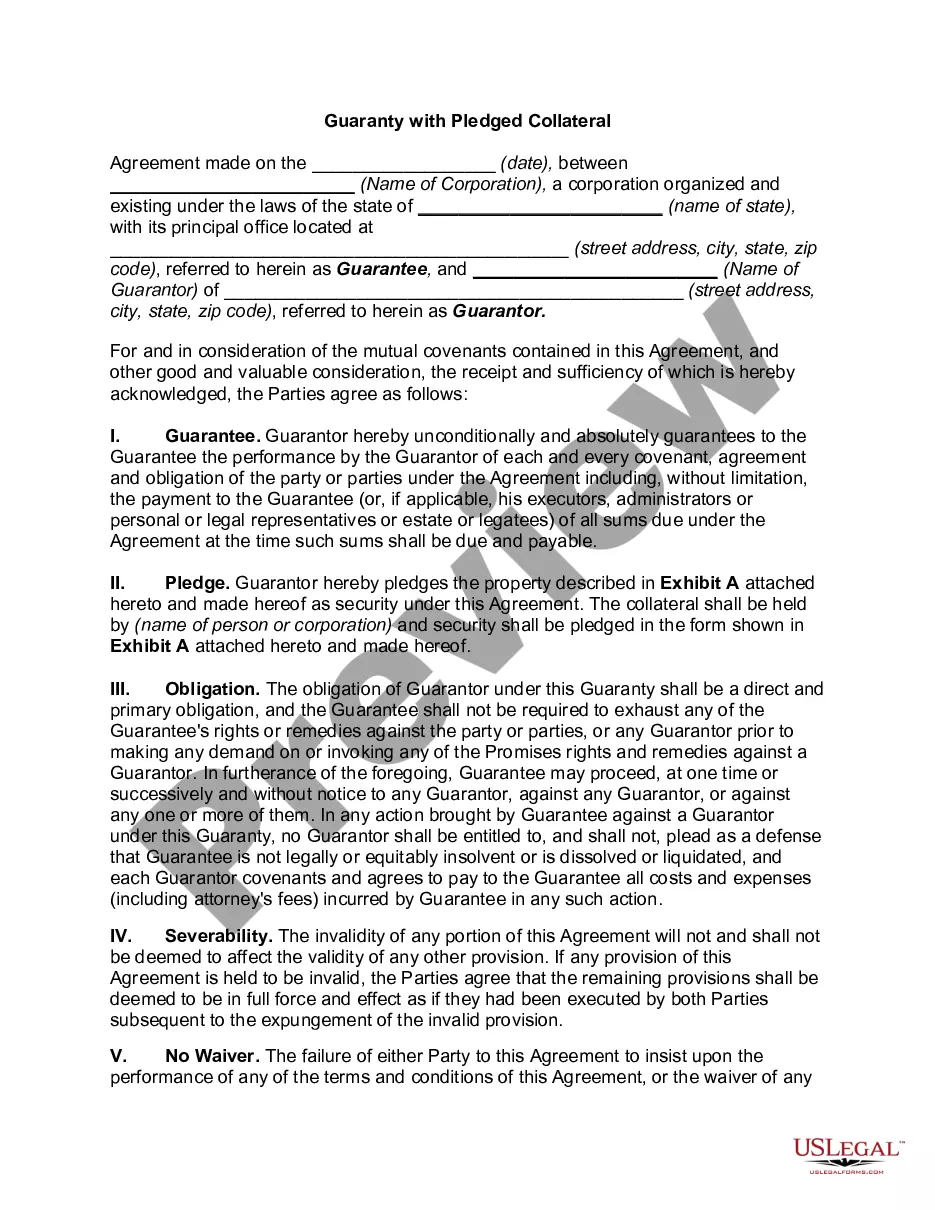

Hawaii Guaranty with Pledged Collateral is a financial agreement that provides an additional layer of security for lending institutions when extending credit to borrowers in Hawaii. In this arrangement, borrowers pledge collateral, such as real estate property or assets, to the lender as a guarantee against the loan amount. If the borrower defaults on the loan repayment, the lender has the right to seize and sell the pledged collateral to recover the outstanding debt. This type of guaranty is commonly used in various lending scenarios, including commercial loans, mortgages, and personal loans. It offers lenders a level of protection by reducing their potential losses in case of default. By securing the loan with pledged collateral, lenders can have more confidence in extending credit to borrowers who may have limited credit history or financial standing. Different types of Hawaii Guaranty with Pledged Collateral may include: 1. Mortgage Guaranty: This type of guaranty is commonly used in real estate transactions, where the borrower pledges the property being financed as collateral. If the borrower fails to repay the mortgage, the lender can foreclose on the property to recoup the loan amount. 2. Asset-Based Loan Guaranty: In this type of Guaranty, borrowers pledge specific assets, such as inventory, equipment, or accounts receivable, as collateral against the loan. Lenders often conduct thorough assessments of the pledged assets to determine their value and potential liquidation in case of default. 3. Secured Personal Loan Guaranty: Personal loans, such as auto loans or debt consolidation loans, can also utilize pledged collateral. Borrowers may pledge their vehicles, savings accounts, or other valuable assets to secure the loan. If the borrower defaults, the lender can seize and sell the collateralized assets to cover the unpaid debt. 4. Business Loan Guaranty: When businesses require capital for expansion, equipment purchases, or operational needs, lenders may request collateral to secure the loan. This can include commercial properties, inventory, accounts receivable, or business assets. It is important for borrowers to fully understand the terms and conditions of a Hawaii Guaranty with Pledged Collateral before entering into such agreements. They should carefully assess their ability to repay the loan and the potential risks associated with the pledged collateral. Lenders, on the other hand, benefit from reduced risk exposure due to the added security provided by the pledged collateral.

Hawaii Guaranty with Pledged Collateral

Description

How to fill out Hawaii Guaranty With Pledged Collateral?

US Legal Forms - one of several greatest libraries of lawful kinds in the United States - gives a variety of lawful papers web templates you may obtain or print. Using the web site, you can find a huge number of kinds for organization and personal purposes, sorted by types, suggests, or keywords and phrases.You can find the newest models of kinds like the Hawaii Guaranty with Pledged Collateral within minutes.

If you have a monthly subscription, log in and obtain Hawaii Guaranty with Pledged Collateral from the US Legal Forms collection. The Download button will appear on each and every kind you perspective. You gain access to all formerly acquired kinds in the My Forms tab of your bank account.

If you wish to use US Legal Forms initially, here are straightforward guidelines to help you get began:

- Make sure you have selected the proper kind for your metropolis/state. Click the Review button to review the form`s articles. See the kind information to actually have selected the appropriate kind.

- If the kind doesn`t suit your needs, utilize the Research area on top of the display screen to discover the one which does.

- Should you be satisfied with the shape, validate your option by simply clicking the Acquire now button. Then, choose the prices strategy you prefer and give your credentials to register on an bank account.

- Method the financial transaction. Utilize your bank card or PayPal bank account to complete the financial transaction.

- Choose the format and obtain the shape on the device.

- Make changes. Fill up, change and print and indication the acquired Hawaii Guaranty with Pledged Collateral.

Each web template you included in your money does not have an expiry particular date and is your own property for a long time. So, if you want to obtain or print yet another duplicate, just visit the My Forms section and click on on the kind you require.

Get access to the Hawaii Guaranty with Pledged Collateral with US Legal Forms, one of the most substantial collection of lawful papers web templates. Use a huge number of specialist and state-particular web templates that meet your company or personal requirements and needs.

Form popularity

FAQ

To pledge assets as collateral (or Pledging) is the act of offering assets as collateral to secure loans. Assets pledged can be in the form of security holdings and act as assurance for recovering the borrowed amount should a borrower fail to pay up.

A pledged asset is a valuable possession that is transferred to a lender to secure a debt or loan. A pledged asset is collateral held by a lender in return for lending funds. Pledged assets can reduce the down payment that is typically required for a loan as well as reduces the interest rate charged.

A pledged asset is a valuable asset that is transferred to a lender to secure a debt or loan. Pledged assets can reduce the down payment that is typically required for a loan. The asset may also provide a better interest rate or repayment terms for the loan.

An agreement typically used to create a security interest in equity interests (including capital stock, LLC interests, and partnership interests) and promissory notes.

Guarantee vs collateral what's the difference? A personal guarantee is a signed document that promises to repay back a loan in the event that your business defaults. Collateral is a good or an owned asset that you use toward loan security in the event that your business defaults.

It's important to note that a loan with a personal guarantee is not considered a secured loan because the agreement is not tied to any specific assets i.e., collateral.

A negative pledge agreement is sometimes signed as a stand-alone document, and, if real estate is involved, a negative pledge agreement will often be recorded in the county where the real estate is located.

A personal guarantee is an unsecured written promise from a business owner and or business executive guaranteeing payment on an equipment lease or loan in the event the business does not pay. Since it is unsecured, a personal guarantee is not tied to a specific asset.

As nouns the difference between pledge and collateral is that pledge is a solemn promise to do something while collateral is a security or guarantee (usually an asset) pledged for the repayment of a loan if one cannot procure enough funds to repay (originally supplied as "accompanying" security).

Pledged collateral refers to assets that are used to secure a loan. The borrower pledges assets or property to the lender to guarantee or secure the loan.