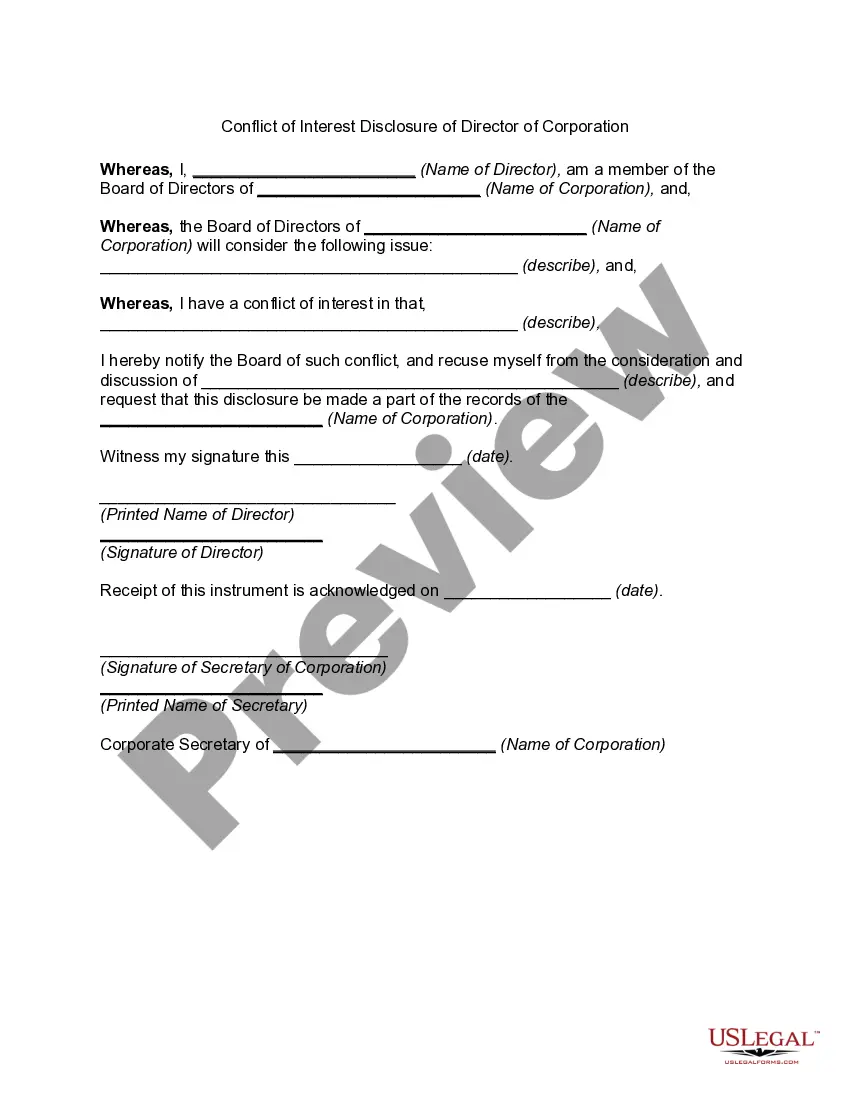

Hawaii Conflict of Interest Disclosure is a crucial requirement mandated by the state for directors of corporations. It is a legal obligation that ensures transparency, promotes fairness, and prevents any potential conflicts of interest within corporate governance. This disclosure serves as a safeguard for the company and its stakeholders, providing a framework for directors to act ethically and in the best interests of the corporation. Directors of corporations in Hawaii are obliged to disclose any potential conflicts of interest that may arise in their role. A conflict of interest occurs when a director's personal or financial interests intersect with the interests of the corporation they serve. This disclosure helps maintain the utmost integrity, credibility, and accountability in corporate decision-making processes. The Hawaii Conflict of Interest Disclosure involves the clear identification and declaration of any actual or perceived conflicts. Directors must provide comprehensive and detailed information that encompasses their relationships, financial interests, and other relevant associations that may impact their ability to make unbiased decisions on behalf of the corporation. Some key elements included in a Hawaii Conflict of Interest Disclosure are: 1. Financial Interests: Directors are required to disclose any financial investments, holdings, or transactions that could influence their decision-making process. This may include stocks, bonds, real estate, partnerships, or any other investments that could potentially impact the corporation's interests. 2. Relationships: Directors must disclose any personal or professional relationships that could potentially lead to conflicts of interest. This includes associations with suppliers, competitors, customers, or any other parties that may influence their objectivity or independence. 3. Gifts and Benefits: Any gifts, benefits, or perks received by directors that could affect their judgment or decision-making process must be disclosed. This transparency ensures unbiased decision-making and prevents any undue influence. 4. Related Party Transactions: Directors must disclose any transactions or dealings with the corporation involving related parties, such as family members, close associates, or other companies in which they have a financial interest. These transactions may require additional scrutiny to ensure fairness and the absence of self-dealing. 5. Disclosure Updates: Directors should regularly update their disclosure to reflect any changes in their financial interests, relationships, or other relevant circumstances. This ensures that the corporation and its stakeholders have up-to-date information to assess potential conflicts of interest. Different types of Hawaii Conflict of Interest Disclosures may exist based on the nature of the corporation or regulatory requirements. For example, nonprofit corporations may have specific disclosure requirements that cater to their unique governance structure and potential conflicts arising from charitable activities. In conclusion, the Hawaii Conflict of Interest Disclosure for directors of corporations is an essential component of ethical corporate governance. It promotes transparency, protects stakeholders' interests, and ensures directors prioritize the corporation's well-being. By disclosing potential conflicts of interest, directors can fulfill their fiduciary duty responsibly, building trust and maintaining the highest standards of corporate integrity.

Hawaii Conflict of Interest Disclosure of Director of Corporation

Description

How to fill out Hawaii Conflict Of Interest Disclosure Of Director Of Corporation?

You may spend several hours on the Internet trying to find the authorized document format that meets the federal and state needs you want. US Legal Forms offers a large number of authorized forms which are reviewed by specialists. You can easily obtain or produce the Hawaii Conflict of Interest Disclosure of Director of Corporation from your support.

If you already have a US Legal Forms accounts, you may log in and then click the Down load key. Next, you may full, modify, produce, or signal the Hawaii Conflict of Interest Disclosure of Director of Corporation. Each and every authorized document format you buy is your own property eternally. To obtain one more copy for any acquired form, proceed to the My Forms tab and then click the corresponding key.

If you use the US Legal Forms internet site initially, stick to the basic directions listed below:

- Initial, ensure that you have chosen the right document format for the area/city that you pick. Look at the form description to make sure you have selected the correct form. If available, use the Review key to check throughout the document format also.

- If you wish to get one more version of your form, use the Lookup area to get the format that suits you and needs.

- When you have discovered the format you would like, just click Get now to move forward.

- Choose the prices prepare you would like, enter your references, and sign up for your account on US Legal Forms.

- Complete the financial transaction. You should use your Visa or Mastercard or PayPal accounts to purchase the authorized form.

- Choose the format of your document and obtain it for your device.

- Make changes for your document if necessary. You may full, modify and signal and produce Hawaii Conflict of Interest Disclosure of Director of Corporation.

Down load and produce a large number of document themes using the US Legal Forms website, which provides the biggest collection of authorized forms. Use specialist and express-certain themes to take on your small business or personal requires.