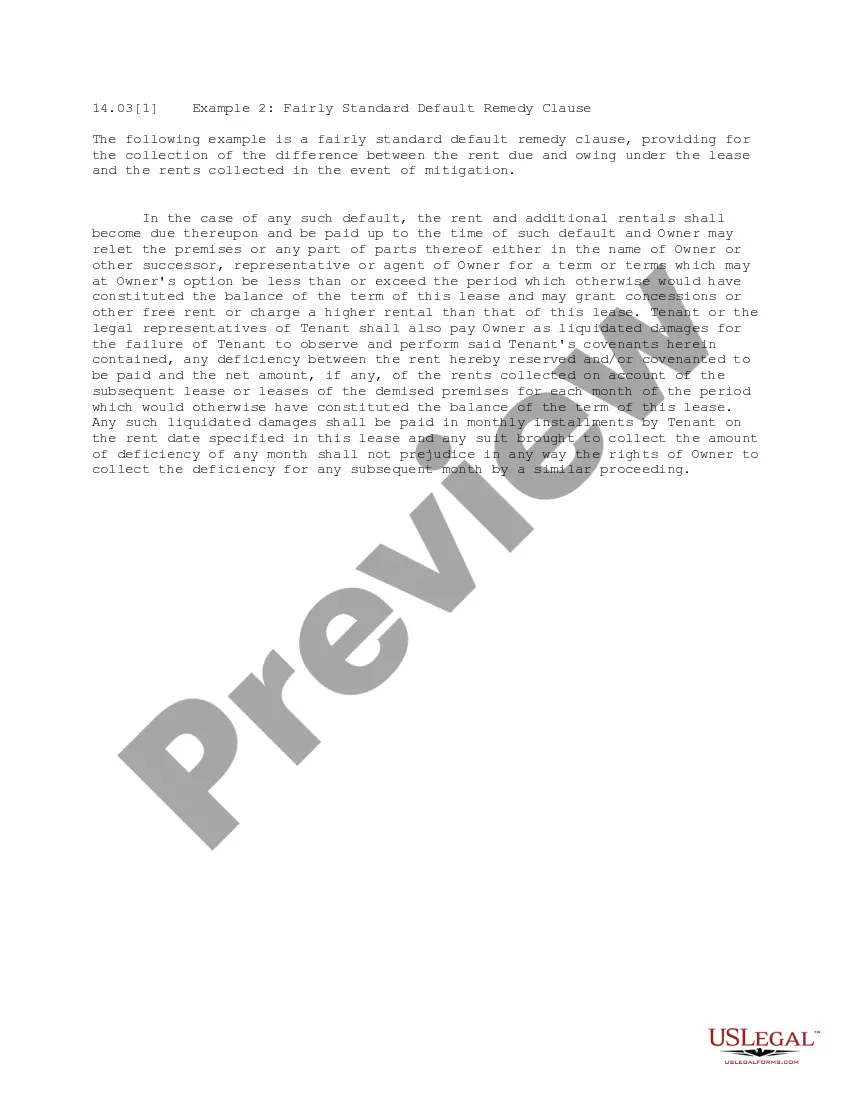

This office lease clause is an onerous approach to a default remedies clause. This clause is similar to those found in many New York City landlord office lease forms.

Hawaii Onerous Approach to Default Remedy Clause

Category:

State:

Multi-State

Control #:

US-OL14032

Format:

Word;

PDF

Instant download

Description

Free preview

How to fill out Onerous Approach To Default Remedy Clause?

US Legal Forms - one of several most significant libraries of authorized forms in the States - provides a variety of authorized document templates it is possible to down load or printing. Utilizing the website, you will get a large number of forms for business and person functions, sorted by types, suggests, or search phrases.You can find the latest variations of forms just like the Hawaii Onerous Approach to Default Remedy Clause within minutes.

If you already possess a monthly subscription, log in and down load Hawaii Onerous Approach to Default Remedy Clause from the US Legal Forms library. The Obtain button will show up on every type you view. You gain access to all earlier downloaded forms within the My Forms tab of your respective account.

In order to use US Legal Forms for the first time, listed below are straightforward recommendations to help you started off:

- Be sure to have picked out the best type for your metropolis/state. Go through the Review button to analyze the form`s content. See the type explanation to actually have chosen the appropriate type.

- When the type doesn`t suit your needs, make use of the Research industry at the top of the display to find the one who does.

- In case you are satisfied with the shape, verify your option by clicking the Buy now button. Then, choose the costs prepare you prefer and offer your accreditations to sign up for an account.

- Process the deal. Make use of Visa or Mastercard or PayPal account to accomplish the deal.

- Find the structure and down load the shape on your own gadget.

- Make adjustments. Complete, revise and printing and indication the downloaded Hawaii Onerous Approach to Default Remedy Clause.

Each template you included with your bank account lacks an expiry particular date and is yours for a long time. So, if you want to down load or printing another version, just go to the My Forms section and click on around the type you will need.

Obtain access to the Hawaii Onerous Approach to Default Remedy Clause with US Legal Forms, by far the most comprehensive library of authorized document templates. Use a large number of skilled and express-specific templates that meet your small business or person requirements and needs.

Form popularity

FAQ

A ?default? is a failure to comply with a provision in the lease. ?Curing? or ?remedying? the default means correcting the failure or omission. A common example is a failure to pay the rent on time.

In contract law, a breach means the failure of a contracting party to perform their obligations ing to the terms of the agreement. Default, ing to the law of obligations and banking law, means to refuse to pay a debt when due.

The Agreement has several available remedies for the buyer and seller in the event of default. The options include (1) declaring the Agreement null and void, (2) termination of the Agreement, (3) specific performance, and (4) stipulated damages.

Default Remedies means all rights and remedies of any Secured Party in respect of any Common Collateral, whether arising pursuant to the DIP Credit Agreements, the Collateral Documents, the Orders or applicable law, the exercise of which is contingent upon the occurrence and continuation of an Event of Default (as ...

The Holder, in addition to being entitled to exercise all rights granted by law, including recovery of damages, shall be entitled to specific performance of its rights under this Agreement.

Typical events of default in loan agreements include non-payment or late payment of amounts due, breach of certain material representations and warranties or covenants, cross-default, breach of change of control provisions, and insolvency.