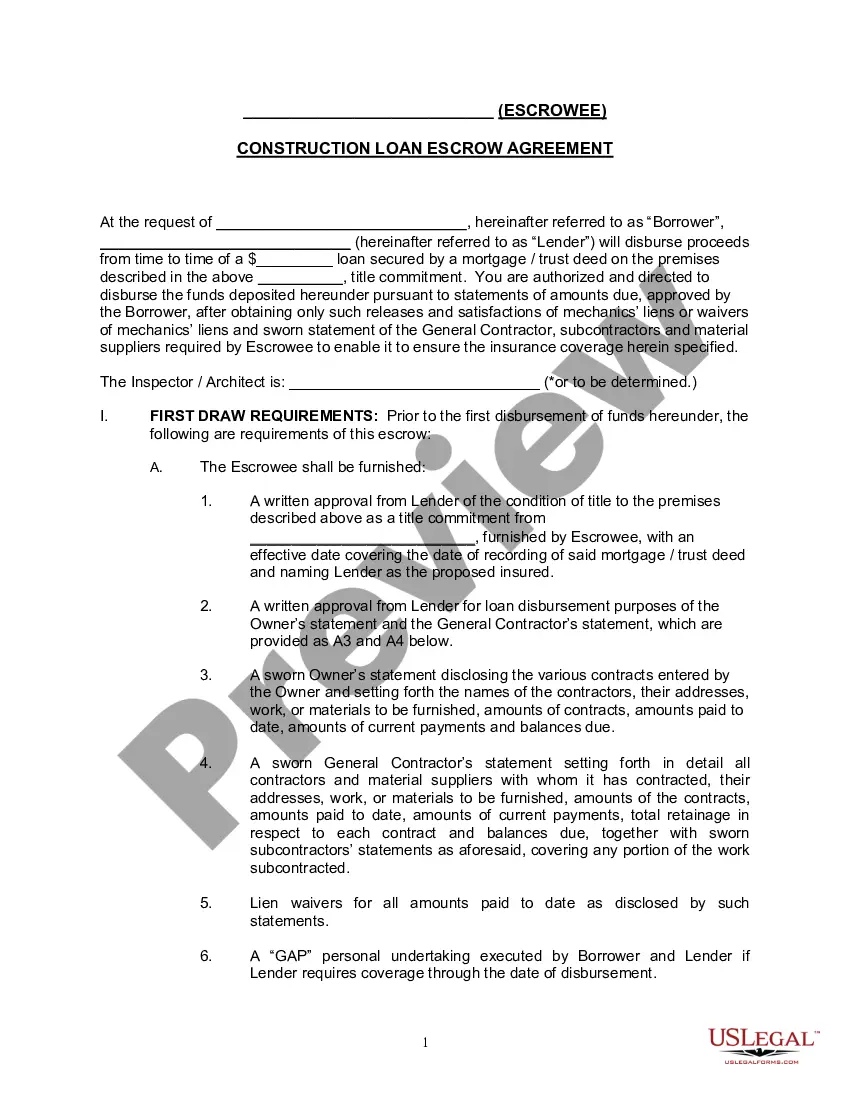

"A construction loan agreement isa legally binding contract between the lender and the borrower, detailing the promises and commitments both parties have to uphold through successful project completion.

A Loan Agreement is a document between a borrower and lender that details the loan repayment schedule.

The Loan Agreement protects the lender by enforcing the borrower's pledge to repay the loan; payment via regular payments or lump sums. The borrower may also find the loan contract useful because it records the details of the loan for their records and helps keep track of payments.

Loan agreements generally include information about:

* The location.

* The loan amount.

* Interest and late fees.

* Repayment method.

* Collateral and insurance."

Hawaii Construction Loan Agreement

Category:

State:

Multi-State

Control #:

US-ENTREP-0065-1

Format:

Word;

Rich Text

Instant download

Description

Free preview

How to fill out Construction Loan Agreement?

US Legal Forms - one of the most significant libraries of authorized forms in America - delivers an array of authorized record layouts you can download or print. Utilizing the internet site, you can find a large number of forms for business and personal reasons, categorized by classes, says, or search phrases.You can find the newest models of forms just like the Hawaii Construction Loan Agreement within minutes.

If you already have a monthly subscription, log in and download Hawaii Construction Loan Agreement from your US Legal Forms local library. The Acquire option will show up on each and every kind you see. You have accessibility to all in the past saved forms inside the My Forms tab of your profile.

In order to use US Legal Forms the very first time, listed below are simple recommendations to obtain started off:

- Ensure you have chosen the best kind for your city/area. Select the Preview option to examine the form`s content material. Look at the kind outline to ensure that you have selected the appropriate kind.

- In case the kind does not match your specifications, take advantage of the Search area towards the top of the display to discover the the one that does.

- In case you are content with the form, confirm your option by clicking the Acquire now option. Then, opt for the prices strategy you like and provide your references to sign up for the profile.

- Method the transaction. Use your bank card or PayPal profile to perform the transaction.

- Pick the formatting and download the form on your product.

- Make adjustments. Fill up, revise and print and signal the saved Hawaii Construction Loan Agreement.

Every web template you included in your account does not have an expiration day and is also the one you have permanently. So, in order to download or print an additional copy, just visit the My Forms portion and click on on the kind you will need.

Obtain access to the Hawaii Construction Loan Agreement with US Legal Forms, probably the most extensive local library of authorized record layouts. Use a large number of skilled and express-certain layouts that satisfy your small business or personal demands and specifications.

Form popularity

FAQ

A construction loan agreement is a legally binding contract between the lender and the borrower, detailing the promises and commitments both parties have to uphold through successful project completion.

Loan agreements typically include covenants, value of collateral involved, guarantees, interest rate terms and the duration over which it must be repaid. Default terms should be clearly detailed to avoid confusion or potential legal court action.

Usually, an IOU and a promissory note form are only signed by the borrower, although they may be signed by both parties. A loan agreement is a single document that contains all of the terms of the loan, and is signed by both parties.

Understanding the Important Clauses in a Loan Agreement #1: Fluctuation Of Interest Rates Clause: ... #2: 'Default' Definition Clause: ... #3: Security Cover Clause: ... #4: Disbursement Clause: ... #5: Force Majeure Clause: ... #6: Reset Clause: ... #7: Prepayment Clause: ... #8: Other Balances Set Off Clause:

If you're going to create a personal loan agreement from the ground up, it should include the following information: Legal names and address of both parties. Names and address of the loan cosigner (if applicable). Amount to be borrowed. Date the loan is to be provided.

Loan agreements typically include covenants, value of collateral involved, guarantees, interest rate terms and the duration over which it must be repaid.

No, entering into a valid loan agreement does not necessarily mean that you are approved for the loan. This is a scenario that borrowers will face when applying for a loan through a financial institution like a bank. Typically, the loan approval process begins with the borrower requesting a loan from a lender.

Loan terms refer to the terms and conditions involved when borrowing money. This can include the loan's repayment period, the interest rate and fees associated with the loan, penalty fees borrowers might be charged, and any other special conditions that may apply.