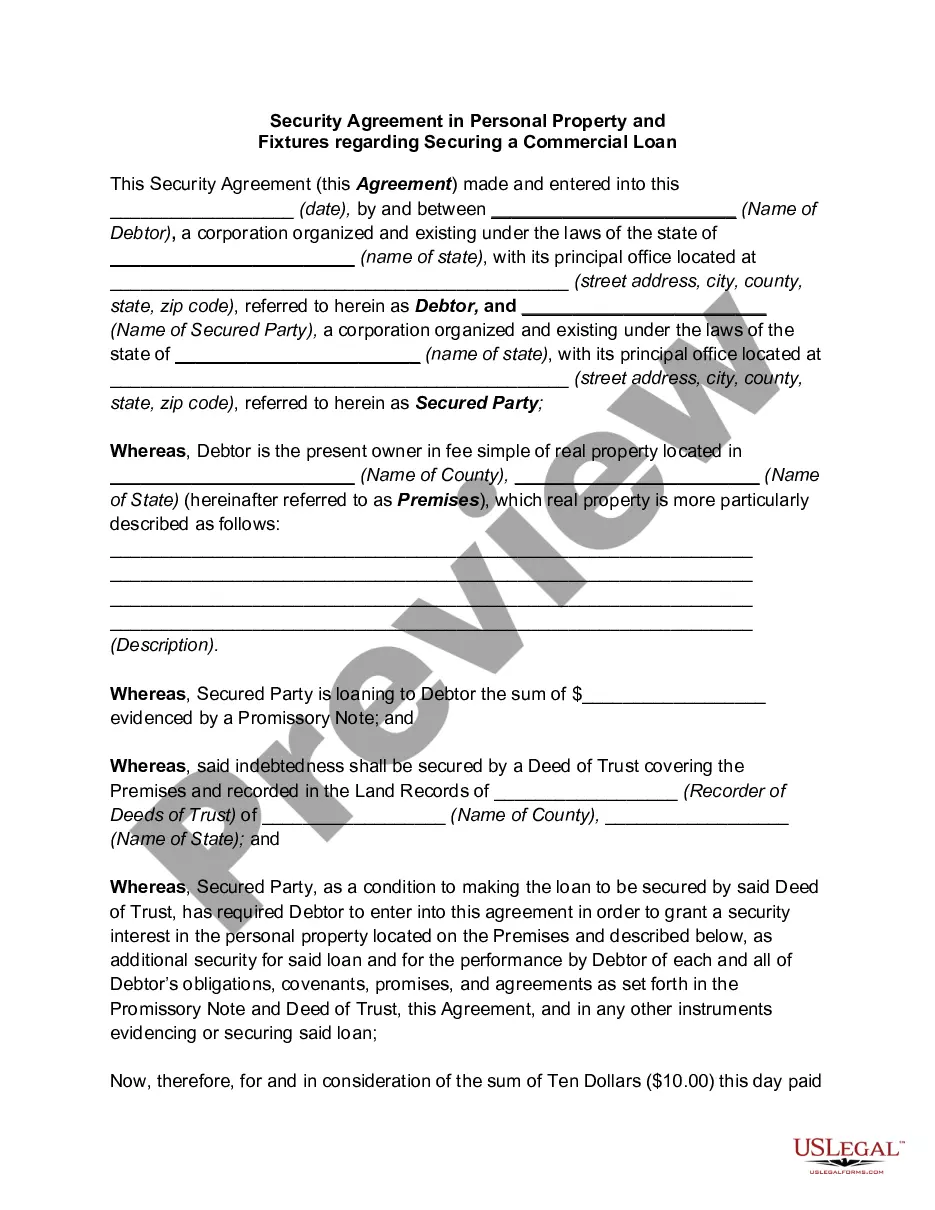

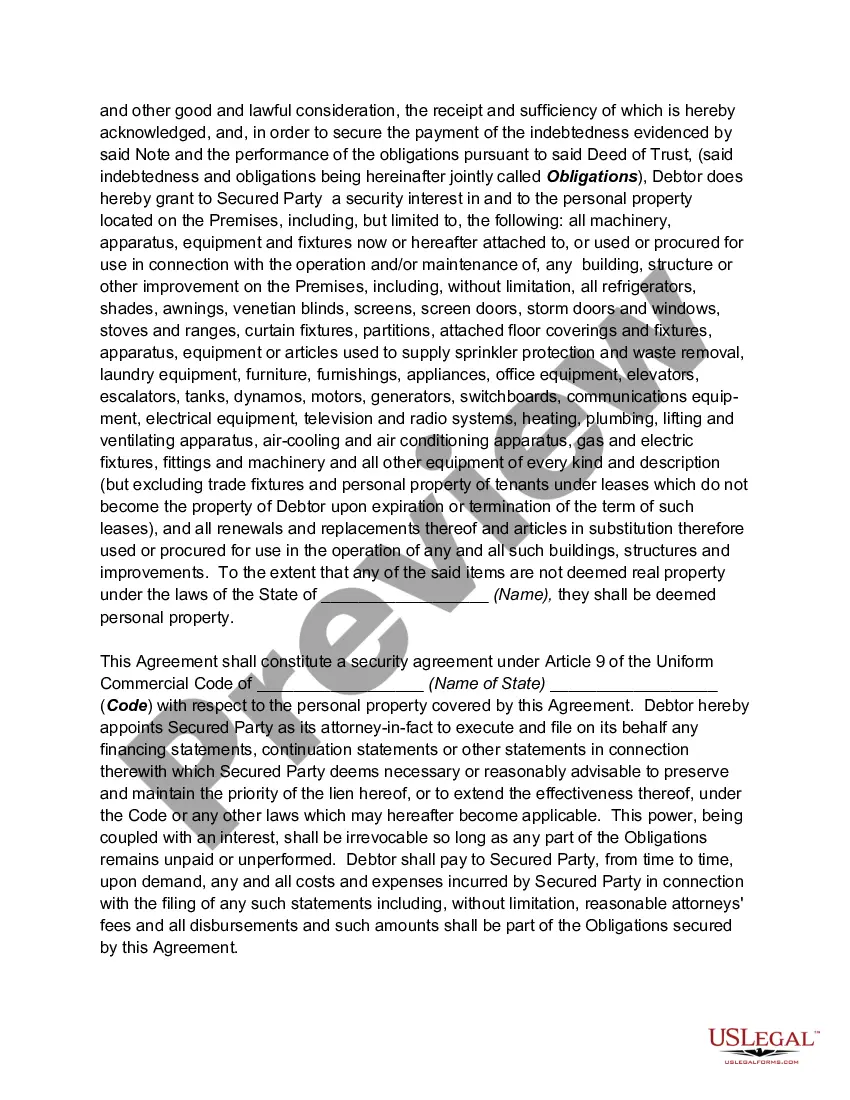

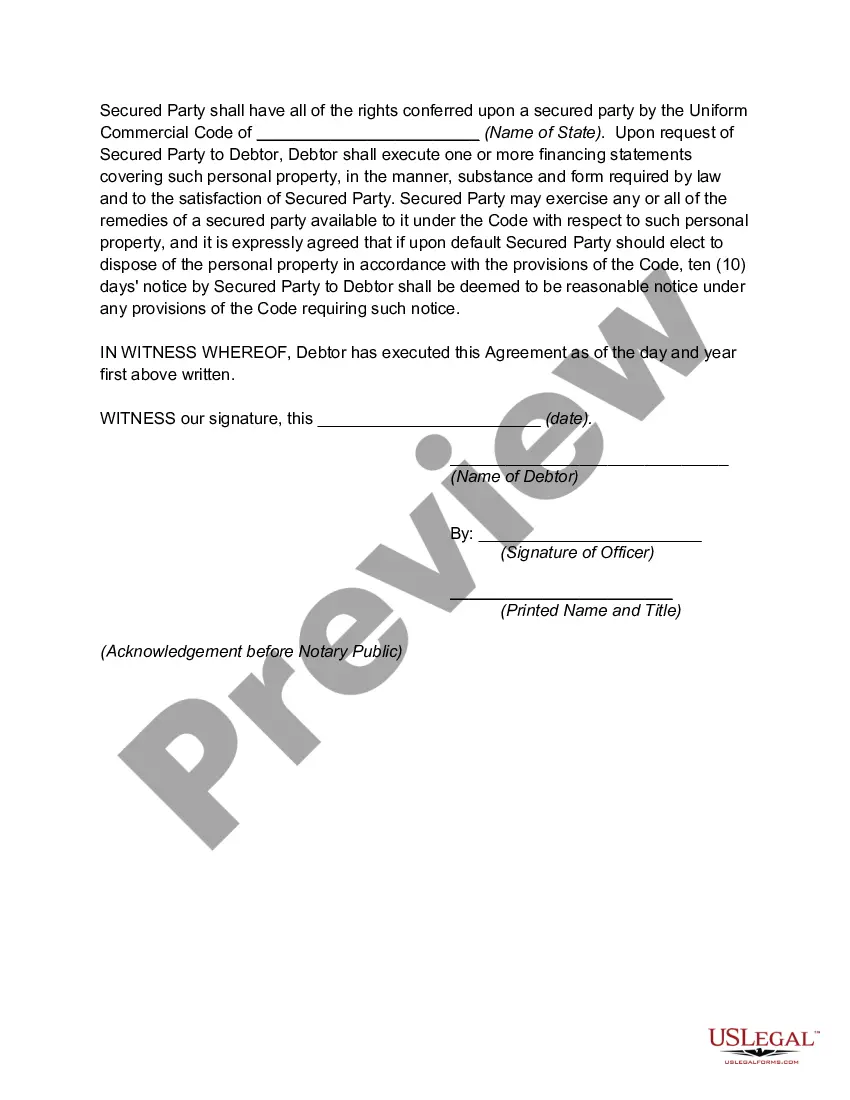

The Hawaii Security Agreement in Personal Property Fixtures is a legally binding document that plays a crucial role in securing a commercial loan in Hawaii. When a borrower seeks a loan, the lender often requires collateral to mitigate the risk involved in lending significant amounts of money. Personal property fixtures, such as equipment, machinery, furniture, and other movable assets, can be used as collateral to secure the loan. The security agreement establishes the lender's rights over these assets in case of default, ensuring their ability to recover the loan amount. There are different types of Hawaii Security Agreements in Personal Property Fixtures that may be used to secure a commercial loan: 1. General Security Agreement (GSA): This is the most common type of security agreement used in Hawaii. It covers all personal property fixtures owned by the borrower. The GSA provides the lender with a broad and comprehensive security interest in the borrower's assets, affording them a significant level of protection in case of default. 2. Specific Security Agreement (SSA): Unlike a GSA, an SSA applies to specific personal property fixtures rather than all the assets owned by the borrower. This agreement may be used when the lender wants to secure a loan against particular assets, such as expensive machinery or specialized equipment. 3. Floating Security Agreement (FSA): A FSA is a type of security agreement that allows the borrower to continue using and selling personal property fixtures while still securing the commercial loan. This type of agreement grants the lender a security interest in the current and future personal property fixtures of the borrower. It offers flexibility to both parties while ensuring the lender has collateral in case of default. In summary, the Hawaii Security Agreement in Personal Property Fixtures is a critical component of securing a commercial loan. Whether as a General Security Agreement, Specific Security Agreement, or Floating Security Agreement, it allows lenders to protect their investment by establishing a legal claim to personal property fixtures owned by the borrower, in case the loan defaults.

Hawaii Security Agreement in Personal Property Fixtures regarding Securing a Commercial Loan

Description

How to fill out Hawaii Security Agreement In Personal Property Fixtures Regarding Securing A Commercial Loan?

Are you presently in a placement where you need to have papers for possibly enterprise or person purposes virtually every working day? There are a lot of lawful document web templates available on the Internet, but finding types you can rely on isn`t simple. US Legal Forms provides a large number of form web templates, much like the Hawaii Security Agreement in Personal Property Fixtures regarding Securing a Commercial Loan, which are created to meet state and federal needs.

When you are already acquainted with US Legal Forms internet site and possess an account, basically log in. Afterward, you may obtain the Hawaii Security Agreement in Personal Property Fixtures regarding Securing a Commercial Loan web template.

If you do not provide an account and want to start using US Legal Forms, abide by these steps:

- Get the form you will need and make sure it is for the correct city/state.

- Use the Review switch to check the shape.

- Browse the outline to ensure that you have selected the right form.

- In the event the form isn`t what you are searching for, utilize the Search area to obtain the form that suits you and needs.

- Whenever you obtain the correct form, just click Buy now.

- Opt for the costs prepare you would like, submit the specified info to make your bank account, and buy your order using your PayPal or Visa or Mastercard.

- Pick a convenient document file format and obtain your version.

Find every one of the document web templates you might have purchased in the My Forms food list. You can get a additional version of Hawaii Security Agreement in Personal Property Fixtures regarding Securing a Commercial Loan whenever, if possible. Just click the necessary form to obtain or printing the document web template.

Use US Legal Forms, the most substantial selection of lawful kinds, to save lots of time as well as steer clear of errors. The service provides expertly manufactured lawful document web templates which you can use for an array of purposes. Generate an account on US Legal Forms and initiate generating your daily life easier.

Form popularity

FAQ

Security interest is an interest in personal property or fixtures that secures payment or performance of an obligation. Secured party is a lender, seller, or other person in whose favor a security interest exists.

Creating a security agreement Some key provisions in a security agreement include: Describing the collateral as accurately and as detailed as possible, so both the borrower and the lender agree upon the secured property. How to determine whether and when the borrower is in default under the loan.

A deed of trust, also called a trust deed, is the functional equivalent of a mortgage. It does not transfer the ownership of real property, as the typical deed does. Like a mortgage, a trust deed makes a piece of real property security (collateral) for a loan.

Let's consider an example. Credit transactions involving large ticket items, such as cars, homes or appliances, are usually secured. When I bought my new car, I borrowed money from my bank for my car loan. My loan is a secured transaction.

A security agreement is a document that provides a lender a security interest in a specified asset or property that is pledged as collateral.

Collateral is an asset pledged by a borrower, to a lender (or a creditor), as security for a loan.

Collateral is an item of value pledged to secure a loan. Collateral reduces the risk for lenders. If a borrower defaults on the loan, the lender can seize the collateral and sell it to recoup its losses. Mortgages and car loans are two types of collateralized loans.

Secured loans are also known as collateral loans, and the collateral you provide for a secured loan offsets some of the risk lenders take on when lending you money. If you're unable to repay the debt, your lender can seize your collateral to recoup their financial losses.