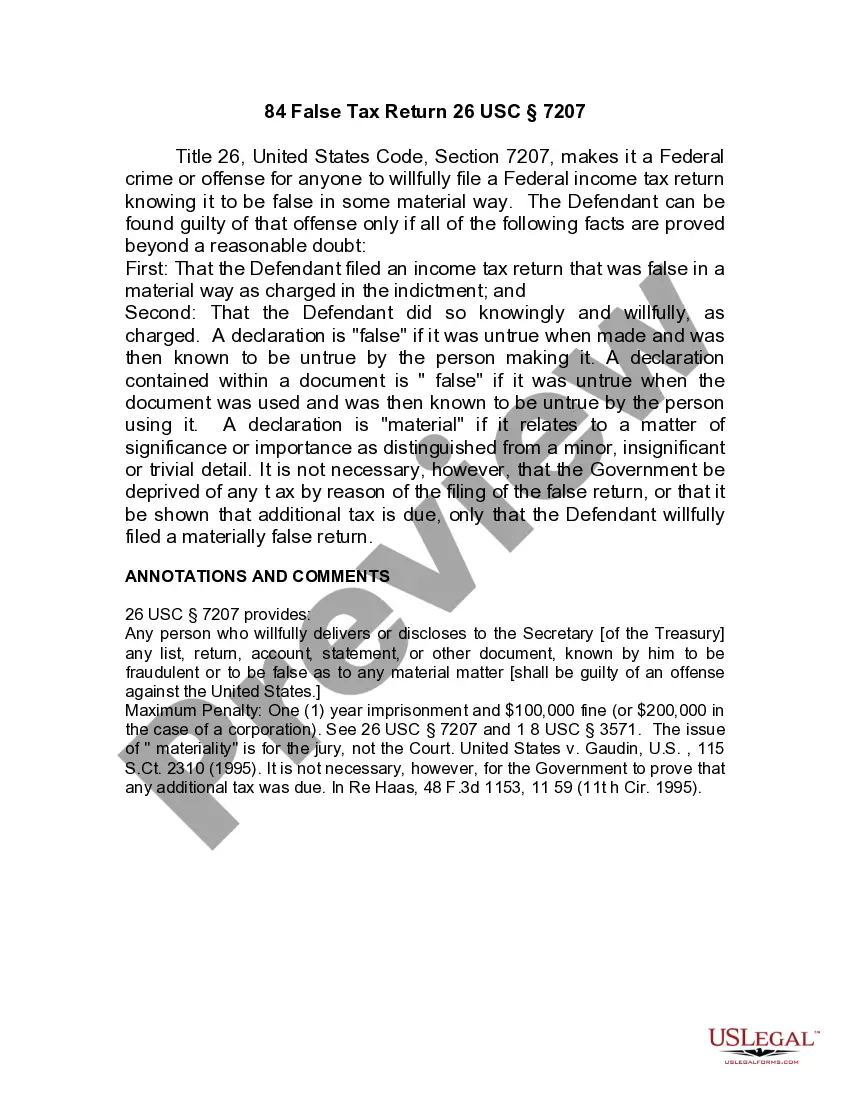

Hawaii Jury Instruction - 10.10.6 Section 6672 Penalty

Description

How to fill out Jury Instruction - 10.10.6 Section 6672 Penalty?

Are you inside a position where you need to have paperwork for possibly organization or individual functions almost every working day? There are tons of legal papers themes available on the net, but finding versions you can depend on isn`t easy. US Legal Forms provides thousands of develop themes, like the Hawaii Jury Instruction - 10.10.6 Section 6672 Penalty, that happen to be composed to meet state and federal requirements.

If you are previously familiar with US Legal Forms site and have a merchant account, just log in. Next, it is possible to obtain the Hawaii Jury Instruction - 10.10.6 Section 6672 Penalty format.

Should you not come with an accounts and would like to begin to use US Legal Forms, abide by these steps:

- Discover the develop you need and make sure it is for that right metropolis/region.

- Take advantage of the Preview switch to examine the shape.

- See the explanation to actually have selected the correct develop.

- In case the develop isn`t what you are looking for, utilize the Research field to find the develop that meets your requirements and requirements.

- If you get the right develop, click on Buy now.

- Select the pricing plan you desire, submit the necessary info to make your bank account, and pay money for your order with your PayPal or Visa or Mastercard.

- Decide on a practical document format and obtain your version.

Find all of the papers themes you might have purchased in the My Forms menu. You can get a more version of Hawaii Jury Instruction - 10.10.6 Section 6672 Penalty any time, if required. Just go through the required develop to obtain or produce the papers format.

Use US Legal Forms, one of the most comprehensive assortment of legal varieties, to conserve time as well as avoid faults. The services provides professionally manufactured legal papers themes which you can use for a variety of functions. Produce a merchant account on US Legal Forms and begin creating your daily life a little easier.

Form popularity

FAQ

418, the California Supreme Court articulated 'three guideposts' for courts reviewing punitive damages: ?(1) the degree of reprehensibility of the defendant's misconduct; (2) the disparity between the actual or potential harm suffered by the plaintiff and the punitive damages award; and (3) the difference between the ...

"Punitive damages" are awarded against a defendant for the purpose of punishing the defendant for its misconduct, or to deter one or both Defendants and others like such defendant from committing such conduct in the future.

You may award punitive damages only if you find that the defendant's conduct that harmed the plaintiff was malicious, oppressive or in reckless disregard of the plaintiff's rights. Conduct is malicious if it is accompanied by ill will, or spite, or if it is for the purpose of injuring the plaintiff.

In addition to compensatory damages, juries in some cases may also award punitive damages, a class of damages which serve to punish unlawful conduct and to deter similar future conduct. BMW of North Am., Inc. v. Gore, 517 U.S. 559, 568 (1996).

Punitive damages are awarded in less than 5 percent of civil jury verdicts, ing to a 1990 American Bar Foundation study of 25,000 jury verdicts in 11 states over a four-year period.

Punitive damages are warranted against (defendant) if you find by clear and convincing evidence that (managing agent, primary owner, or other person whose conduct may warrant punitive damages without proof of a superior's fault) [was] [were] personally guilty of [intentional misconduct] [or] [gross negligence], which ...