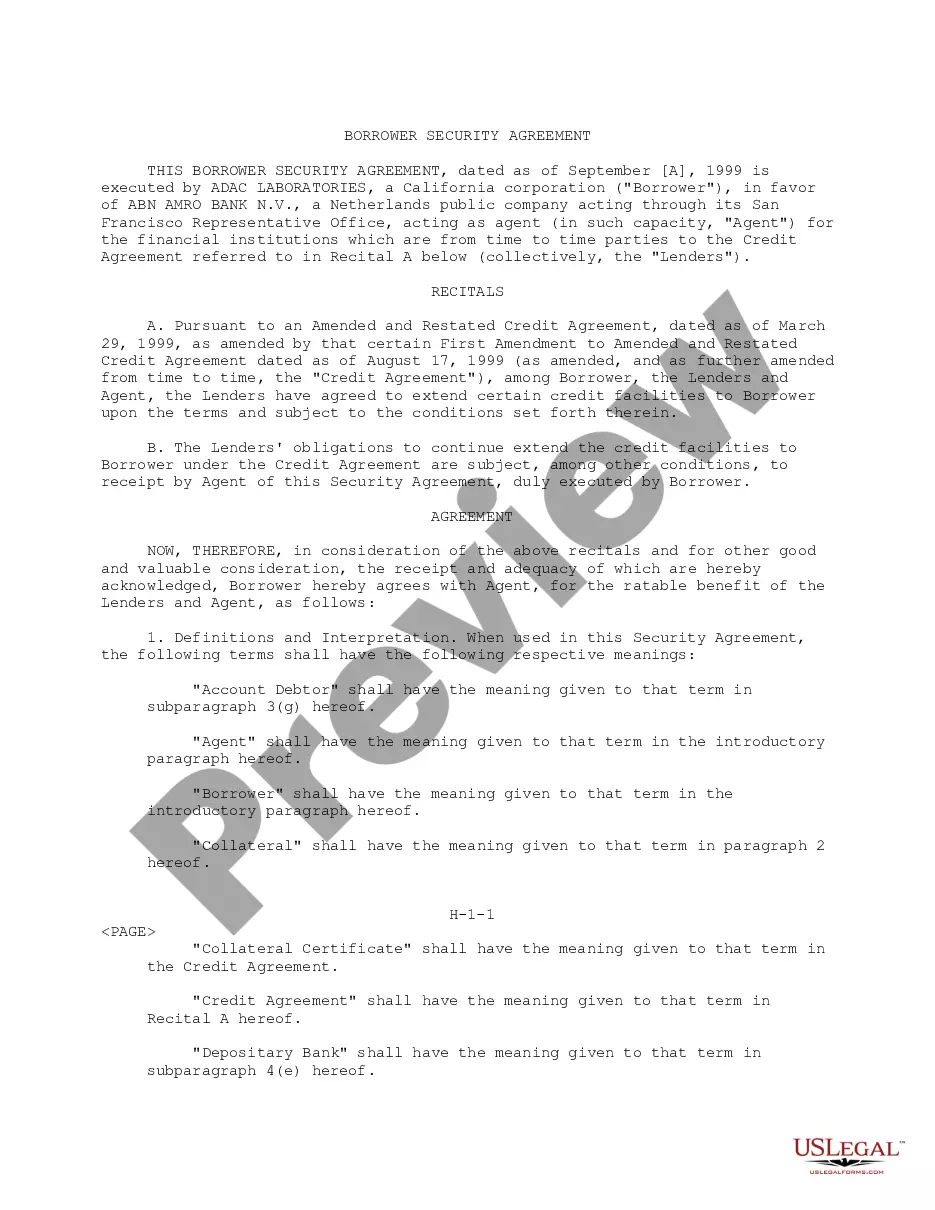

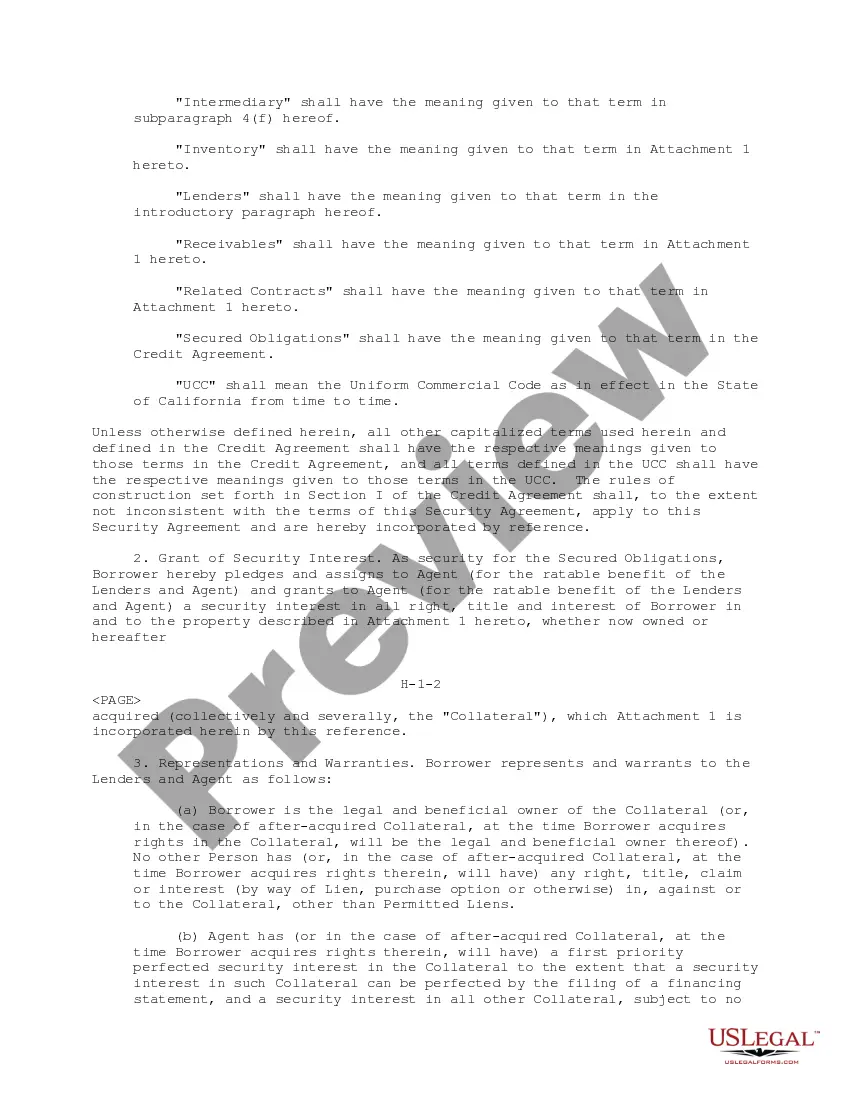

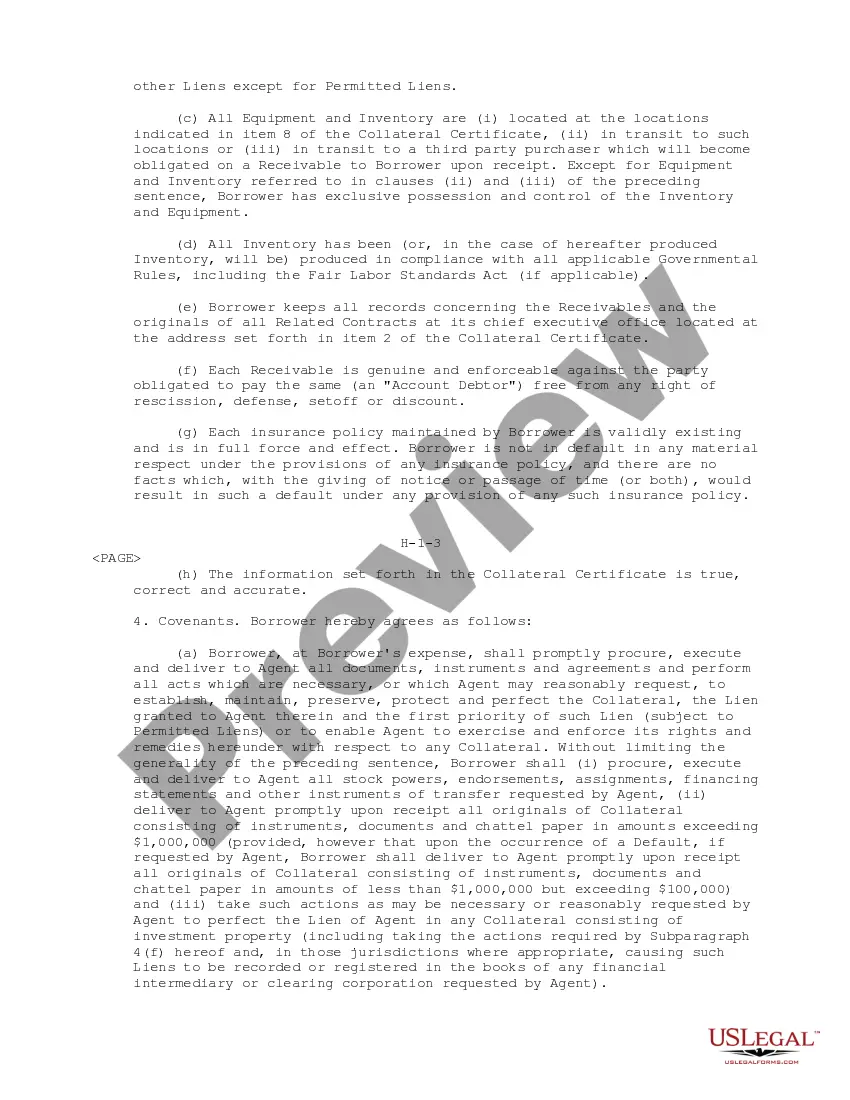

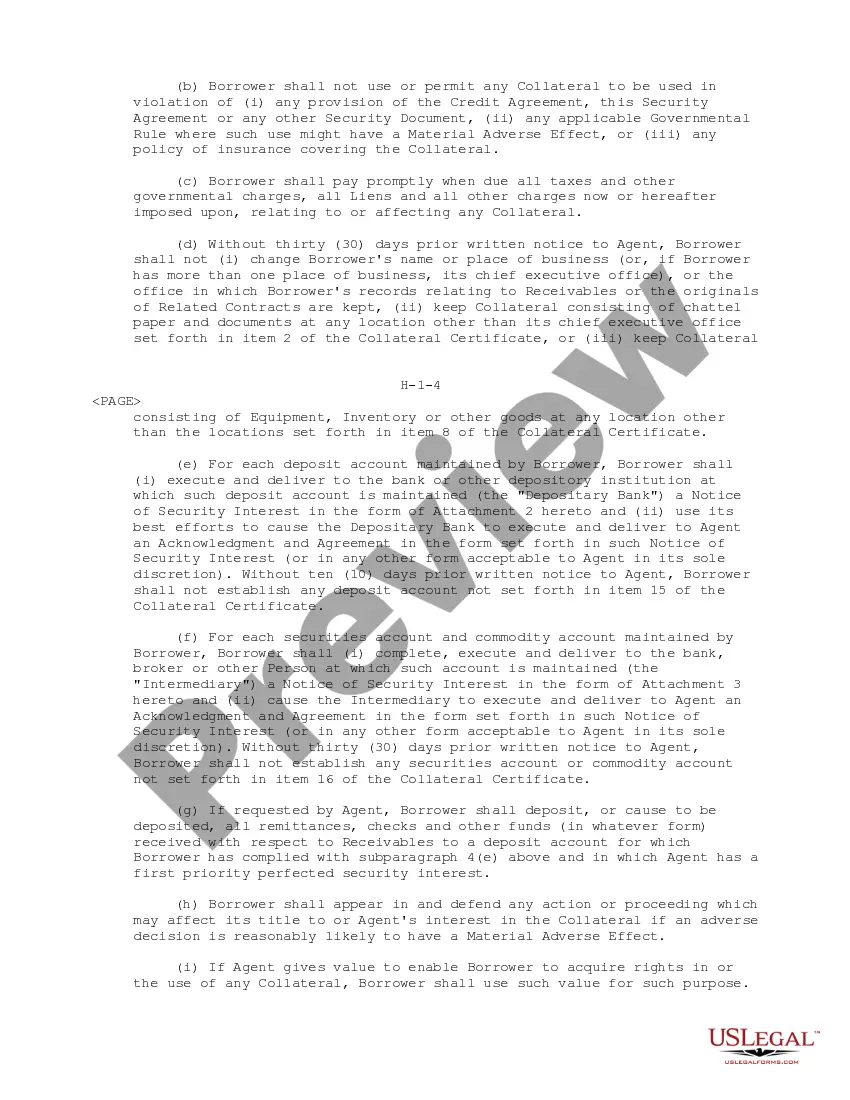

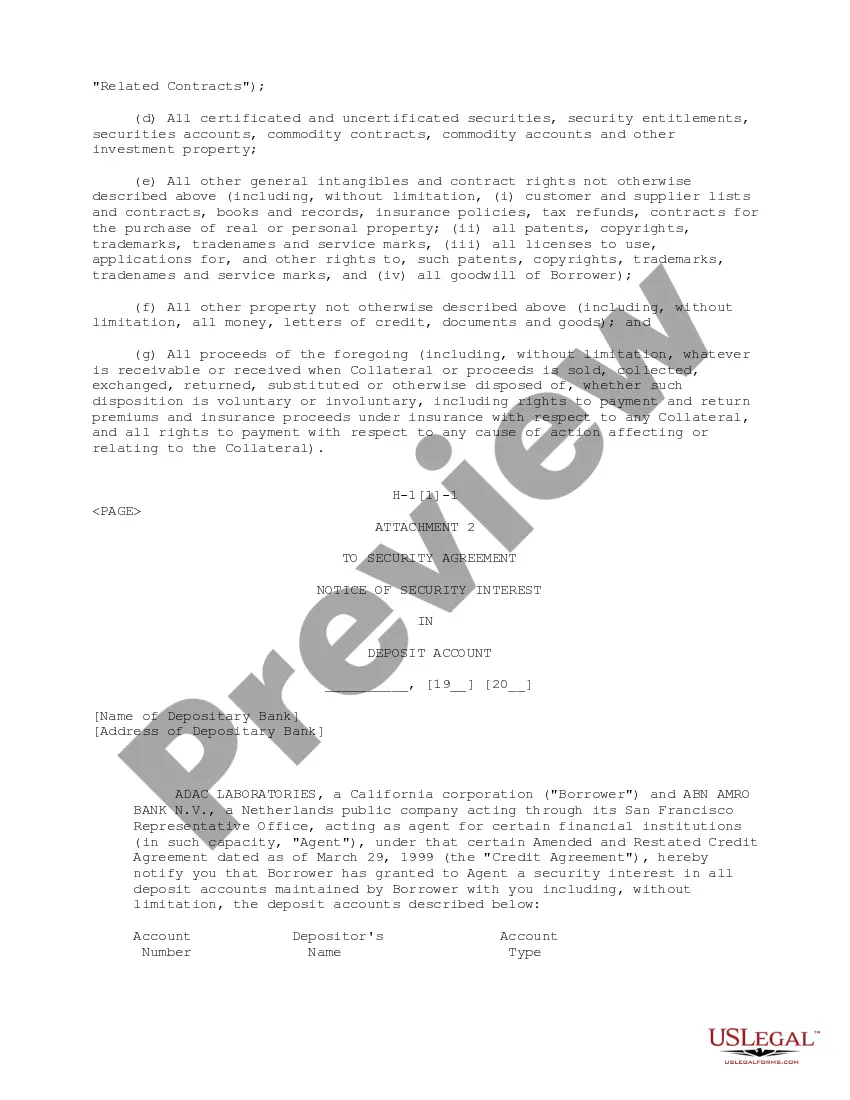

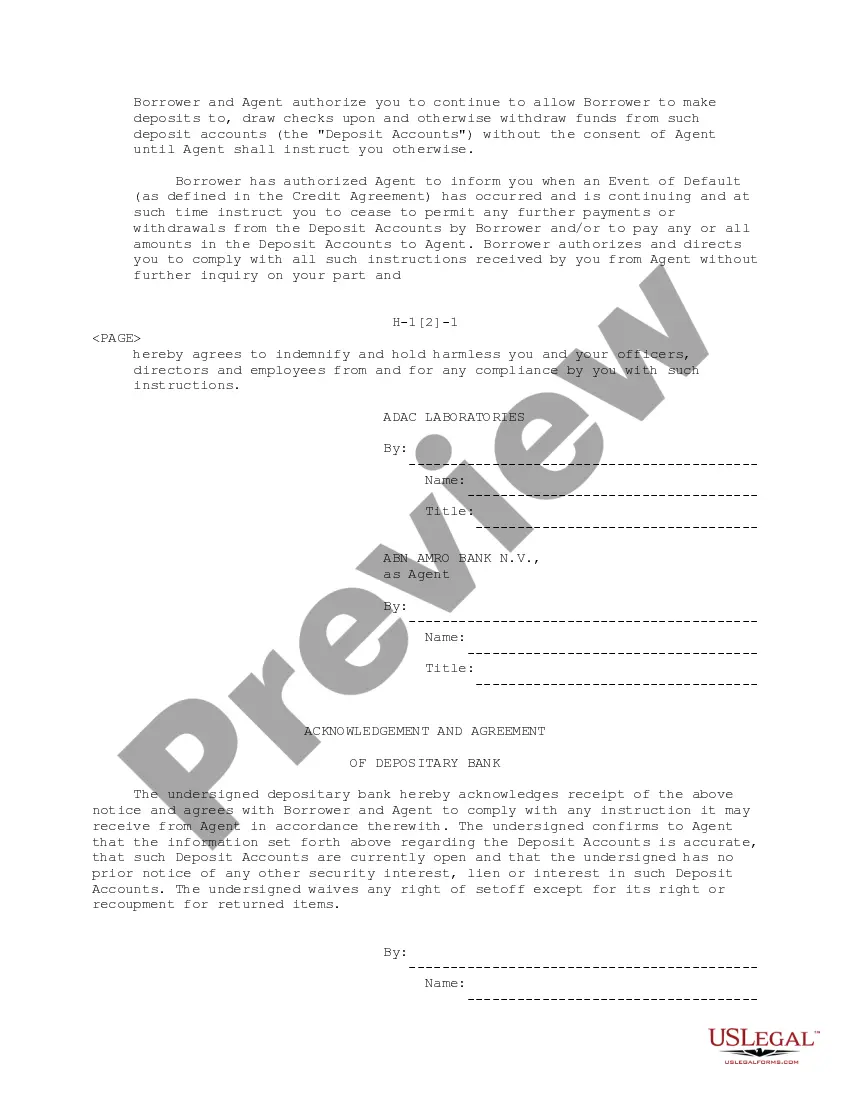

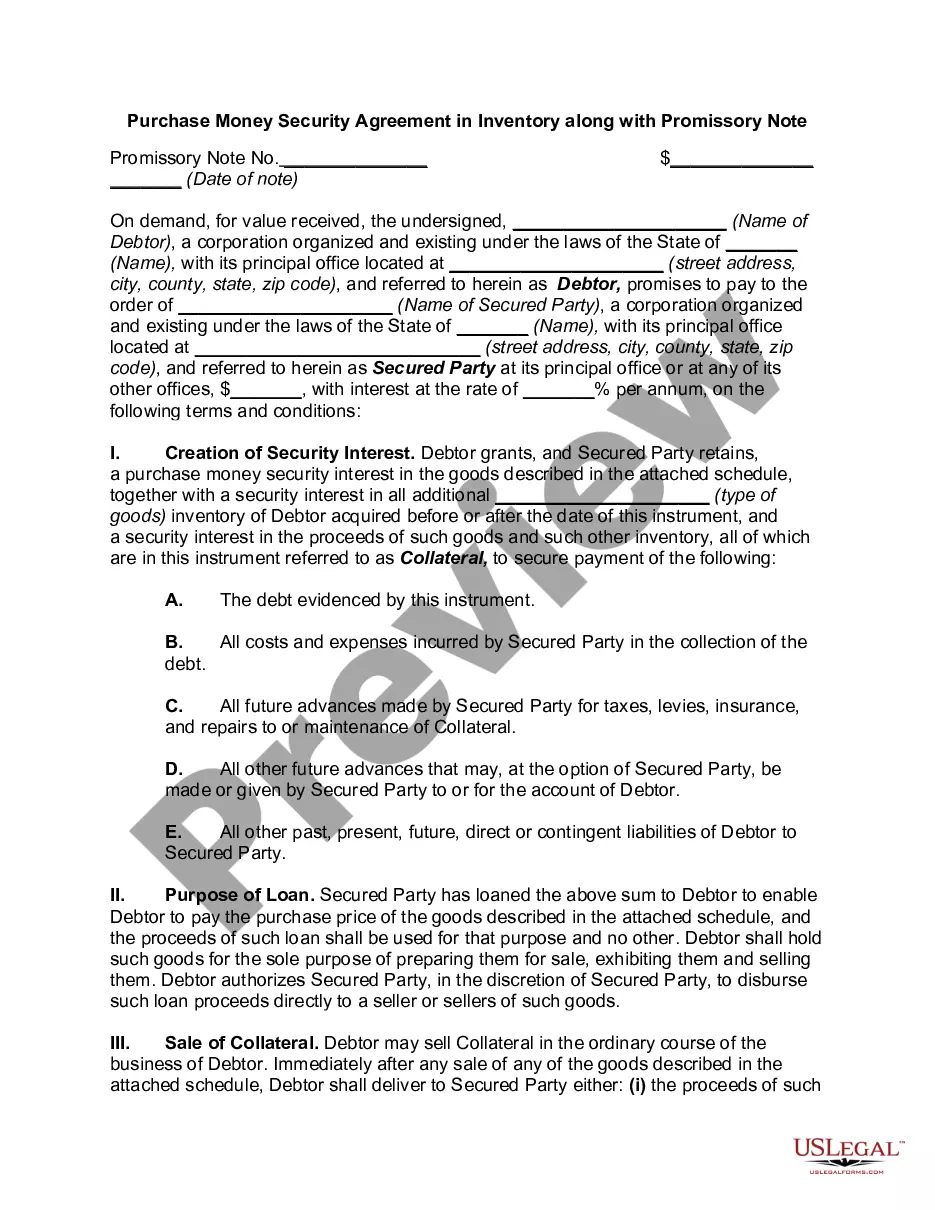

The Hawaii Borrower Security Agreement is a legally binding document that outlines the terms and conditions regarding the extension of credit facilities to borrowers in the state of Hawaii. This agreement is designed to protect the lender's interests by establishing a security interest in certain assets of the borrower, which can be used as collateral in the event of default. The Hawaii Borrower Security Agreement is applicable to various types of credit facilities, including loans, lines of credit, and other forms of credit extensions. It is crucial for borrowers to thoroughly understand the implications and requirements set forth in this agreement before entering into any credit arrangement. The key elements covered in the Hawaii Borrower Security Agreement may include: 1. Collateral: The agreement specifies the assets or property that will serve as collateral. This can include real estate, vehicles, inventory, accounts receivable, or other valuable assets that can be easily liquidated in the event of default. 2. Grant of Security Interest: The borrower grants the lender a security interest in the designated collateral, providing the lender with the right to repossess and sell the assets if the borrower fails to meet their financial obligations. 3. Perfection of Security Interest: The agreement outlines the steps necessary for the lender to perfect their security interest, which typically includes the filing of a UCC-1 financing statement with the appropriate state agency. This step ensures that the lender's claim to the collateral takes priority over other creditors. 4. Default and Remedies: The agreement specifies the conditions that constitute a default, such as missed payments, breach of covenants, or insolvency. It also outlines the remedies available to the lender in the event of default, such as repossession, foreclosure, or legal action. 5. Representations and Warranties: The borrower typically makes certain representations and warranties regarding the collateral, ensuring that they have the legal right to pledge the assets and that there are no other claims or encumbrances on them. Types of Hawaii Borrower Security Agreements regarding the extension of credit facilities may include: 1. Real Estate Mortgage: This agreement specifically pertains to credit facilities granted for the purchase or refinancing of real estate properties, where the property itself serves as collateral. 2. Chattel Mortgage: This agreement is used when personal property, such as equipment, vehicles, or inventory, is pledged as collateral for a credit facility. 3. Accounts Receivable Financing Agreement: This type of agreement is applicable when a borrower uses their accounts receivable as collateral to secure a credit extension. It is important for borrowers in Hawaii to carefully review and understand the specific terms within their Borrower Security Agreement, as different types of credit facilities may have unique requirements and provisions. Consulting with legal professionals or financial advisors is advisable to ensure compliance with the agreement and protect both parties' interests.

Hawaii Borrower Security Agreement regarding the extension of credit facilities

Description

How to fill out Hawaii Borrower Security Agreement Regarding The Extension Of Credit Facilities?

Choosing the best authorized papers template could be a have difficulties. Naturally, there are a variety of templates accessible on the Internet, but how can you find the authorized develop you require? Make use of the US Legal Forms website. The support delivers a large number of templates, including the Hawaii Borrower Security Agreement regarding the extension of credit facilities, that can be used for company and personal requirements. All of the types are checked out by pros and meet up with state and federal demands.

If you are currently listed, log in to the profile and click on the Obtain switch to get the Hawaii Borrower Security Agreement regarding the extension of credit facilities. Use your profile to appear from the authorized types you possess ordered previously. Proceed to the My Forms tab of your own profile and get an additional version from the papers you require.

If you are a new end user of US Legal Forms, listed here are easy directions so that you can comply with:

- First, ensure you have chosen the proper develop for the area/region. You are able to look over the shape utilizing the Preview switch and browse the shape description to guarantee it will be the right one for you.

- In case the develop is not going to meet up with your preferences, utilize the Seach industry to obtain the appropriate develop.

- When you are certain that the shape is acceptable, go through the Get now switch to get the develop.

- Opt for the costs prepare you want and enter in the essential info. Create your profile and pay money for the order making use of your PayPal profile or Visa or Mastercard.

- Choose the document file format and down load the authorized papers template to the device.

- Complete, edit and produce and indicator the obtained Hawaii Borrower Security Agreement regarding the extension of credit facilities.

US Legal Forms may be the greatest catalogue of authorized types that you can see various papers templates. Make use of the service to down load skillfully-manufactured papers that comply with state demands.