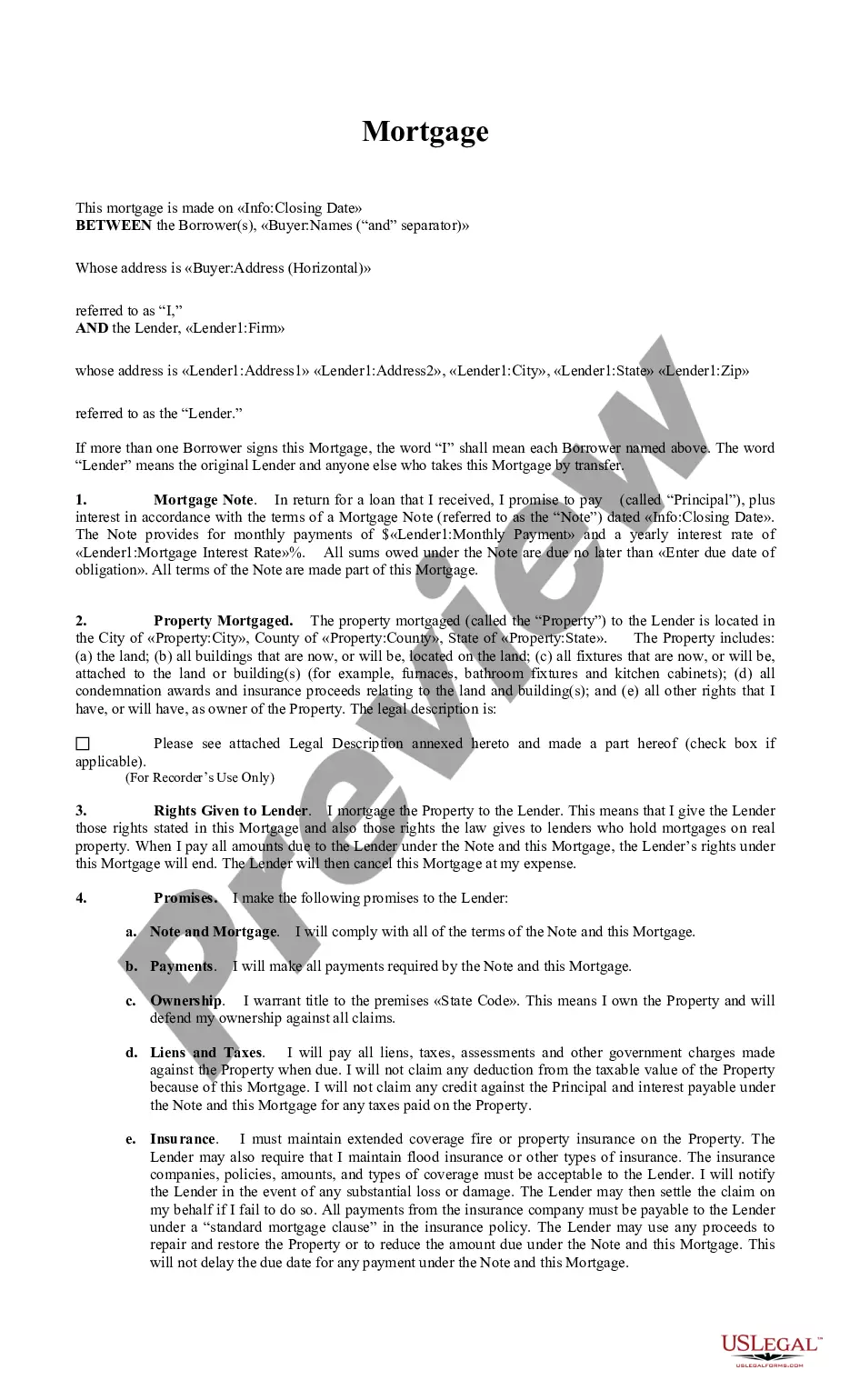

A reverse mortgage is a loan from the U.S. Government for 50% to 75% of the value of a home owned by a homeowner aged 62 and older. Instead of making monthly payments to a lender, as with a regular mortgage, a lender makes payments to the homeowner. The funds from a reverse mortgage are tax-free. The loan doesn't have to be repaid in the homeowner's lifetime, however, when the homeowner dies, the money received plus approximately 4% interest is repaid by their estate. The loan is repaid when the homeowner ceases to occupy the home as a principal residence, due to the homeowner (the last remaining spouse, in cases of couples) passing away, selling the home, or permanently moving out.

Iowa Home Equity Conversion Mortgage - Reverse Mortgage

State:

Multi-State

Control #:

US-01685BG

Format:

Word;

Rich Text

Instant download

Description

Free preview

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Built-in online Word editor

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Export easily

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

E-sign your document

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

Notarize online 24/7

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

Store your document securely

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Home Equity Conversion Mortgage - Reverse Mortgage?

Locating the appropriate authorized document format can be quite a challenge. Naturally, there are numerous online templates available on the web, but how will you acquire the official form you need? Utilize the US Legal Forms website. The service offers thousands of templates, including the Iowa Home Equity Conversion Mortgage - Reverse Mortgage, which can be utilized for business and personal purposes. All the forms are reviewed by experts and fulfill federal and state regulations.

If you are already registered, Log In to your account and then click the Acquire button to locate the Iowa Home Equity Conversion Mortgage - Reverse Mortgage. Use your account to search for the legal documents you have obtained previously. Navigate to the My documents tab of your account and retrieve another copy of the document you need.

If you are a new user of US Legal Forms, here are simple instructions for you to follow: First, ensure you have selected the correct form for your city/county. You can browse the form using the Preview button and review the form details to confirm this is indeed the right one for you. If the form does not meet your needs, utilize the Search field to find the appropriate form. Once you are certain that the form is suitable, click the Buy now button to obtain the form. Choose the payment plan you prefer and enter the required information. Create your account and complete the transaction using your PayPal account or credit card. Select the document format and download the authorized document format to your device. Fill out, modify, print, and sign the acquired Iowa Home Equity Conversion Mortgage - Reverse Mortgage.

Whether for personal or business use, US Legal Forms provides a reliable source for official document templates that meet your legal needs.

- US Legal Forms is the largest collection of legal forms where you can find a variety of document templates.

- Utilize the service to download professionally crafted documents that adhere to state requirements.

- The platform ensures a wide selection of templates to meet diverse legal needs.

- You can conveniently access and manage your forms through your account.

- The process of obtaining legal documents is streamlined for user efficiency.

- Expertly reviewed forms ensure compliance with legal standards.

Form popularity

FAQ

The downside of a reverse mortgage can be that the closing costs can be higher than a traditional loan, the property must be your primary residence, the loan is not assumable, and there may be less equity to leave to your heir as an inheritance. Here's the Truth About Reverse Mortgages (No BS) reverse.mortgage ? truth-about-reverse-mortgages reverse.mortgage ? truth-about-reverse-mortgages

A Home Equity Conversion Mortgage (HECM), the most common type of reverse mortgage, is a special type of home loan only for homeowners who are 62 and older. This information only applies to Home Equity Conversion Mortgages (HECMs), which are the most common type of reverse mortgage loans.

Cons of HECM You have to live in your home: When you get a HECM, your property must be your principal residence for much of the year. You'll have to pay back the HECM if you sell the home or want to move.

A reverse mortgage increases your debt and can use up your equity. While the amount is based on your equity, you're still borrowing the money and paying the lender a fee and interest. Your debt keeps going up (and your equity keeps going down) because interest is added to your balance every month. Reverse Mortgages | Consumer Advice - Federal Trade Commission ftc.gov ? articles ? reverse-mortgages ftc.gov ? articles ? reverse-mortgages

Reverse mortgage cons Reverse mortgages have costs that include lender fees (origination fees are capped at $6,000 and depend on the amount of your loan), FHA insurance charges and closing costs. These costs can be added to the loan balance; however, that means the borrower would have more debt and less equity. Reverse Mortgage Pros And Cons - Bankrate bankrate.com ? mortgages ? reverse-mortga... bankrate.com ? mortgages ? reverse-mortga...

Reverse mortgages represent one way to get the equity out of your home, but they aren't the only way. If you don't qualify for a reverse mortgage but still want to turn your equity to cash, there are options that you can consider.

A traditional private reverse mortgage is not necessarily backed by the federal government, whereas an HECM is not only underwritten by HUD, it is also regulated to consumer safety by the federal government as well. This allows interest rates charged to be far lower.

The benefit is that HECM loans are nonrecourse, which means the homeowner or the estate (if the homeowner dies) won't have to pay more at the end of the loan than what the home is worth ? no matter whether the home value at the time of sale is less than the loan amount. Everything You Need to Know About HECM Loans | Mortgages and Advice usnews.com ? loans ? mortgages ? articles usnews.com ? loans ? mortgages ? articles