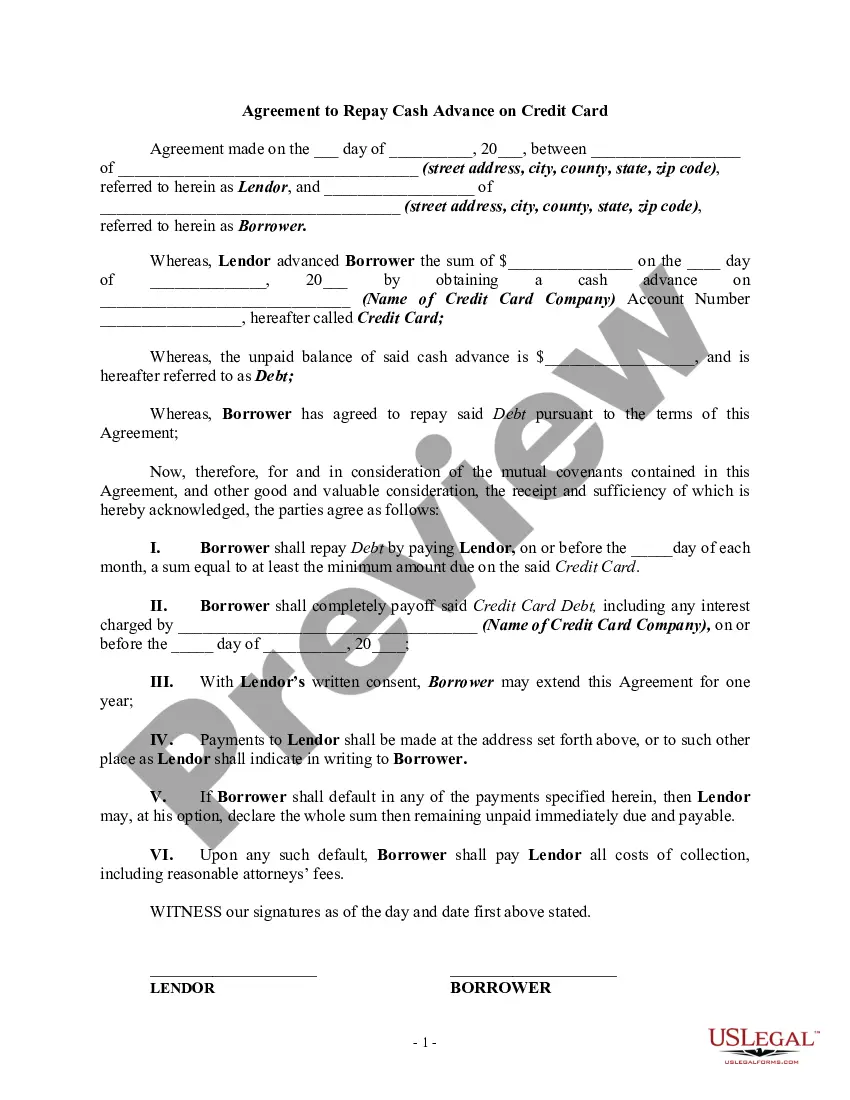

Iowa Agreement to Repay Cash Advance on Credit Card serves as a legally binding document between a borrower and a credit card company when it comes to obtaining a cash advance from a credit card. This agreement outlines the terms and conditions under which the borrower may access and repay the cash advance, including interest rates, fees, and repayment obligations. The Iowa Agreement to Repay Cash Advance on Credit Card aims to protect both parties involved by setting clear guidelines for the transaction. When it comes to different types of Iowa Agreement to Repay Cash Advance on Credit Card, they may vary slightly depending on the credit card company and specific terms offered. However, some common variations include: 1. Fixed Percentage Agreement: This type of agreement stipulates that the borrower can access a cash advance up to a certain percentage of their credit limit. For example, if the credit limit is $10,000 and the fixed percentage is 50%, the borrower can access up to $5,000 as a cash advance. 2. Variable Percentage Agreement: In this scenario, the percentage of the credit limit that can be obtained as a cash advance may fluctuate based on factors such as the borrower's credit score or payment history. The credit card company assesses and adjusts the available cash advance amount accordingly. 3. Introductory Period Agreement: Some credit card companies may offer promotional introductory periods with reduced or waived fees and interest rates for cash advances. This type of agreement usually outlines the specific duration of the promotional period and the terms that apply during this time. Key aspects that should be included in an Iowa Agreement to Repay Cash Advance on Credit Card are: a. Interest Rates: The agreement should clearly state the applicable interest rate for the cash advance, whether it's a fixed rate or variable rate, and any potential changes to the rate over time. b. Fees: This section should outline any associated fees, such as cash advance fees or ATM withdrawal fees, and specify if there are any exceptions or circumstances where these fees may be waived. c. Repayment Terms: The agreement should provide details on the repayment obligations, including the minimum monthly payment required, the due date, and the consequences of late or missed payments. d. Grace Period: If the credit card company offers a grace period before interest is charged on the cash advance, this should be clearly stated, along with the duration of the grace period. e. Credit Limit Adjustments: The agreement may specify if accessing a cash advance can temporarily reduce the available credit limit and how long it takes for the limit to reset after repayment. In summary, an Iowa Agreement to Repay Cash Advance on Credit Card is essential for establishing the terms and conditions when acquiring a cash advance from a credit card. Understanding the different types of agreements and their specific terms can help borrowers make informed decisions and ensure responsible financial management.

Iowa Agreement to Repay Cash Advance on Credit Card

Description

How to fill out Iowa Agreement To Repay Cash Advance On Credit Card?

US Legal Forms - one of the most extensive collections of approved forms in the United States - provides various authorized document templates that you can download or print.

By utilizing the website, you can discover numerous forms for business and personal purposes, organized by categories, states, or keywords. You can quickly access the latest versions of forms like the Iowa Agreement to Repay Cash Advance on Credit Card.

If you hold a membership, Log In and download the Iowa Agreement to Repay Cash Advance on Credit Card from your US Legal Forms library. The Download button will be visible on every form you view. You can access all previously downloaded forms from the My documents section of your account.

Every template you add to your account has no expiration date and belongs to you permanently. Therefore, if you wish to download or print another copy, simply navigate to the My documents section and click on the form you need.

Access the Iowa Agreement to Repay Cash Advance on Credit Card with US Legal Forms, the most comprehensive collection of authorized document templates. Utilize a multitude of professional and state-specific templates that cater to your business or personal requirements and preferences.

- Ensure you have selected the correct form for your city/region. Click the Preview button to examine the content of the form. Review the form description to confirm that you have picked the appropriate form.

- If the form does not meet your needs, use the Search field at the top of the screen to find the one that does.

- If you are satisfied with the form, verify your choice by clicking the Purchase now button. Then, select your preferred payment method and provide your details to create an account.

- Process the transaction. Utilize your credit card or PayPal account to complete the payment.

- Choose the format and download the form to your device.

- Edit. Fill in, modify, print, and sign the downloaded Iowa Agreement to Repay Cash Advance on Credit Card.

Form popularity

FAQ

A cash advance lets you borrow a certain amount of money against your credit card's line of credit. You usually pay a fee for the service.

3 And you will pay interest on your cash advance even if you pay it off in full and had a zero balance for that billing cycle. You also have the option of paying off the cash advance over time, just as you can with a purchase, as long as you make minimum monthly payments.

That means you will be charged interest starting from the date you withdraw a cash advance. That's different from when you make a purchase with you card, and the issuer offers a grace period of at least 21 days where you won't incur interest if your balance is paid in full by the due date.

ATM or bank fee: If you use an ATM or visit a bank, you can expect a fee for taking out a cash advance. No grace period: Cash advances don't benefit from a grace period. That means you will be charged interest starting from the date you withdraw a cash advance.

Pay off your cash advance as fast as you can Since your advance begins accruing interest the same day you get your cash, start repaying the amount you borrow as soon as possible. If you take out a $200 cash advance, aim to pay that amount in fullor as much as possibleon top of your minimum payment.

Unlike a cash withdrawal from a bank account, a cash advance has to be paid back just like anything else you put on your credit card. Think of it as using your credit card to "buy" cash rather than goods or services.

A cardholder agreement is a legal document outlining the terms under which a credit card is offered to a customer. Among other provisions, the cardholder agreement states the annual percentage rate (APR) of the card, as well as how the card's minimum payments are calculated.

Since your advance begins accruing interest the same day you get your cash, start repaying the amount you borrow as soon as possible. If you take out a $200 cash advance, aim to pay that amount in fullor as much as possibleon top of your minimum payment. Make it a goal to repay the amount in days instead of weeks.

Cash advances don't impact your credit score differently than regular credit card purchases. However, the additional fees and interest that cash advances are subject to sometimes catch card holders off-guard and lead to situations of credit card delinquency, which negatively affect credit score.

A cash advance allows you to use your credit card to get a short-term cash loan at a bank or ATM. Unlike a cash withdrawal from a bank account, a cash advance has to be paid back just like anything else you put on your credit card. Think of it as using your credit card to "buy" cash rather than goods or services.