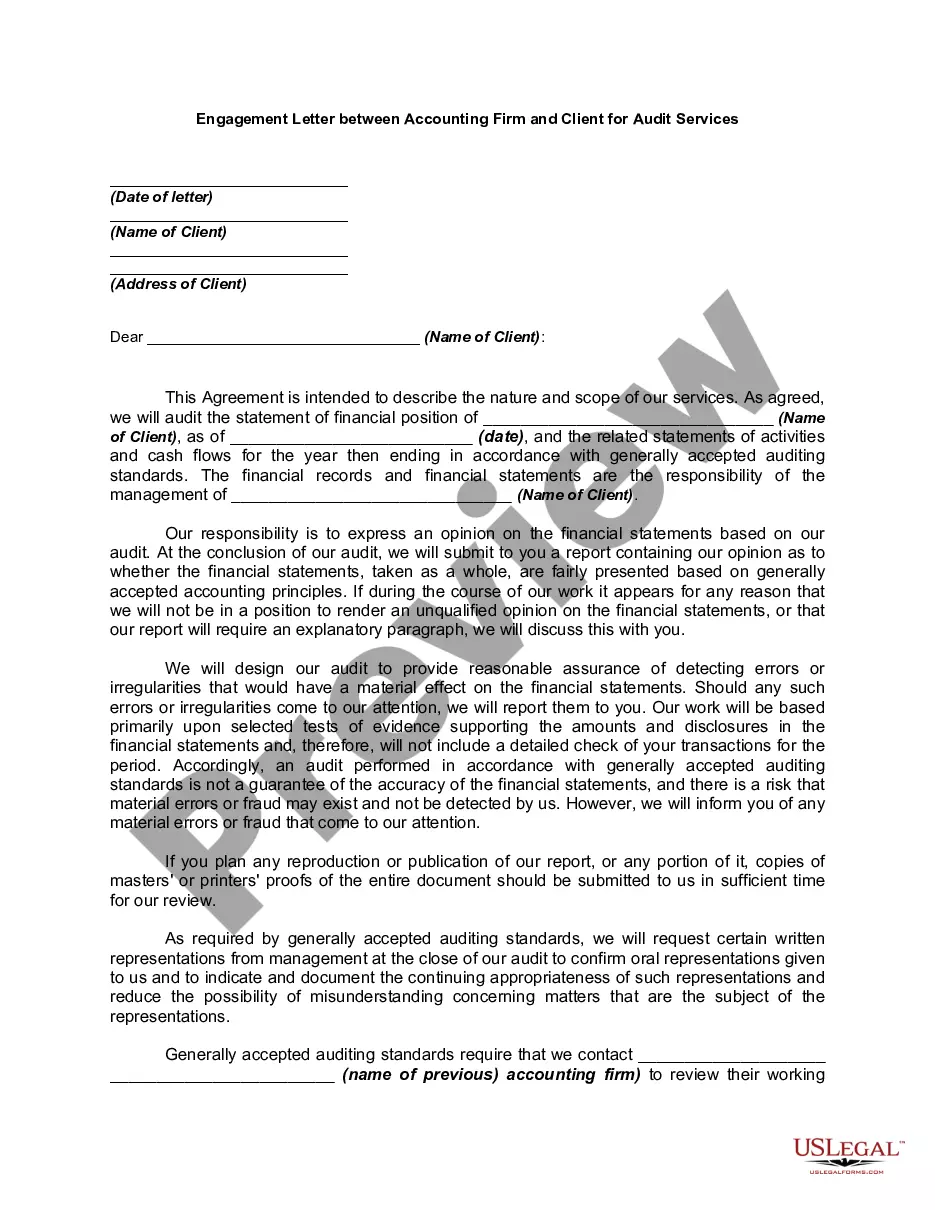

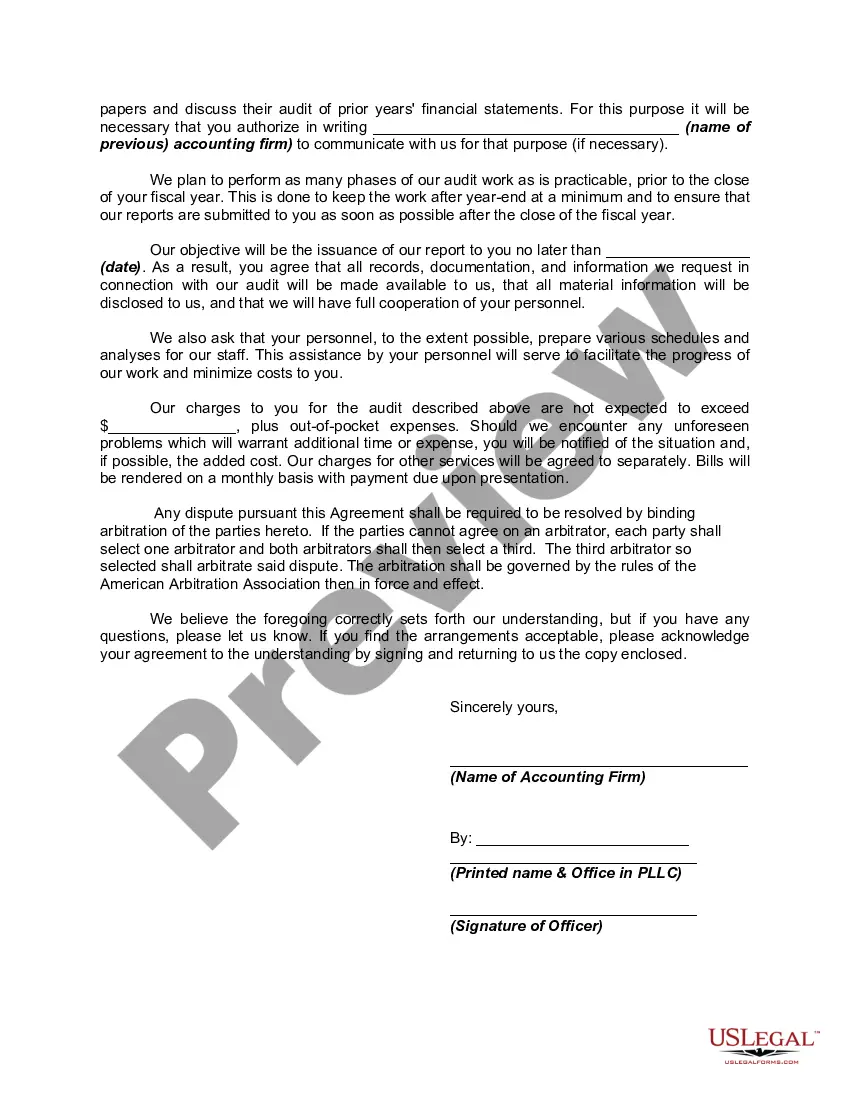

Generally, a contract to employ a certified public accountant need not be in writing. However, such contracts often call for services of a highly complex and technical nature, and hence they should be explicit in their terms, and they should be in writing. In particular, a written employment contract is necessary in order to avoid misunderstanding with the employer regarding the amount of the accountant's fee or compensation and the nature of its computation. As most commonly used in legal settings, an audit is an examination of financial records and documents and other evidence by a trained accountant. Audits are conducted of records of a business or governmental entity, with the aim of ensuring proper accounting practices, recommendations for improvements, and a balancing of the books.

This form is a generic example that may be referred to when preparing such a form for your particular state. It is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a form in a particular jurisdiction.

Iowa Engagement Letter Between Accounting Firm and Client For Audit Services is an important document that serves as a formal agreement between an accounting firm and their client for the provision of audit services. This letter outlines the terms and conditions, responsibilities, and expectations of both parties involved in the engagement. Iowa Engagement Letters for audit services can be further categorized based on the type of client or organization they cater to, such as: 1. Iowa Engagement Letter for Nonprofit Organizations: This type of engagement letter specifically addresses the audit requirements and considerations relevant to nonprofit organizations in Iowa. It includes discussions on compliance with federal and state regulations, specific tax and financial reporting requirements unique to nonprofit entities, and considerations for fund accounting. 2. Iowa Engagement Letter for Governmental Entities: This engagement letter is designed for accounting firms undertaking audit services for governmental entities in Iowa. It covers aspects related to compliance with governmental auditing standards, adherence to legal and regulatory requirements, and the specific financial reporting frameworks applicable to governmental entities. 3. Iowa Engagement Letter for Small Businesses: Tailored for small businesses in Iowa, this engagement letter emphasizes the importance of accurate financial reporting and disclosure requirements. It addresses specific considerations for small businesses such as limited resources, internal control systems, and financial transparency. 4. Iowa Engagement Letter for Publicly-Traded Companies: This engagement letter is specifically developed to address the needs of publicly-traded companies in Iowa. It focuses on compliance with relevant regulations, such as the Sarbanes-Oxley Act, and provides guidance on the audit process, risk assessment, internal controls, and financial statement disclosures. Key elements commonly found in Iowa Engagement Letters for Audit Services include: 1. Scope of the Engagement: Clearly defines the purpose, objectives, and boundaries of the audit engagement, including the timeframe and period under review. 2. Responsibilities of the Accounting Firm: Specifies the responsibilities of the accounting firm, such as conducting the audit in accordance with professional auditing standards, maintaining independence, and rendering an unbiased opinion on the financial statements. 3. Responsibilities of the Client: Outlines the client's obligations, including the preparation and fair presentation of financial statements, provision of necessary documents and information, and cooperation with the audit team. 4. Audit Fee and Payment Terms: States the agreed-upon fee for the audit services and provides details on payment terms, such as the billing frequency and method of payment. 5. Limitations of the Audit: Clearly states that an audit does not guarantee the detection of all errors, fraud, or noncompliance, and specifies that the responsibility for the prevention and detection of such issues rests with the client's management. 6. Confidentiality and Data Protection: Emphasizes the accounting firm's commitment to maintaining the confidentiality of the client's information and data protection practices. Overall, Iowa Engagement Letters for Audit Services play a crucial role in establishing a clear understanding between the accounting firm and the client, ensuring transparency, accountability, and professionalism throughout the audit engagement process.Iowa Engagement Letter Between Accounting Firm and Client For Audit Services is an important document that serves as a formal agreement between an accounting firm and their client for the provision of audit services. This letter outlines the terms and conditions, responsibilities, and expectations of both parties involved in the engagement. Iowa Engagement Letters for audit services can be further categorized based on the type of client or organization they cater to, such as: 1. Iowa Engagement Letter for Nonprofit Organizations: This type of engagement letter specifically addresses the audit requirements and considerations relevant to nonprofit organizations in Iowa. It includes discussions on compliance with federal and state regulations, specific tax and financial reporting requirements unique to nonprofit entities, and considerations for fund accounting. 2. Iowa Engagement Letter for Governmental Entities: This engagement letter is designed for accounting firms undertaking audit services for governmental entities in Iowa. It covers aspects related to compliance with governmental auditing standards, adherence to legal and regulatory requirements, and the specific financial reporting frameworks applicable to governmental entities. 3. Iowa Engagement Letter for Small Businesses: Tailored for small businesses in Iowa, this engagement letter emphasizes the importance of accurate financial reporting and disclosure requirements. It addresses specific considerations for small businesses such as limited resources, internal control systems, and financial transparency. 4. Iowa Engagement Letter for Publicly-Traded Companies: This engagement letter is specifically developed to address the needs of publicly-traded companies in Iowa. It focuses on compliance with relevant regulations, such as the Sarbanes-Oxley Act, and provides guidance on the audit process, risk assessment, internal controls, and financial statement disclosures. Key elements commonly found in Iowa Engagement Letters for Audit Services include: 1. Scope of the Engagement: Clearly defines the purpose, objectives, and boundaries of the audit engagement, including the timeframe and period under review. 2. Responsibilities of the Accounting Firm: Specifies the responsibilities of the accounting firm, such as conducting the audit in accordance with professional auditing standards, maintaining independence, and rendering an unbiased opinion on the financial statements. 3. Responsibilities of the Client: Outlines the client's obligations, including the preparation and fair presentation of financial statements, provision of necessary documents and information, and cooperation with the audit team. 4. Audit Fee and Payment Terms: States the agreed-upon fee for the audit services and provides details on payment terms, such as the billing frequency and method of payment. 5. Limitations of the Audit: Clearly states that an audit does not guarantee the detection of all errors, fraud, or noncompliance, and specifies that the responsibility for the prevention and detection of such issues rests with the client's management. 6. Confidentiality and Data Protection: Emphasizes the accounting firm's commitment to maintaining the confidentiality of the client's information and data protection practices. Overall, Iowa Engagement Letters for Audit Services play a crucial role in establishing a clear understanding between the accounting firm and the client, ensuring transparency, accountability, and professionalism throughout the audit engagement process.