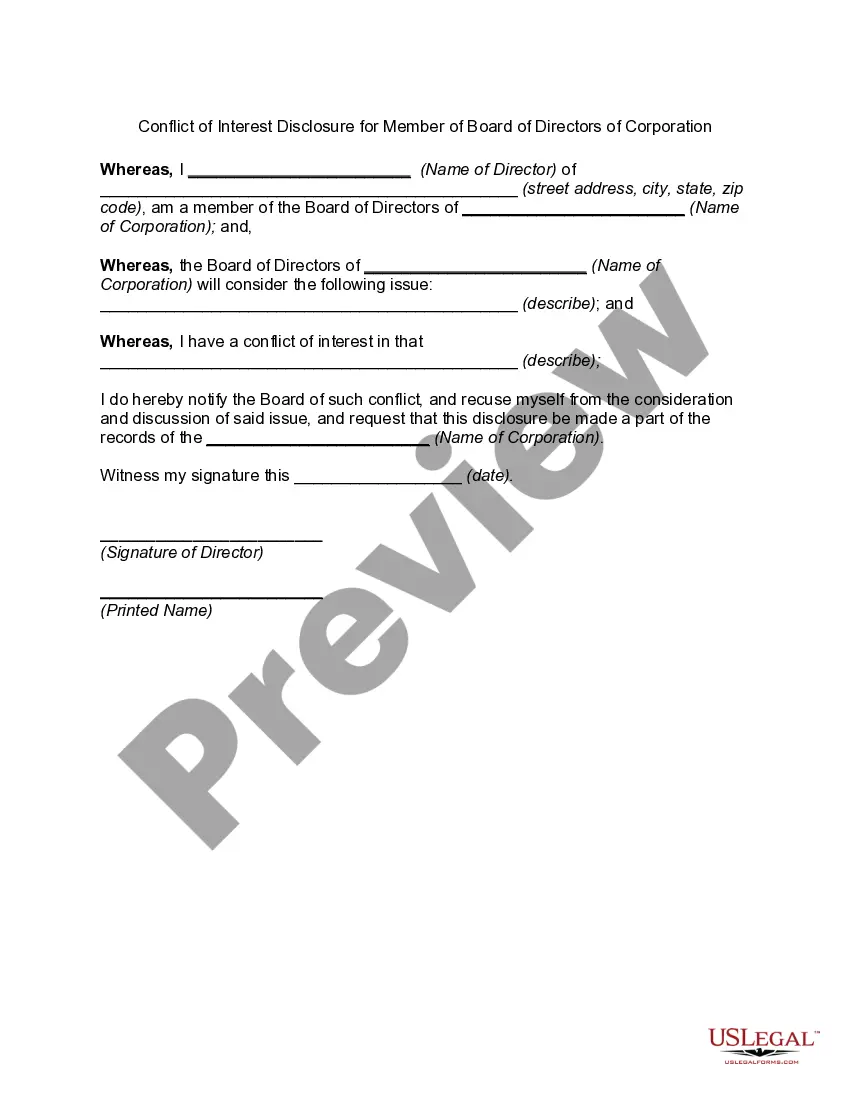

Hawaii Conflict of Interest Disclosure for Member of Board of Directors of Corporation is an essential and mandatory process to ensure transparency, accountability, and ethical decision-making within corporate governance in Hawaii. The purpose behind this disclosure requirement is to prevent any potential conflicts of interest that may arise between a director's personal or financial interests and their obligations to the corporation. A Hawaii Conflict of Interest Disclosure requires board members to disclose any personal, financial, or external interests that may influence their decision-making processes as a director. This disclosure helps to maintain the integrity of the corporation and ensures that board members act in the best interests of the company and its stakeholders. The Hawaii Conflict of Interest Disclosure for Member of Board of Directors may come in different forms, depending on the specific circumstances. Some common types include: 1. Financial Interests Disclosure: This type of disclosure requires board members to reveal any financial interests, such as ownership in other companies, stock holdings, investments, or loans, that could potentially create conflicts when making decisions on behalf of the corporation. 2. Related Party Transactions Disclosure: Board members must disclose any transactions or business dealings with the corporation involving a related party. Related parties could include immediate family members, close associates, or entities in which the director has a significant interest. The goal is to expose any potential bias or benefits that the director or related parties may gain from such transactions. 3. Outside Employment Disclosure: If a board member holds a position with another organization, the member must disclose this information to determine if any conflict of interest may arise due to divided loyalty, potential competition, or interference with their ability to fulfill their duties to the corporation. 4. Non-Financial Interests Disclosure: This type of disclosure involves identifying any non-financial interests, such as memberships in professional associations, involvement in community organizations, or participation on other boards, that could create potential conflicts or perceived biases. 5. Ongoing Disclosure Obligations: Board members must be vigilant in ensuring that disclosures are made on an ongoing basis. They should promptly update their disclosures if any new potential conflicts of interest arise during their tenure as board members. Hawaii Conflict of Interest Disclosure for Member of Board of Directors of Corporation is an essential tool to maintain the integrity and impartiality of corporate decision-making. By requiring board members to disclose potential conflicts, Hawaii aims to ensure that directors act solely in the best interests of the corporation and its shareholders. Compliance with this disclosure requirement is crucial to uphold ethical standards and maintain the trust of stakeholders.

Hawaii Conflict of Interest Disclosure for Member of Board of Directors of Corporation

Description

How to fill out Hawaii Conflict Of Interest Disclosure For Member Of Board Of Directors Of Corporation?

US Legal Forms - one of the greatest libraries of legitimate forms in the United States - provides an array of legitimate record templates you may download or printing. While using site, you can find a large number of forms for company and specific purposes, categorized by categories, says, or search phrases.You can find the most up-to-date models of forms much like the Hawaii Conflict of Interest Disclosure for Member of Board of Directors of Corporation in seconds.

If you currently have a subscription, log in and download Hawaii Conflict of Interest Disclosure for Member of Board of Directors of Corporation from the US Legal Forms collection. The Down load switch will appear on each form you view. You have access to all in the past delivered electronically forms inside the My Forms tab of your own account.

If you want to use US Legal Forms the first time, listed here are simple instructions to help you get started off:

- Ensure you have selected the best form for your personal area/state. Go through the Preview switch to check the form`s content. See the form explanation to ensure that you have selected the appropriate form.

- In the event the form doesn`t satisfy your demands, make use of the Look for field towards the top of the monitor to discover the one which does.

- In case you are content with the form, confirm your option by visiting the Purchase now switch. Then, opt for the costs prepare you favor and supply your accreditations to sign up on an account.

- Method the financial transaction. Make use of credit card or PayPal account to complete the financial transaction.

- Find the structure and download the form in your system.

- Make changes. Fill up, change and printing and indicator the delivered electronically Hawaii Conflict of Interest Disclosure for Member of Board of Directors of Corporation.

Every single template you included with your money does not have an expiration particular date and it is your own property eternally. So, if you want to download or printing an additional duplicate, just proceed to the My Forms portion and click on in the form you need.

Gain access to the Hawaii Conflict of Interest Disclosure for Member of Board of Directors of Corporation with US Legal Forms, by far the most comprehensive collection of legitimate record templates. Use a large number of skilled and state-particular templates that satisfy your small business or specific requires and demands.