Iowa Agreement for Purchase of Business Assets from a Corporation

Description

How to fill out Agreement For Purchase Of Business Assets From A Corporation?

US Legal Forms - one of the biggest libraries of lawful varieties in the United States - offers a wide array of lawful file templates you are able to obtain or printing. While using internet site, you will get 1000s of varieties for organization and individual purposes, sorted by groups, says, or keywords and phrases.You will discover the most up-to-date types of varieties like the Iowa Agreement for Purchase of Business Assets from a Corporation in seconds.

If you already have a registration, log in and obtain Iowa Agreement for Purchase of Business Assets from a Corporation through the US Legal Forms local library. The Obtain switch can look on each and every form you look at. You have accessibility to all formerly downloaded varieties from the My Forms tab of your respective accounts.

In order to use US Legal Forms for the first time, listed below are simple instructions to help you began:

- Be sure to have selected the proper form to your area/state. Go through the Review switch to check the form`s information. See the form information to actually have chosen the appropriate form.

- If the form does not fit your demands, take advantage of the Research discipline at the top of the monitor to get the one that does.

- If you are satisfied with the form, validate your choice by clicking the Buy now switch. Then, opt for the rates plan you prefer and provide your accreditations to register for the accounts.

- Approach the deal. Utilize your Visa or Mastercard or PayPal accounts to perform the deal.

- Pick the format and obtain the form in your product.

- Make alterations. Fill up, change and printing and signal the downloaded Iowa Agreement for Purchase of Business Assets from a Corporation.

Each design you included with your bank account does not have an expiry time and is yours permanently. So, if you would like obtain or printing another backup, just go to the My Forms area and then click in the form you require.

Obtain access to the Iowa Agreement for Purchase of Business Assets from a Corporation with US Legal Forms, the most comprehensive local library of lawful file templates. Use 1000s of specialist and state-distinct templates that satisfy your business or individual demands and demands.

Form popularity

FAQ

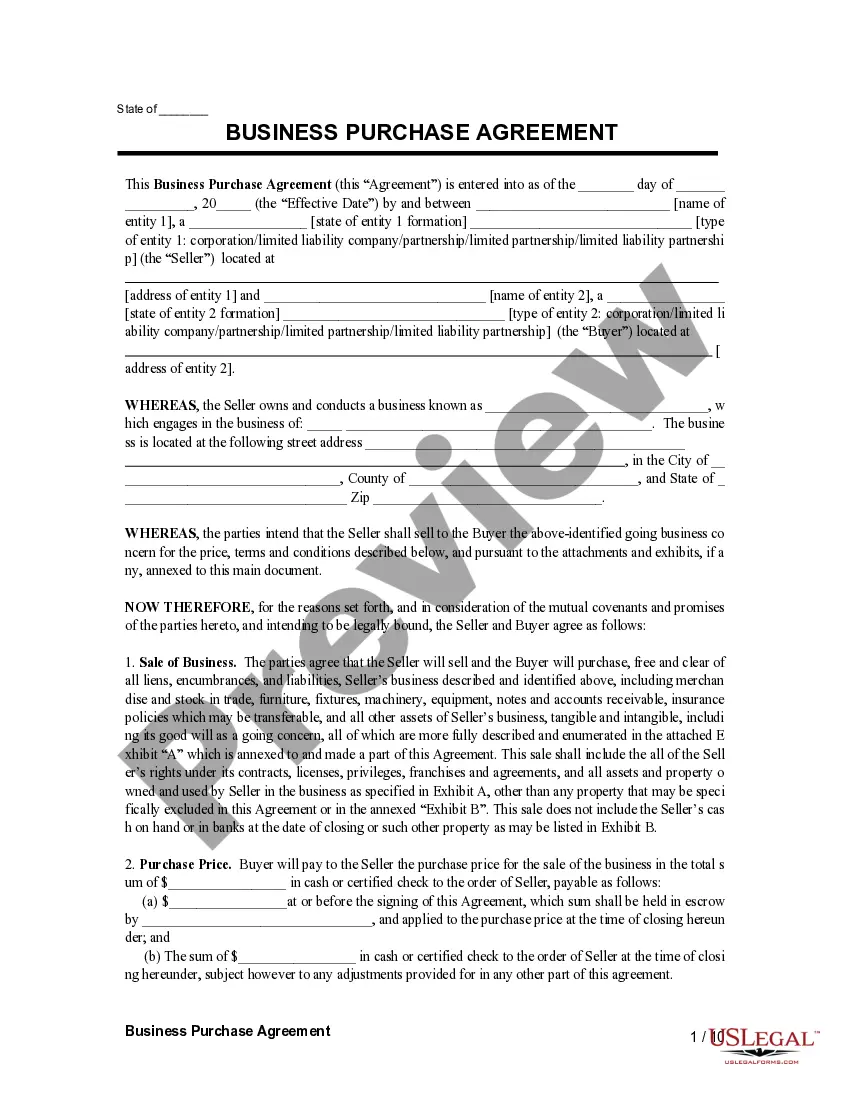

How to Write a Business Purchase Agreement? Step 1 ? Parties and Business Information. A business purchase agreement should detail the names of the buyer and seller at the start of the contract. ... Step 2 ? Business Assets. ... Step 3 ? Business Liabilities. ... Step 4 ? Purchase Price. ... Step 5 ? Terms. ... Step 6 ? Signatures.

At its most basic, a purchase agreement should include the following: Name and contact information for buyer and seller. The address of the property being sold. The price to be paid for the property. The date of transfer. Disclosures. Contingencies. Signatures.

Either the seller or the buyer can prepare a purchase agreement. Like any contract, it can be a standard document that one party uses in the normal course of business or it can be the end result of back-and-forth negotiations.

A business purchase agreement is a written contract between two (2) parties wherein one party agrees to buy the other party's company for a specific price. By drafting the legal document, each party warrants and agrees to a set of binding conditions that are enforceable in ance with state law.

All business contracts should include fundamentals such as: The date of the contract. The names of all parties or entities involved. Payment amounts and due dates. Contract expiration dates. Potential damages for breach of contract, missed deadlines or incomplete services.

A purchase and sale agreement is used to document the parties' intentions and the terms they have agreed will govern the transaction. You can include specific terms like the product or property, the price of the product or property, conditions for the delivery of the product, and the date of product delivery.

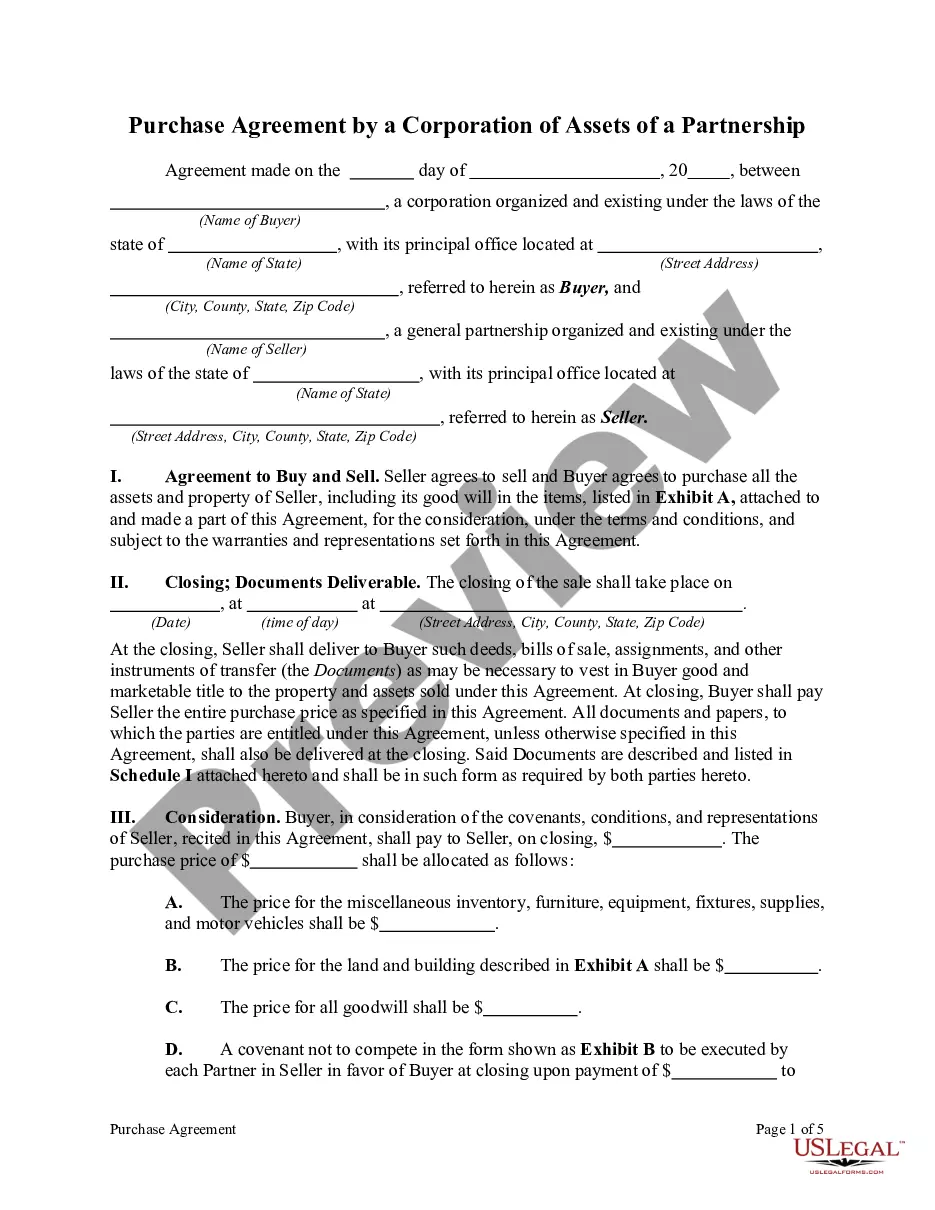

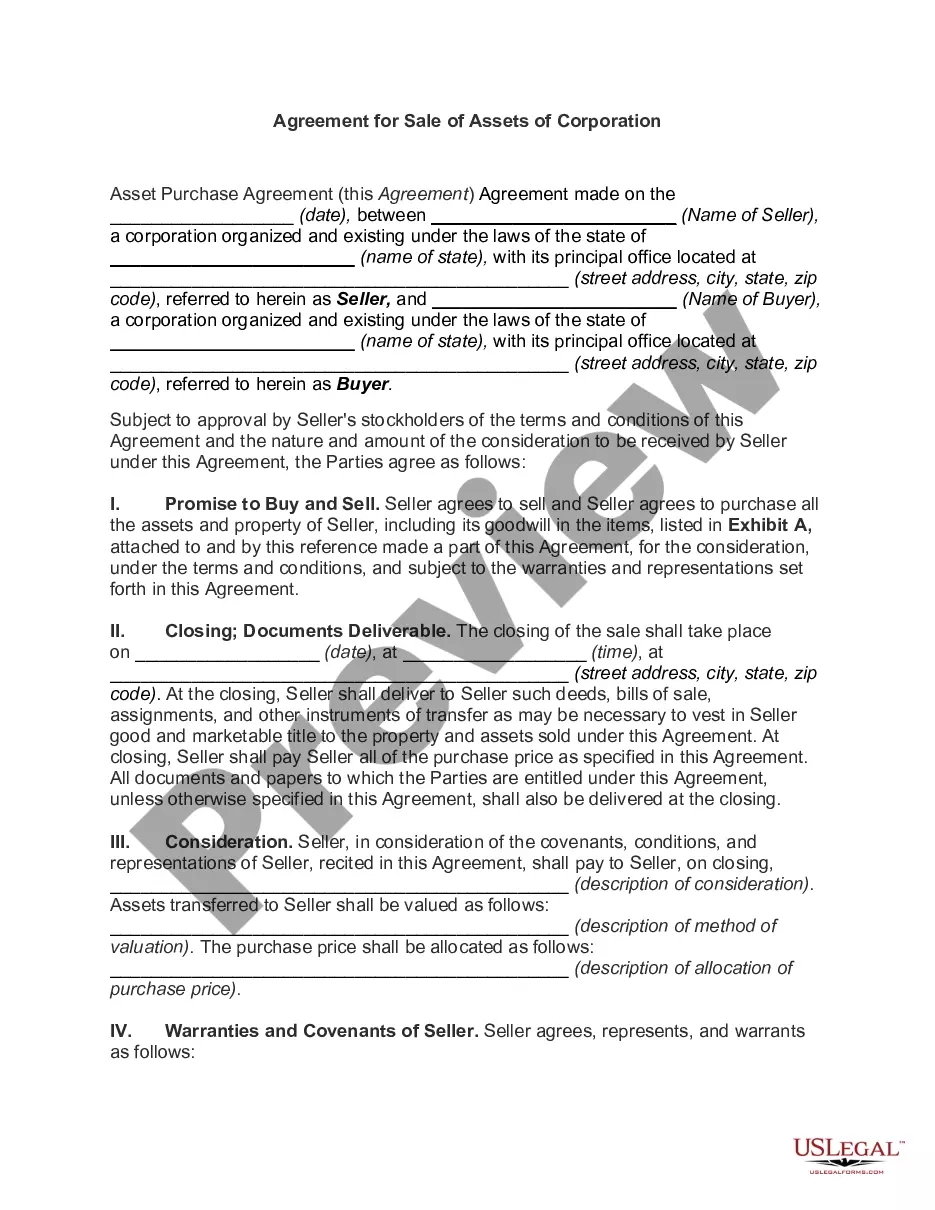

An asset purchase agreement is a legal contract to buy the assets of a business. It can also be used to purchase specific assets from a business, especially if they are significant in value.

After signing a letter of intent and completing due diligence, a business purchase agreement marks the official start to the legally binding transaction of a business. This agreement requires the buyer to purchase the business ing to the terms and price outlined in the agreement.