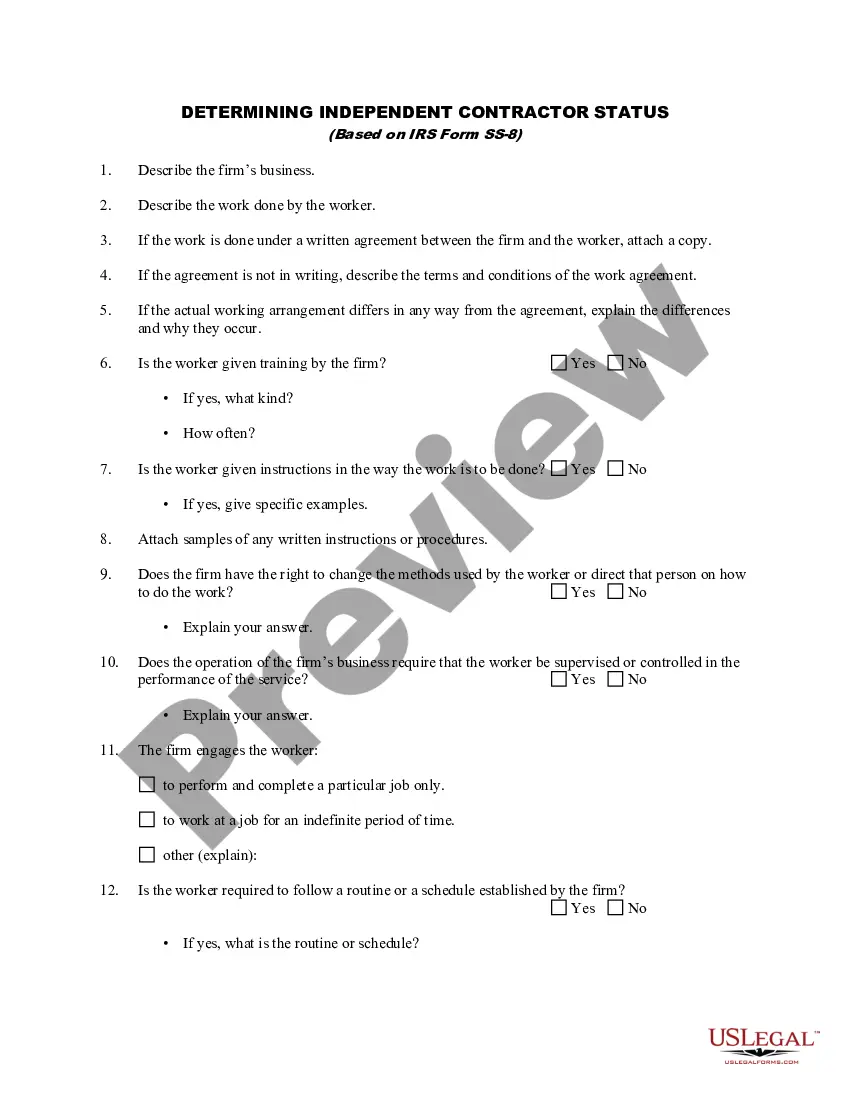

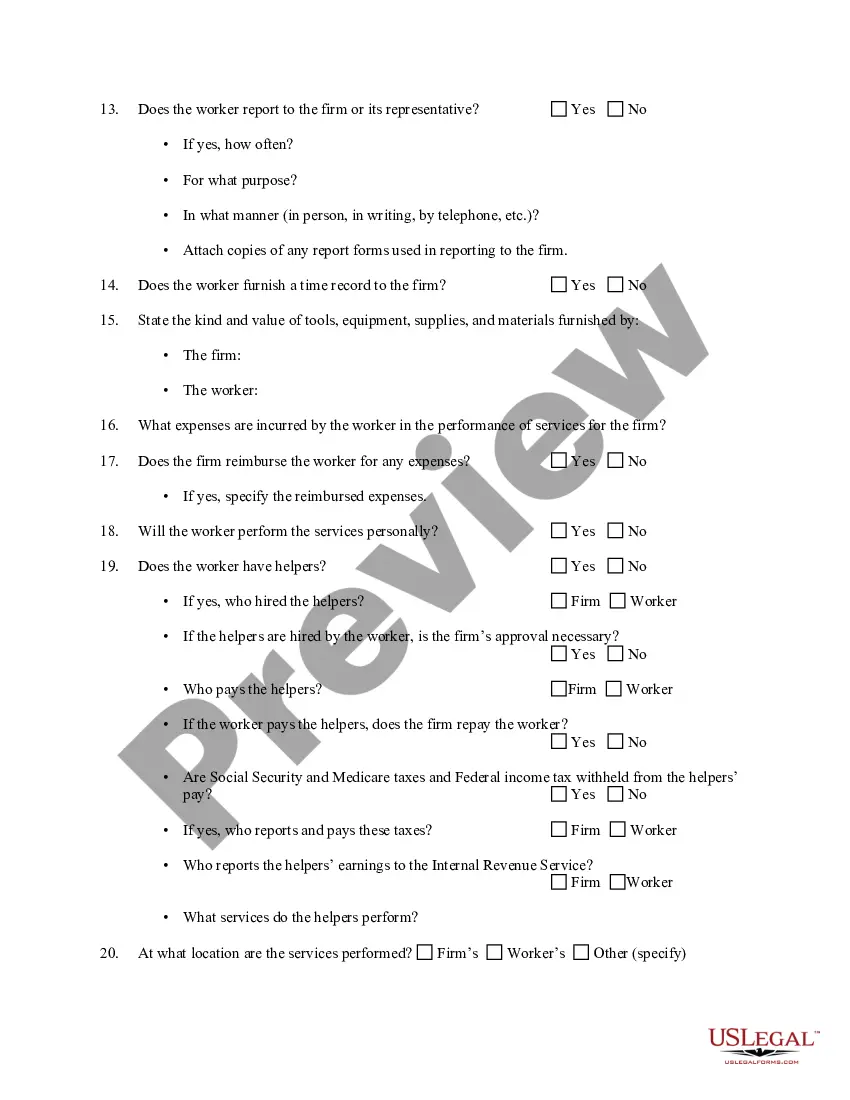

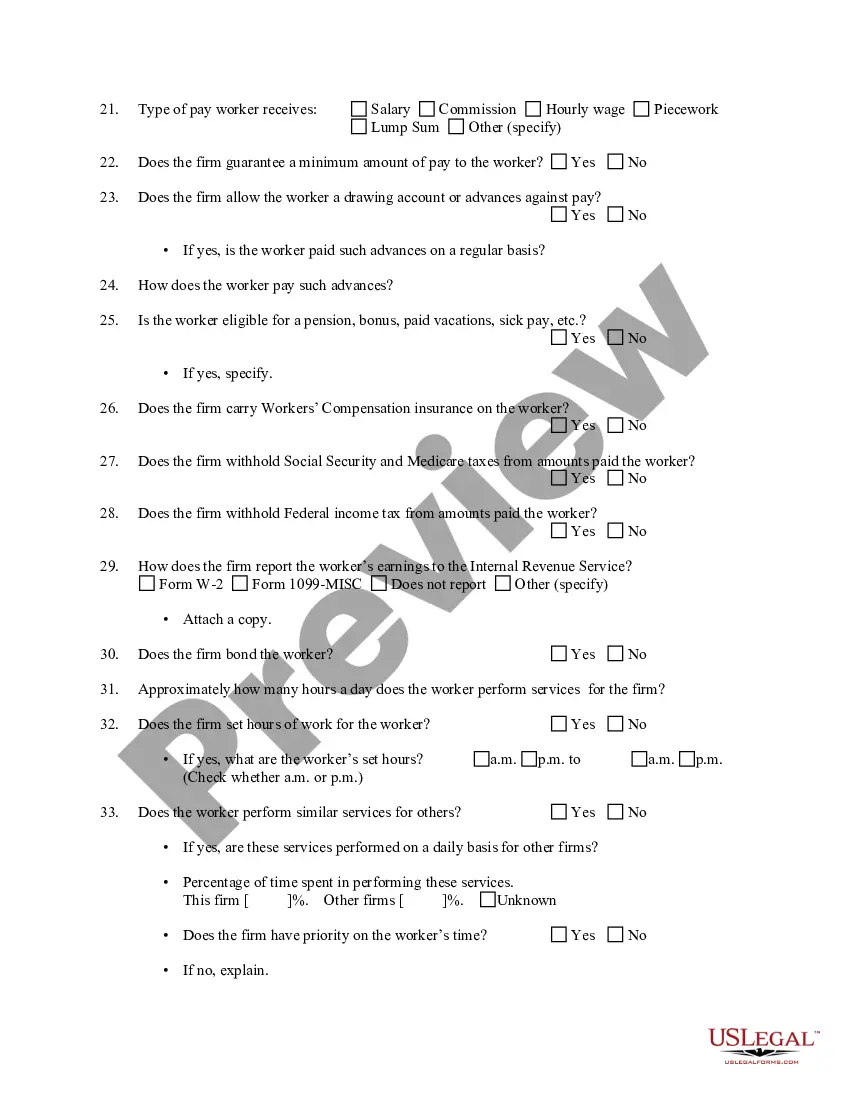

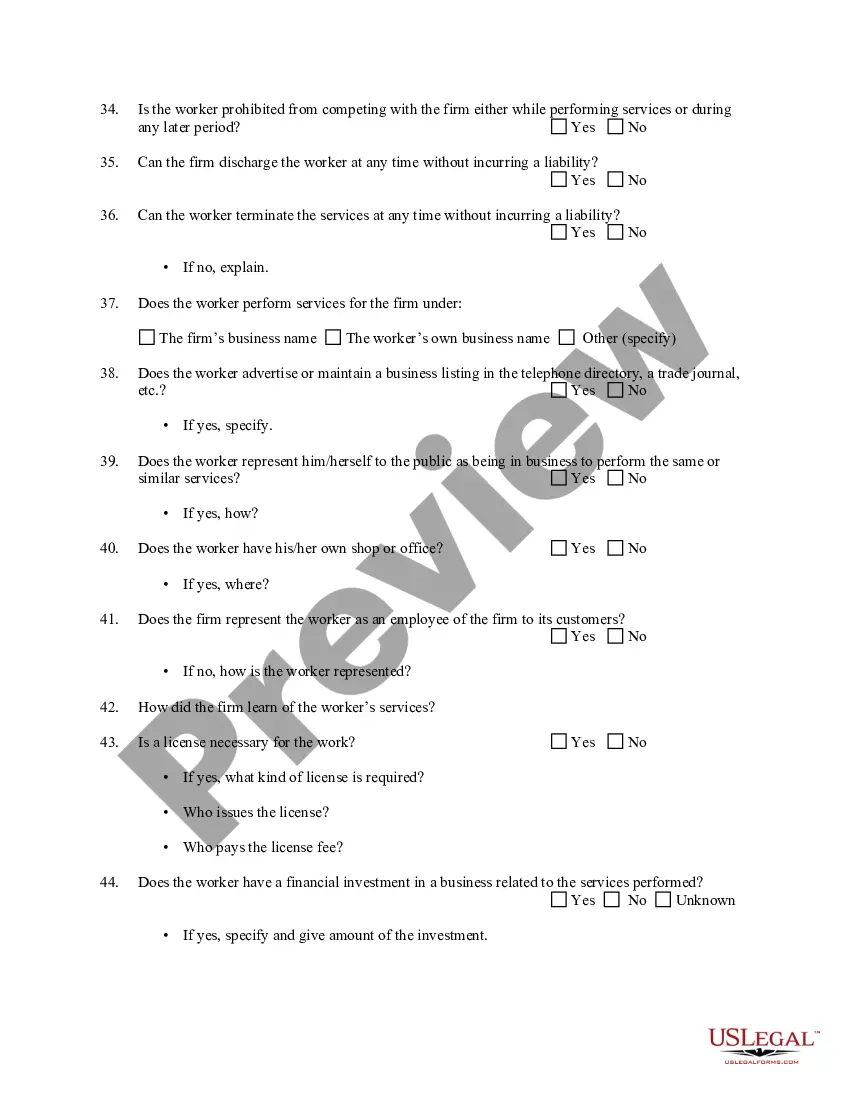

Hawaii Determining Self-Employed Independent Contractor Status: A Comprehensive Guide In Hawaii, determining self-employed independent contractor status is a crucial aspect of labor law compliance. It involves accurately classifying individuals who work for a business or organization as either employees or independent contractors. The classification holds significant legal and tax implications, affecting wage and hour rights, insurance coverage, retirement benefits, and more. It is important to understand that the Hawaii Department of Labor and Industrial Relations (DLR) uses various criteria to determine the classification, including aspects such as behavioral control, financial control, and the nature of the working relationship. Let's delve into each of these elements to gain a clearer understanding: 1. Behavioral Control: This aspect considers whether the hiring company has the right to control how the individual performs their work. Indicators might include instructions given to the worker, training provided, and the level of supervision. If the company has significant control over these factors, the individual may be classified as an employee. 2. Financial Control: This criterion focuses on the degree of control the worker has over their financial affairs in the engagement. Key elements include the ability to realize a profit or loss, controlling significant aspects of their business operations, and having the freedom to offer their services to multiple clients. If the individual has a high level of financial control, they may be deemed an independent contractor. 3. Nature of the Working Relationship: This aspect examines the overall relationship between the hiring company and the worker. It considers factors such as the presence or absence of a written contract, whether the individual receives employee benefits, and the permanency or duration of the working relationship. This evaluation aims to determine whether the individual is an integrated part of the company's workforce or maintains an independent business entity. It's essential for employers to carefully assess these factors to ensure compliance with Hawaii's laws and regulations. Failure to correctly classify workers may lead to potential legal consequences, including penalties and back payment for overtime, leave, or benefits. Different Types of Hawaii Determining Self-Employed Independent Contractor Status: 1. Employee: An individual who works for a company under its direct control, following the company's policies and procedures, and receiving employment benefits. 2. Independent Contractor: An individual who operates their own business, providing services to multiple clients, with a higher level of control over the work performed and limited reliance on the business that contracts their services. In conclusion, determining self-employed independent contractor status in Hawaii involves carefully evaluating various factors related to behavioral control, financial control, and the nature of the working relationship. Contractors should maintain a real and independent business existence while employers must ensure proper classification to comply with labor laws. Remaining informed and seeking legal advice when necessary will help both parties navigate this complex area of Hawaii labor law.

Hawaii Determining Self-Employed Independent Contractor Status

Description

How to fill out Hawaii Determining Self-Employed Independent Contractor Status?

If you have to full, download, or printing authorized file themes, use US Legal Forms, the largest variety of authorized kinds, that can be found on the Internet. Utilize the site`s easy and handy lookup to obtain the documents you require. A variety of themes for enterprise and personal reasons are sorted by categories and claims, or search phrases. Use US Legal Forms to obtain the Hawaii Determining Self-Employed Independent Contractor Status in just a few clicks.

Should you be already a US Legal Forms buyer, log in for your bank account and click on the Download button to have the Hawaii Determining Self-Employed Independent Contractor Status. You may also entry kinds you in the past delivered electronically from the My Forms tab of your own bank account.

Should you use US Legal Forms the first time, follow the instructions under:

- Step 1. Ensure you have selected the shape for the right town/country.

- Step 2. Use the Review method to check out the form`s content. Don`t neglect to read through the outline.

- Step 3. Should you be not satisfied with the develop, use the Research area towards the top of the monitor to get other models of your authorized develop format.

- Step 4. Once you have located the shape you require, go through the Get now button. Opt for the costs plan you choose and include your references to sign up for the bank account.

- Step 5. Method the financial transaction. You can utilize your bank card or PayPal bank account to accomplish the financial transaction.

- Step 6. Pick the file format of your authorized develop and download it on the device.

- Step 7. Full, change and printing or indication the Hawaii Determining Self-Employed Independent Contractor Status.

Each authorized file format you buy is yours eternally. You possess acces to every develop you delivered electronically in your acccount. Click the My Forms portion and pick a develop to printing or download yet again.

Compete and download, and printing the Hawaii Determining Self-Employed Independent Contractor Status with US Legal Forms. There are thousands of specialist and status-particular kinds you can use for your enterprise or personal requires.

Form popularity

FAQ

A 1099 (Miscellaneous Income) form issued by the business. A narrated conversation with the employer. For FS, self-employed clients can be certified once without income verification. At the time of certification, explain to the client - in writing - that they must begin keeping income records.

What Is an Independent Contractor? An independent contractor is a self-employed person or entity contracted to perform work foror provide services toanother entity as a nonemployee. As a result, independent contractors must pay their own Social Security and Medicare taxes.

The general rule is that an individual is an independent contractor if the payer has the right to control or direct only the result of the work and not what will be done and how it will be done. If you are an independent contractor, then you are self-employed.

The basic test for determining whether a worker is an independent contractor or an employee is whether the principal has the right to control the manner and means by which the work is performed.

For the independent contractor, the company does not withhold taxes. Employment and labor laws also do not apply to independent contractors. To determine whether a person is an employee or an independent contractor, the company weighs factors to identify the degree of control it has in the relationship with the person.

Four ways to verify your income as an independent contractorIncome-verification letter. The most reliable method for proving earnings for independent contractors is a letter from a current or former employer describing your working arrangement.Contracts and agreements.Invoices.Bank statements and Pay stubs.

Becoming an independent contractor is one of the many ways to be classified as self-employed. By definition, an independent contractor provides work or services on a contractual basis, whereas, self-employment is simply the act of earning money without operating within an employee-employer relationship.

How to demonstrate that you are an independent worker on your resumeMention that time when you had to work on a project on your own.Talk about projects that required extra accountability.Describe times when you had to manage several projects all at once.More items...

Independent contractors are self-employed workers who provide services for an organisation under a contract for services. Independent contractors are not employees and are typically highly skilled, providing their clients with specialist skills or additional capacity on an as needed basis.

These factors are: (1) the kind of occupation, with reference to whether the work usually is done under the direction of a supervisor or is done by a specialist without supervision; (2) the skill required in the particular occupation; (3) whether the employer or the individual in question furnishes the equipment used