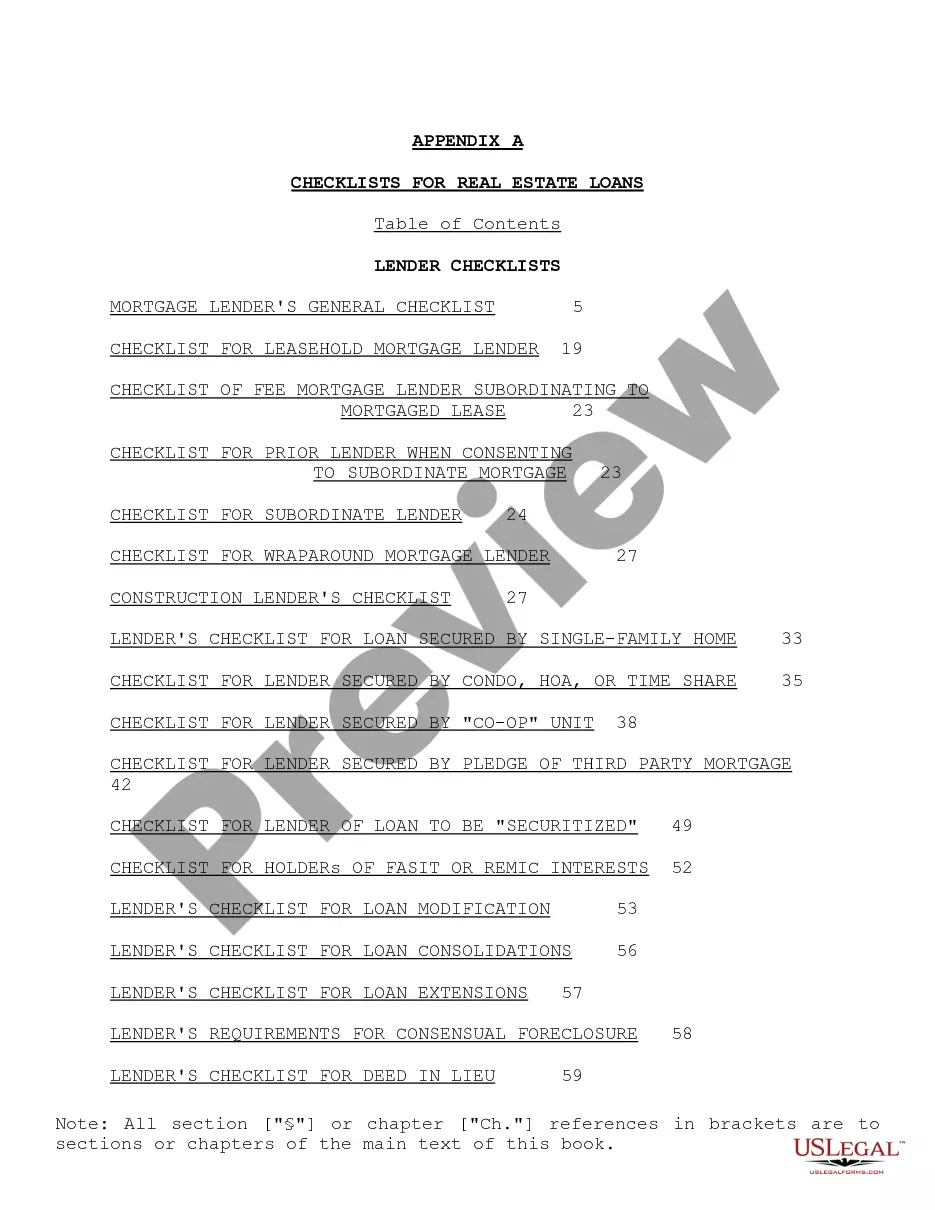

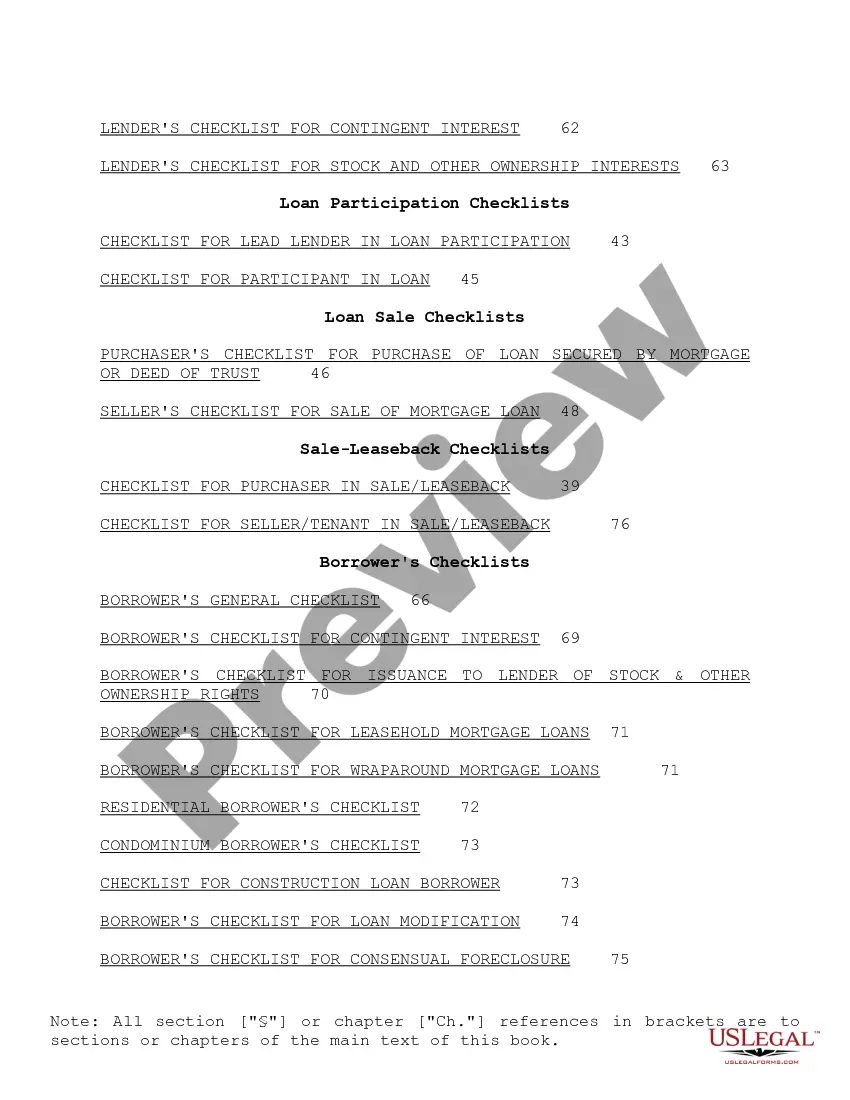

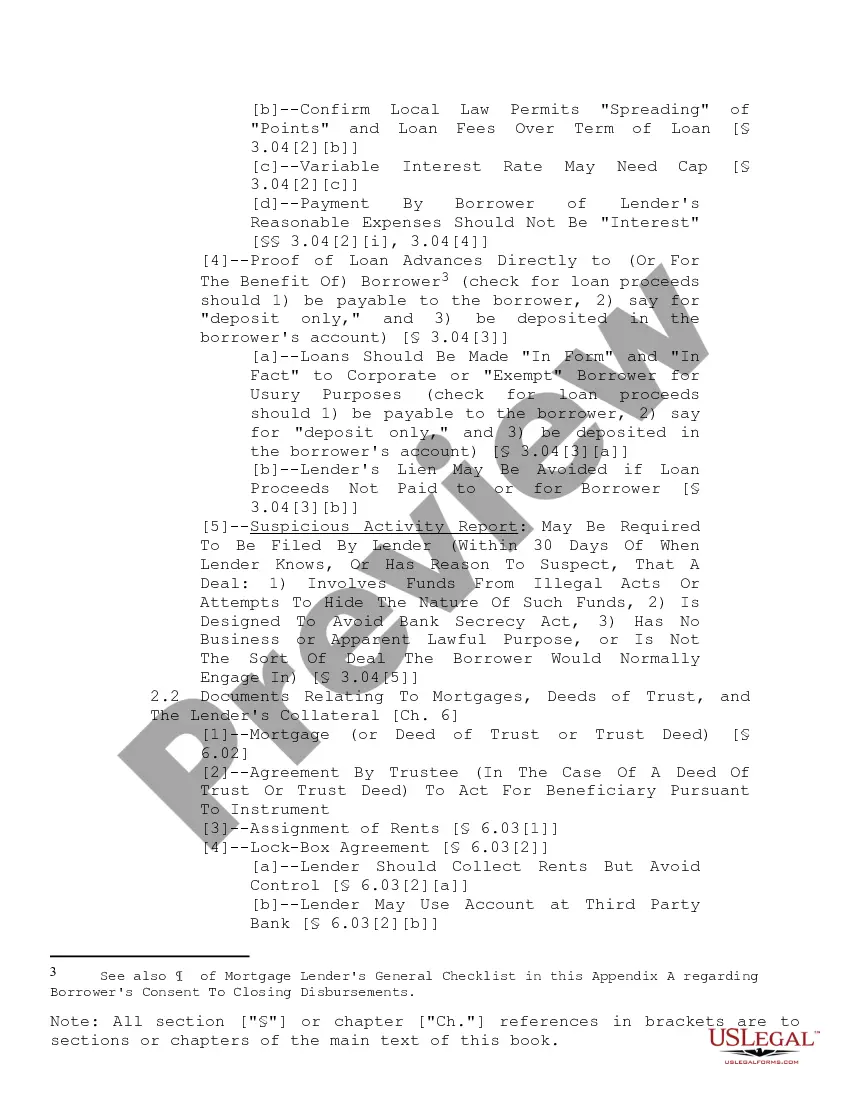

"Checklist for Real Estate Loans" is a American Lawyer Media form. This consist of many checklist that can be used for real estate loans.

Hawaii Checklist for Real Estate Loans: A Comprehensive Guide for Homebuyers When it comes to securing a real estate loan in Hawaii, it is crucial for homebuyers to be well-prepared and knowledgeable about the process. To ensure a smooth loan application and closing, it is advisable to follow a detailed Hawaii Checklist for Real Estate Loans. This comprehensive checklist acts as a helpful guide for borrowers to stay organized and cover all necessary steps throughout the loan process, mitigating the potential for any setbacks or surprises. Here is a detailed breakdown of the key components and recommended items to include on a Hawaii Checklist for Real Estate Loans: 1. Mortgage Pre-qualification: Initiating the loan process by obtaining pre-qualification from a reliable mortgage lender allows homebuyers to assess their affordability and understand their borrowing capacity. 2. Credit Check: Reviewing credit reports and scores is essential. Ensure there are no inaccuracies or issues that could negatively impact loan applications. 3. Organize Financial Documents: Gather vital documents required for loan applications such as pay stubs, tax returns, bank statements, and investment account statements. Maintaining proper records greatly expedites the approval process. 4. Down Payment Savings: Determine the amount of down payment required for the desired property. Saving diligently for this purpose is vital, as it contributes to a stronger loan application. 5. Budget for Closing Costs: Estimate the closing costs, including appraisal fees, title insurance, inspection fees, and other expenses that are typically associated with real estate transactions. 6. Research Loan Options: Hawaii offers various types of loans. Educate yourself about the available options such as conventional loans, FHA loans, VA loans, and USDA loans to determine which suits your needs best. 7. Mortgage Rates and Terms: Study the prevailing mortgage interest rates and loan terms offered by different lenders to secure the most favorable conditions. This research can be done online or by consulting with a mortgage broker or loan officer. 8. Obtain Loan Pre-approval: Once all documents are in order, complete a loan pre-approval application with a preferred lender. This vital step provides homebuyers with a pre-approved loan amount, enhancing their credibility during negotiations. 9. Engage a Real Estate Agent: Collaborating with a knowledgeable real estate agent specializing in the Hawaii market will assist in finding suitable properties that match your criteria and budget. They leverage their expertise to negotiate the best deal on your behalf. 10. Real Estate Property Research: Conduct detailed research on potential properties, assessing factors such as location, neighborhood amenities, proximity to schools, transport links, and future development plans. This ensures an informed decision-making process. 11. Home Inspection: Before finalizing any purchase, engage a professional home inspector to thoroughly evaluate the property for any structural issues, potential repairs, or maintenance concerns. This protects buyers from unexpected expenses down the line. 12. Appraisal: As part of the loan process, the lender will arrange for an independent appraisal to determine the market value of the property. Understanding this value is crucial for loan approval and avoiding overpaying. 13. Secure Homeowner's Insurance: Identify a reputable insurance provider and obtain homeowners' insurance, as it is typically a prerequisite for loan approval and safeguards the property investment. 14. Final Loan Approval: After satisfying all lender requirements, the loan undergoes final approval, finalizing the terms and conditions for the mortgage loan. 15. Closing Process: Coordinate with your lender, real estate agent, and attorney/title company to complete all necessary paperwork and formalities during the closing process. Be sure to review all documents thoroughly before signing. Some specific types of real estate loans in Hawaii include: 1. Conventional Loans: These are traditional mortgage loans often requiring a down payment and good credit standing. 2. FHA Loans: Backed by the Federal Housing Administration, FHA loans are popular for first-time homebuyers due to lower down payment requirements and more flexible credit criteria. 3. VA Loans: Exclusively available to eligible active or retired military personnel, VA loans offer competitive rates, zero down payment options, and reduced fees. 4. USDA Loans: The United States Department of Agriculture supports USDA loans, providing incentives for eligible homebuyers in rural areas to purchase homes with minimal down payments. By following this comprehensive Hawaii Checklist for Real Estate Loans, potential homebuyers can navigate the loan process effectively, ensuring a seamless and successful real estate purchase in Hawaii.Hawaii Checklist for Real Estate Loans: A Comprehensive Guide for Homebuyers When it comes to securing a real estate loan in Hawaii, it is crucial for homebuyers to be well-prepared and knowledgeable about the process. To ensure a smooth loan application and closing, it is advisable to follow a detailed Hawaii Checklist for Real Estate Loans. This comprehensive checklist acts as a helpful guide for borrowers to stay organized and cover all necessary steps throughout the loan process, mitigating the potential for any setbacks or surprises. Here is a detailed breakdown of the key components and recommended items to include on a Hawaii Checklist for Real Estate Loans: 1. Mortgage Pre-qualification: Initiating the loan process by obtaining pre-qualification from a reliable mortgage lender allows homebuyers to assess their affordability and understand their borrowing capacity. 2. Credit Check: Reviewing credit reports and scores is essential. Ensure there are no inaccuracies or issues that could negatively impact loan applications. 3. Organize Financial Documents: Gather vital documents required for loan applications such as pay stubs, tax returns, bank statements, and investment account statements. Maintaining proper records greatly expedites the approval process. 4. Down Payment Savings: Determine the amount of down payment required for the desired property. Saving diligently for this purpose is vital, as it contributes to a stronger loan application. 5. Budget for Closing Costs: Estimate the closing costs, including appraisal fees, title insurance, inspection fees, and other expenses that are typically associated with real estate transactions. 6. Research Loan Options: Hawaii offers various types of loans. Educate yourself about the available options such as conventional loans, FHA loans, VA loans, and USDA loans to determine which suits your needs best. 7. Mortgage Rates and Terms: Study the prevailing mortgage interest rates and loan terms offered by different lenders to secure the most favorable conditions. This research can be done online or by consulting with a mortgage broker or loan officer. 8. Obtain Loan Pre-approval: Once all documents are in order, complete a loan pre-approval application with a preferred lender. This vital step provides homebuyers with a pre-approved loan amount, enhancing their credibility during negotiations. 9. Engage a Real Estate Agent: Collaborating with a knowledgeable real estate agent specializing in the Hawaii market will assist in finding suitable properties that match your criteria and budget. They leverage their expertise to negotiate the best deal on your behalf. 10. Real Estate Property Research: Conduct detailed research on potential properties, assessing factors such as location, neighborhood amenities, proximity to schools, transport links, and future development plans. This ensures an informed decision-making process. 11. Home Inspection: Before finalizing any purchase, engage a professional home inspector to thoroughly evaluate the property for any structural issues, potential repairs, or maintenance concerns. This protects buyers from unexpected expenses down the line. 12. Appraisal: As part of the loan process, the lender will arrange for an independent appraisal to determine the market value of the property. Understanding this value is crucial for loan approval and avoiding overpaying. 13. Secure Homeowner's Insurance: Identify a reputable insurance provider and obtain homeowners' insurance, as it is typically a prerequisite for loan approval and safeguards the property investment. 14. Final Loan Approval: After satisfying all lender requirements, the loan undergoes final approval, finalizing the terms and conditions for the mortgage loan. 15. Closing Process: Coordinate with your lender, real estate agent, and attorney/title company to complete all necessary paperwork and formalities during the closing process. Be sure to review all documents thoroughly before signing. Some specific types of real estate loans in Hawaii include: 1. Conventional Loans: These are traditional mortgage loans often requiring a down payment and good credit standing. 2. FHA Loans: Backed by the Federal Housing Administration, FHA loans are popular for first-time homebuyers due to lower down payment requirements and more flexible credit criteria. 3. VA Loans: Exclusively available to eligible active or retired military personnel, VA loans offer competitive rates, zero down payment options, and reduced fees. 4. USDA Loans: The United States Department of Agriculture supports USDA loans, providing incentives for eligible homebuyers in rural areas to purchase homes with minimal down payments. By following this comprehensive Hawaii Checklist for Real Estate Loans, potential homebuyers can navigate the loan process effectively, ensuring a seamless and successful real estate purchase in Hawaii.