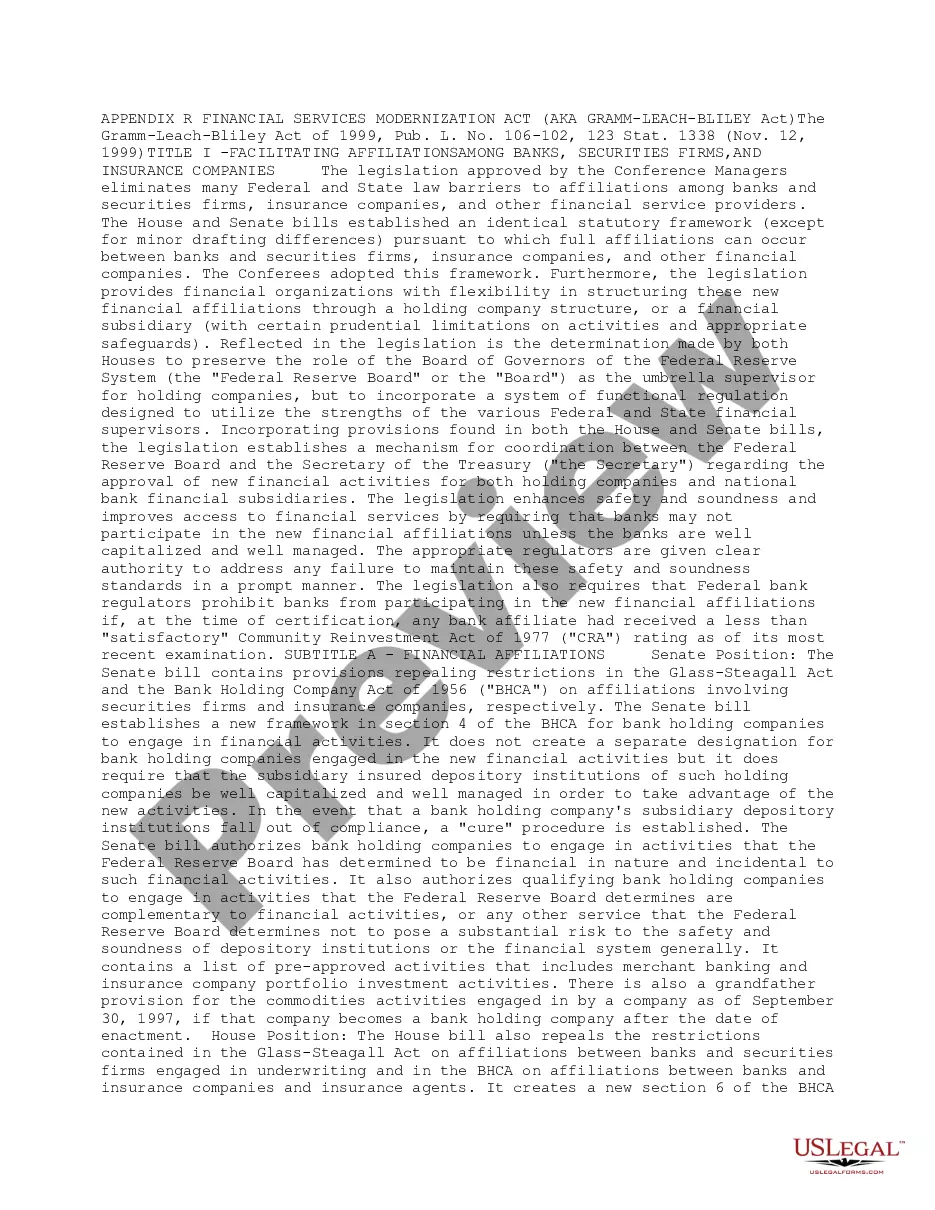

Full text and statutory guidelines for the Financial Services Modernization Act (Gramm-Leach-Bliley Act)

The Hawaii Financial Services Modernization Act, also known as the Gramm-Leach-Bliley Act (ALBA), is a significant piece of legislation that was enacted by the U.S. Congress in 1999. The act's main purpose was to update and modernize the financial services industry by removing several restrictions on the types of activities that financial institutions could engage in. This article will provide a detailed description of the Act and its key provisions, using relevant keywords. The ALBA aimed to foster competition, innovation, and efficiency within the financial sector while ensuring the privacy and security of consumers' financial information. It brought about significant changes in the regulatory framework, particularly by repealing the Glass-Steagall Act of 1933, which had imposed strict separation between commercial banking activities and investment banking activities. Under the Gramm-Leach-Bliley Act, financial institutions such as banks, insurance companies, and securities firms were allowed to form affiliations and operate as financial holding companies. This meant that a single entity could offer a variety of financial services previously separated by legal barriers. For instance, a bank could now provide insurance or investment services to its customers. One of the key pillars of the ALBA was the focus on consumer privacy and information security. The act introduced provisions requiring financial institutions to provide customers with clear notices about their privacy policies and practices. Customers were given the choice to opt-out of sharing personal information with non-affiliated third parties. Additionally, the ALBA mandated the implementation of appropriate safeguards to protect customers' non-public personal information from unauthorized access or misuse. The ALBA also established the Financial Privacy Rule and the Safeguards Rule. The Financial Privacy Rule dictates how financial institutions collect, disclose, and protect customers' personal information, while the Safeguards Rule requires them to develop and implement comprehensive information security programs to safeguard customer data. In Hawaii, the Gramm-Leach-Bliley Act applies in the same manner as it does throughout the United States. There are no specific variations or additional types of the Act specific to the state. Therefore, references to the Hawaii Financial Services Modernization Act generally point to the overarching federal legislation. Overall, the Hawaii Financial Services Modernization Act (Gramm-Leach-Bliley Act) revolutionized the financial industry by enabling greater integration and diversification of services while emphasizing consumer privacy and data security. It paved the way for the modern financial landscape we experience today, where financial institutions offer an array of services through affiliations and partnerships.The Hawaii Financial Services Modernization Act, also known as the Gramm-Leach-Bliley Act (ALBA), is a significant piece of legislation that was enacted by the U.S. Congress in 1999. The act's main purpose was to update and modernize the financial services industry by removing several restrictions on the types of activities that financial institutions could engage in. This article will provide a detailed description of the Act and its key provisions, using relevant keywords. The ALBA aimed to foster competition, innovation, and efficiency within the financial sector while ensuring the privacy and security of consumers' financial information. It brought about significant changes in the regulatory framework, particularly by repealing the Glass-Steagall Act of 1933, which had imposed strict separation between commercial banking activities and investment banking activities. Under the Gramm-Leach-Bliley Act, financial institutions such as banks, insurance companies, and securities firms were allowed to form affiliations and operate as financial holding companies. This meant that a single entity could offer a variety of financial services previously separated by legal barriers. For instance, a bank could now provide insurance or investment services to its customers. One of the key pillars of the ALBA was the focus on consumer privacy and information security. The act introduced provisions requiring financial institutions to provide customers with clear notices about their privacy policies and practices. Customers were given the choice to opt-out of sharing personal information with non-affiliated third parties. Additionally, the ALBA mandated the implementation of appropriate safeguards to protect customers' non-public personal information from unauthorized access or misuse. The ALBA also established the Financial Privacy Rule and the Safeguards Rule. The Financial Privacy Rule dictates how financial institutions collect, disclose, and protect customers' personal information, while the Safeguards Rule requires them to develop and implement comprehensive information security programs to safeguard customer data. In Hawaii, the Gramm-Leach-Bliley Act applies in the same manner as it does throughout the United States. There are no specific variations or additional types of the Act specific to the state. Therefore, references to the Hawaii Financial Services Modernization Act generally point to the overarching federal legislation. Overall, the Hawaii Financial Services Modernization Act (Gramm-Leach-Bliley Act) revolutionized the financial industry by enabling greater integration and diversification of services while emphasizing consumer privacy and data security. It paved the way for the modern financial landscape we experience today, where financial institutions offer an array of services through affiliations and partnerships.