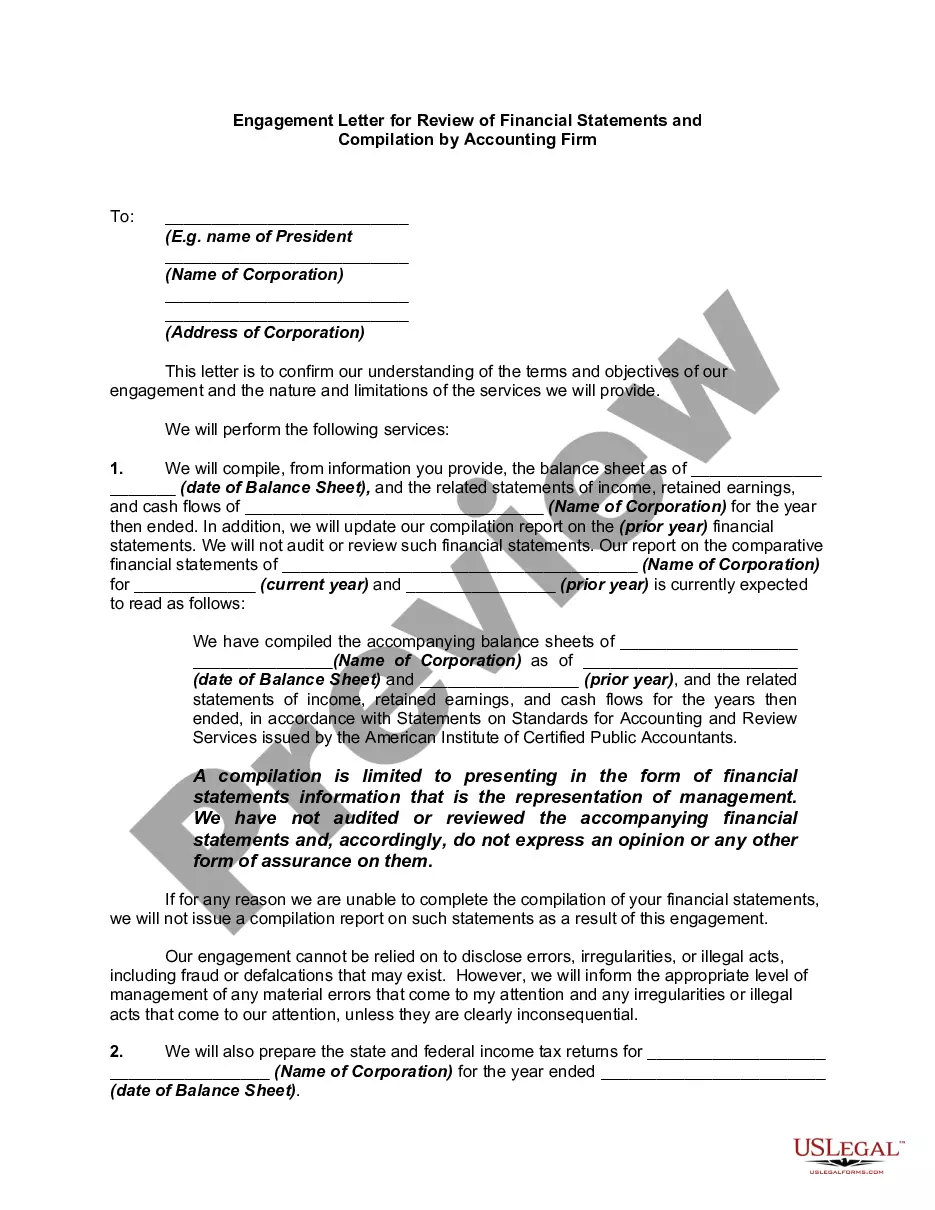

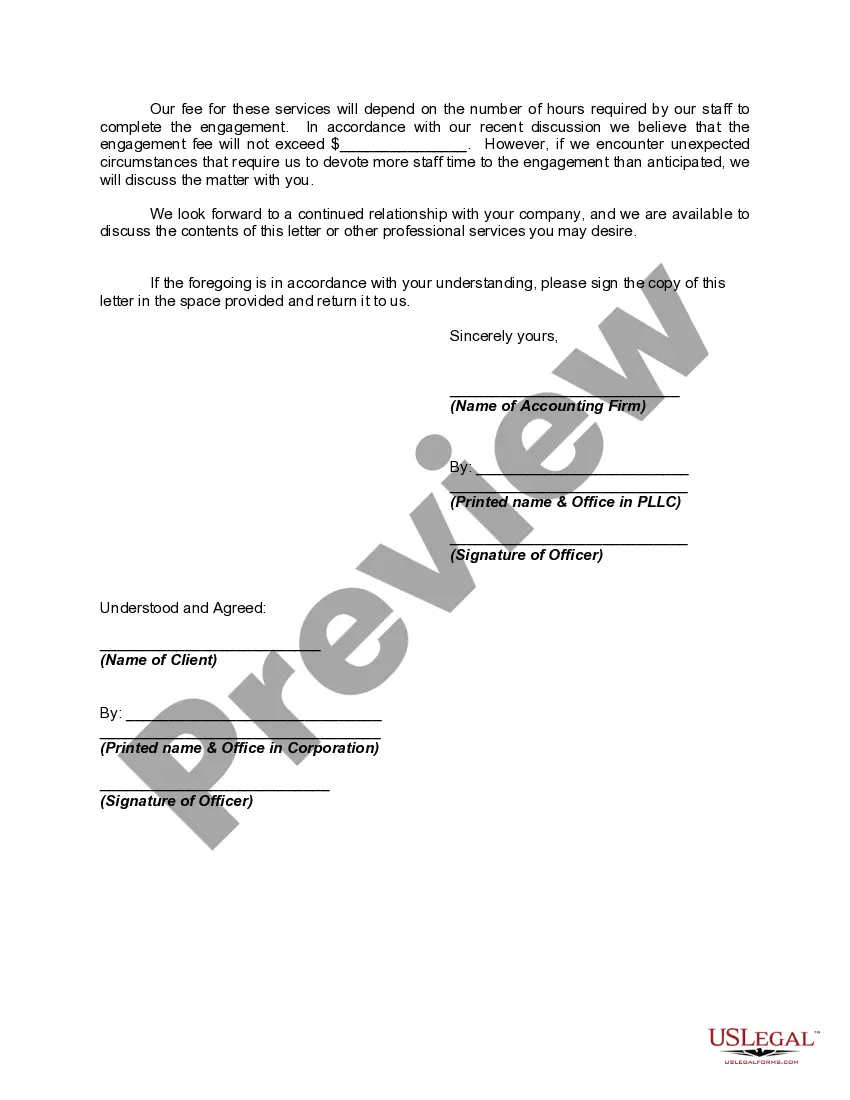

Compiled financial statements represent the most basic level of service that certified public accountants provide with respect to financial statements. In a compilation, the CPA must comply with certain basic requirements of professional standards, such as having a knowledge of the client's industry and applicable accounting principles, having a clear understanding with the client as to the services to be provided, and reading the financial statements to determine whether there are any obvious departures from generally accepted accounting principles (or, in some cases, another comprehensive basis of accounting used by the entity). It may be necessary for the CPA to perform "other accounting services" (such as creating a general ledger for the client, or assisting the client with adjusting entries for the books of the client (before the financial statements can be prepared). Upon completion, a report on the financial statements is issued that states a compilation was performed in accordance with AICPA professional standards, but no assurance is expressed that the statements are in conformity with generally accepted accounting principles. This is known as the expression of "no assurance." Compiled financial statements are often prepared for privately-held entities that do not need a higher level of assurance expressed by the CPA.

Iowa Engagement Letter for Review of Financial Statements and Compilation by Accounting Firm An Iowa Engagement Letter for Review of Financial Statements and Compilation by an Accounting Firm is a formal agreement between an accounting firm and its client in the state of Iowa, outlining the terms of engagement for the services of reviewing financial statements and compiling them. This letter serves as a contractual agreement that defines the scope, responsibilities, and expectations of both parties involved in the financial statement review and compilation process in accordance with the Iowa State Laws and regulations. The engagement letter ensures transparency and clear communication between the accounting firm and the client in regard to the specific financial services being provided. It establishes a professional relationship and outlines the obligations and liabilities of each party, protecting both the accounting firm and the client. The key elements typically included in an Iowa Engagement Letter for Review of Financial Statements and Compilation by an Accounting Firm are: 1. Client Information: This section will include the client's details, such as their legal name, address, contact information, and any relevant identification numbers. 2. Scope of Engagement: Here, the engagement letter will outline the specific services to be provided, such as the review of financial statements, compilation of financial statements, and any other related services agreed upon. 3. Objective: The objective section will define the purpose of the engagement, whether it is to provide limited assurance through a review or to compile financial statements without any assurance. 4. Responsibilities: This section will outline the responsibilities of both the accounting firm and the client throughout the engagement. It may include the provision of accurate and complete financial information by the client, access to necessary documents and records, and adherence to Iowa State Laws and regulations. 5. Reporting: The reporting section will detail the format of the final financial statements, any disclosures required, and the estimated timeline for completion. 6. Fee Structure: This part will define the financial terms of the engagement, including the agreed-upon fees, payment terms, and any additional expenses or disbursements. 7. Termination: Contingencies or circumstances under which either party can terminate the engagement will be defined in this section, along with any associated penalties or obligations. Different types of Iowa Engagement Letters for Review of Financial Statements and Compilation by Accounting Firm may include variations in scope, objectives, or specific service requirements depending on the needs and preferences of the client. However, the key elements mentioned above are typically present in all engagement letters to ensure a comprehensive and professional agreement. In conclusion, an Iowa Engagement Letter for Review of Financial Statements and Compilation by an Accounting Firm is a crucial document that outlines the terms and conditions of the engagement between a client and an accounting firm in Iowa. It provides a clear description of the agreed-upon services, responsibilities, objectives, and fee structure, ensuring a transparent and mutually beneficial arrangement for both parties.