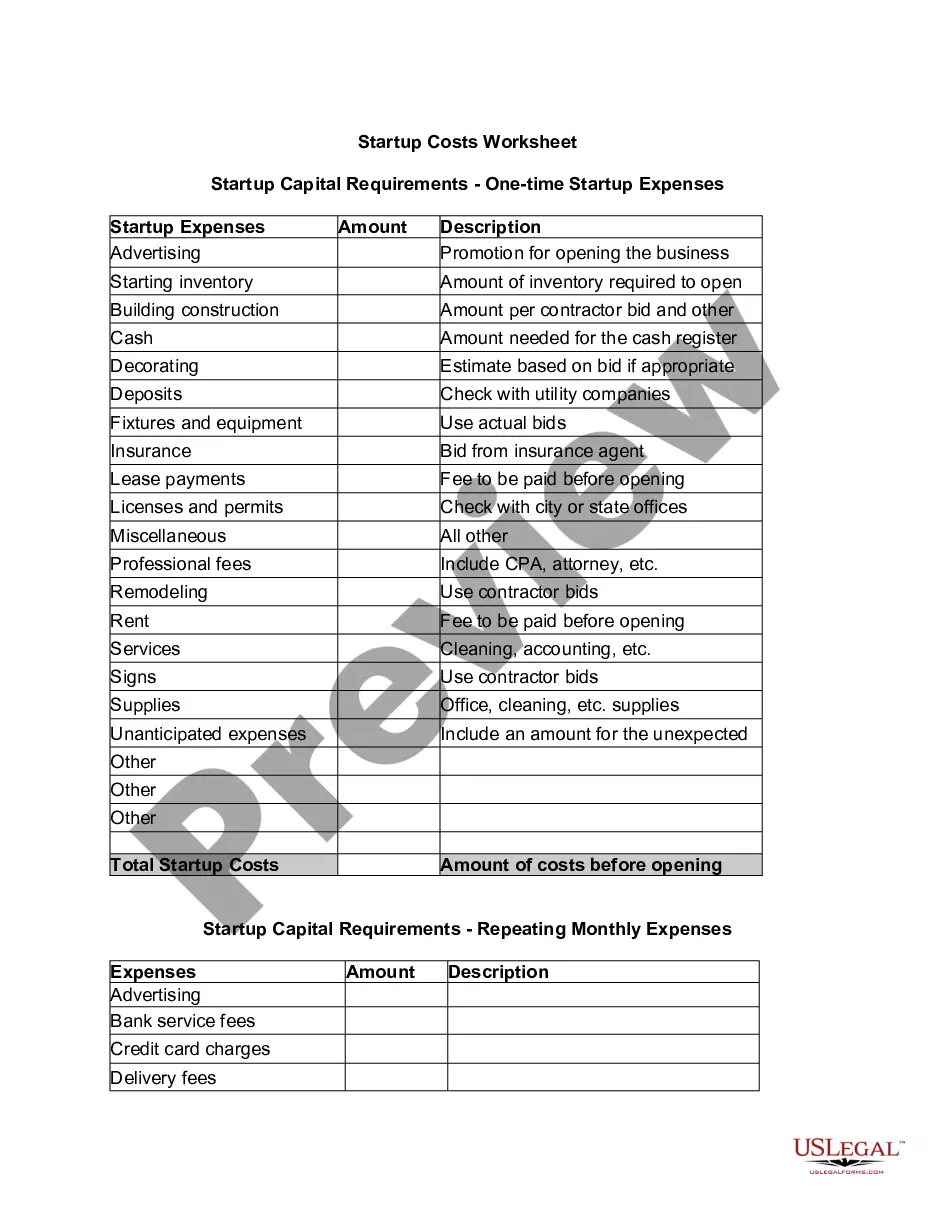

Hawaii Startup Costs Worksheet

Description

How to fill out Startup Costs Worksheet?

US Legal Forms - one of the largest legal document libraries in the United States - offers a broad selection of legal document templates that you can download or print.

By using the website, you can find thousands of forms for both business and personal use, organized by categories, states, or keywords. You can access the most current versions of forms such as the Hawaii Startup Costs Worksheet in moments.

If you have a membership, Log In to download the Hawaii Startup Costs Worksheet from the US Legal Forms library. The Download button will appear on every form you view. You have access to all previously obtained forms in the My documents section of your account.

Process the transaction. Use your Visa, Mastercard, or PayPal account to complete the transaction.

Select the format and download the form to your device. Edit. Fill out, modify, print, and sign the downloaded Hawaii Startup Costs Worksheet.

- Make sure you have selected the appropriate form for your city/county.

- Select the Review option to examine the content of the form.

- Refer to the form description to verify that you have picked the right form.

- If the form does not meet your requirements, use the Search feature at the top of the screen to find one that does.

- Once satisfied with the form, confirm your selection by clicking on the Get now button.

- Then, choose your preferred pricing plan and provide your credentials to register for an account.

Form popularity

FAQ

For those companies reporting under US GAAP, Financial Accounting Standards Codification 720 states that start up/organization costs should be expensed as incurred.

Essentially, the accounting for startup activities is to expense them as incurred. While the guidance is simple enough, the key issue is not to assume that other costs similar to start-up costs should be treated in the same way.

How to calculate startup costsIdentify your expenses. Start by writing down the startup costs you've already incurred but don't stop there.Estimate your costs. Once you've developed a list of your business needs, note the average cost for each category.Do the math.Add a cushion.Put the numbers to work.

Under GAAP, you report organizational or startup costs as an expense when you incur them. If you spend $5,000 on employee training prior to opening, you'd record $5,000 as a startup expense and reduce your cash account by $5,000. When you make out your taxes, the accounting for startup costs is more complicated.

What are examples of startup costs? Examples of startup costs include licensing and permits, insurance, office supplies, payroll, marketing costs, research expenses, and utilities.

Under Generally Accepted Accounting Principles, you report startup costs as expenses incurred at the time you spend the money. Some of your initial expenses, such as buying equipment, are not classified as startup costs under GAAP and have to be capitalized, not expensed.

Startup capital is what entrepreneurs use to pay for any or all of the required expenses involved in creating a new business. This includes paying for the initial hires, obtaining office space, permits, licenses, inventory, research and market testing, product manufacturing, marketing, or any other operational expense.

You can calculate the capital requirements by adding founding expenses, investments and start-up costs together. By subtracting your equity capital from the capital requirements, you calculate how much external capital you are going to need.

Start-up expenses are the costs of getting your business up and running. These include buying or leasing space, marketing costs, equipment, licenses, salaries, and the cost of servicing loans. Start-up assets are items of value, such as cash on hand, equipment, land, buildings, inventory, etc.

How to take IRS deductions. The IRS allows you to deduct $5,000 in business startup costs and $5,000 in organizational costs, but only if your total startup costs are $50,000 or less. If your startup costs in either area exceed $50,000, the amount of your allowable deduction will be reduced by the overage.