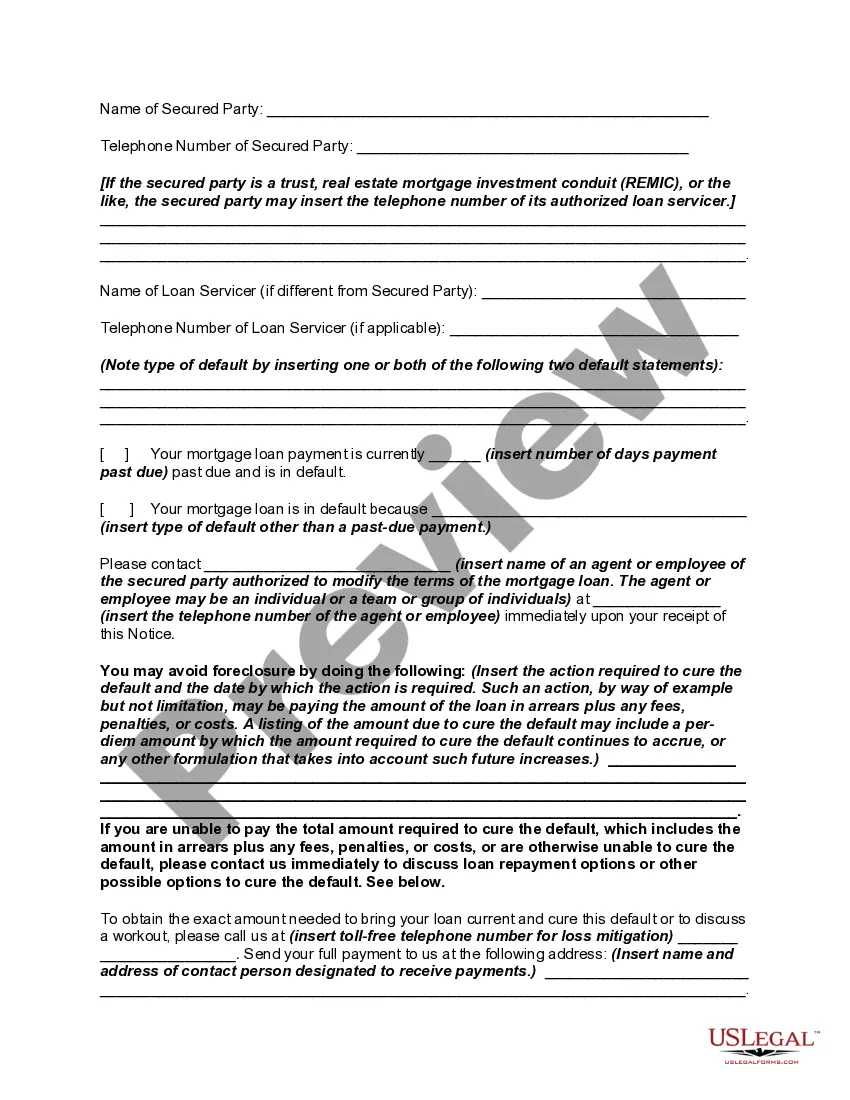

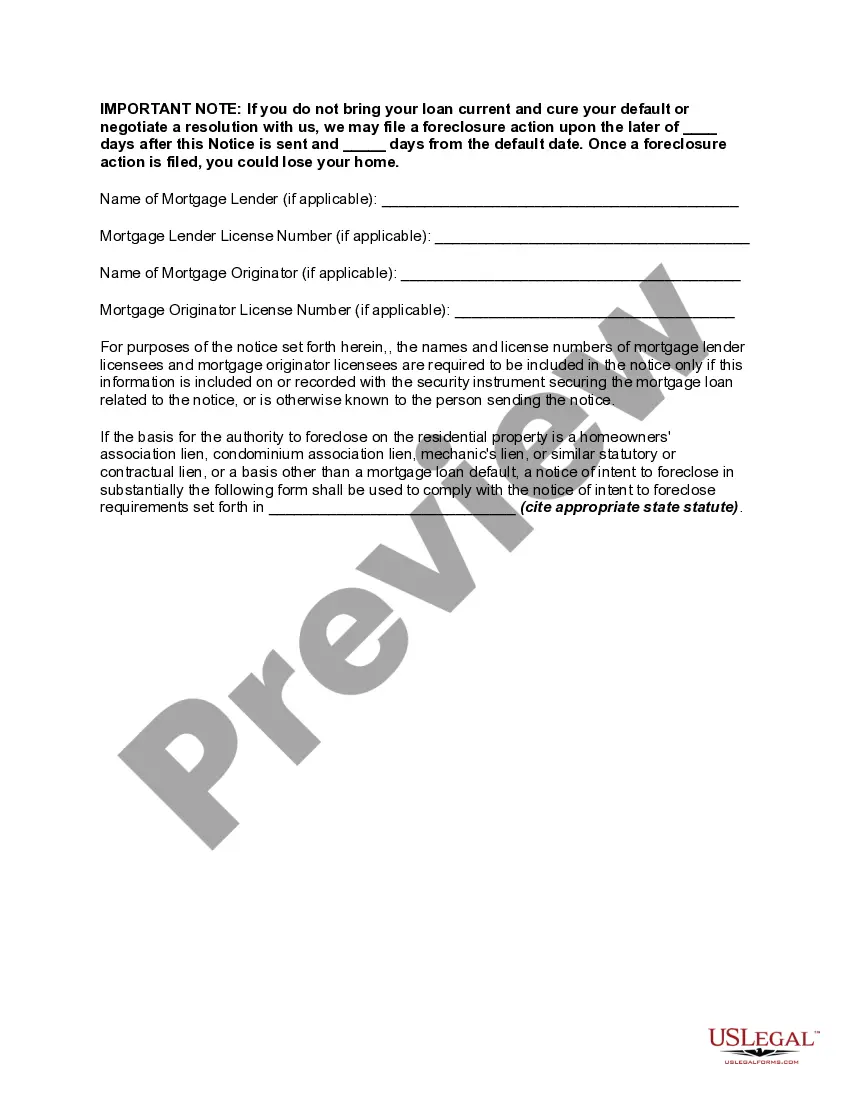

A number of states have enacted measures to facilitate greater communication between borrowers and lenders by requiring mortgage servicers to provide certain notices to defaulted borrowers prior to commencing a foreclosure action. The measures serve a dual purpose, providing more meaningful notice to borrowers of the status of their loans and slowing down the rate of foreclosures within these states. For instance, one state now requires a mortgagee to mail a homeowner a notice of intent to foreclose at least 45 days before initiating a foreclosure action on a loan. The notice must be in writing, and must detail all amounts that are past due and any itemized charges that must be paid to bring the loan current, inform the homeowner that he or she may have options as an alternative to foreclosure, and provide contact information of the servicer, HUD-approved foreclosure counseling agencies, and the state Office of Commissioner of Banks.

Title: Understanding the Iowa Notice of Intent to Foreclose — Mortgage Loan Default Keywords: Iowa, Notice of Intent to Foreclose, Mortgage Loan Default, foreclosure process, delinquency, mortgage lender, loan modification, foreclosure alternatives Introduction: The Iowa Notice of Intent to Foreclose — Mortgage Loan Default is a legal document that mortgage lenders in Iowa send to borrowers who have fallen into default on their mortgage loans. This notice serves as an official communication, informing the borrower about the lender's intention to proceed with foreclosure if the delinquency remains unresolved. Iowa's law requires lenders to follow specific procedures and timelines when initiating foreclosure, ensuring that borrowers have certain rights and opportunities to address the default before foreclosure takes place. Types of Iowa Notice of Intent to Foreclose — Mortgage Loan Default: 1. Initial Notice of Intent: This standard notice is typically the first communication sent by a mortgage lender to a borrower who has fallen behind on their mortgage payments. It outlines the lender's intention to proceed with foreclosure unless the default is rectified within a specified timeframe. 2. Notice of Intent with Loan Modification Options: In some cases, the lender may provide alternatives to foreclosure in the form of loan modification options. This notice informs the borrower about the possibility of modifying their existing mortgage terms to make their payments more manageable and avoid foreclosure. 3. Notice of Intent to Foreclose after Failed Loan Modification: If a borrower has previously attempted a loan modification but defaulted on the revised terms, the lender may issue a subsequent notice of intent to foreclose. This notice emphasizes that the prior modification attempt was unsuccessful, and foreclosure proceedings may commence. 4. Final Notice of Intent: If a borrower has not successfully resolved the delinquency or arranged an agreement with the lender after receiving prior notices, the final notice of intent is sent. This notice indicates the imminent initiation of foreclosure proceedings and the borrower's final opportunity to remedy the default before legal action is taken. Important Considerations: 1. Seek Legal Advice: When receiving an Iowa Notice of Intent to Foreclose — Mortgage Loan Default, it is crucial for borrowers to seek advice from a qualified attorney experienced in foreclosure law. An attorney can provide guidance on available options, negotiate with the lender, and protect the borrower's interests throughout the process. 2. Exploring Alternatives: Borrowers should explore foreclosure alternatives such as loan modifications, repayment plans, refinancing, or short sales. These options may help resolve the default and avoid foreclosure. 3. Timely Communication: Open and timely communication with the mortgage lender is essential. By promptly responding to the notice and engaging in discussions with the lender, borrowers can negotiate potential solutions and potentially halt foreclosure proceedings. 4. Consider Housing Counseling Services: Housing counseling agencies approved by the U.S. Department of Housing and Urban Development (HUD) may provide valuable guidance to borrowers facing foreclosure, assisting them in understanding their rights, exploring options, and establishing realistic plans to prevent foreclosure. Conclusion: The Iowa Notice of Intent to Foreclose — Mortgage Loan Default is a pivotal document in the foreclosure process that notifies borrowers of their default status and the lender's intention to initiate foreclosure if the default remains unresolved. It is crucial for borrowers to understand their rights, explore alternatives, seek legal advice, and communicate effectively with their mortgage lender to potentially avoid the devastating consequences of foreclosure.