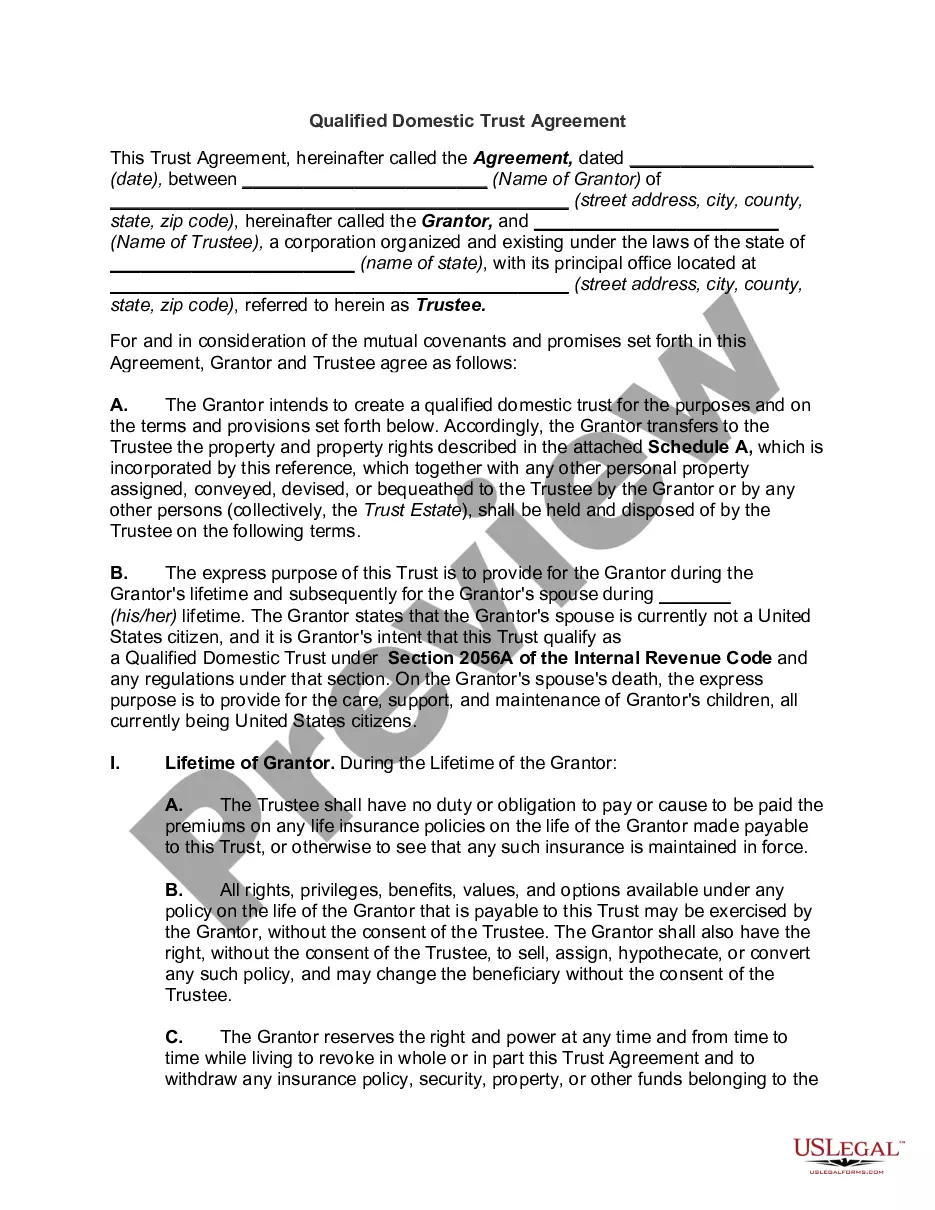

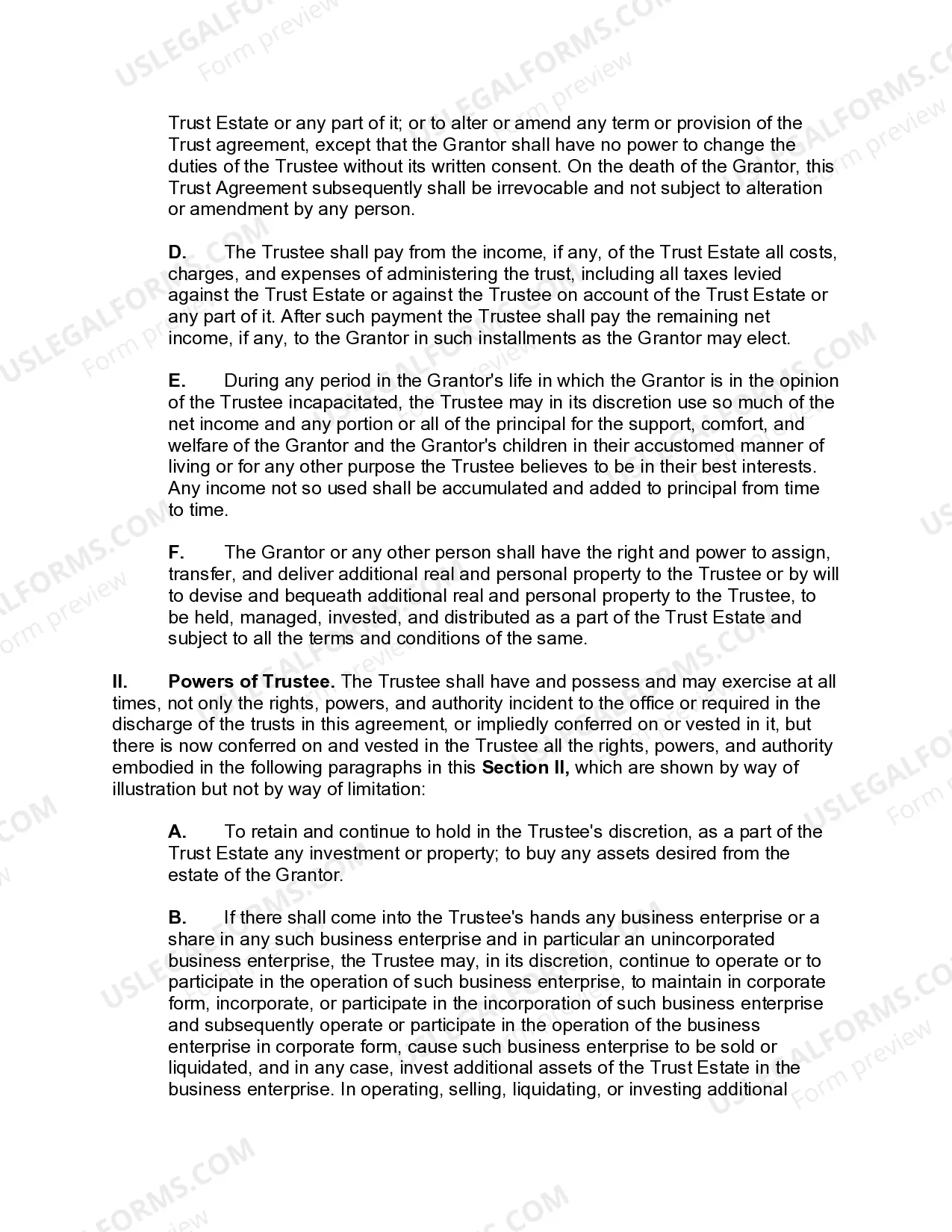

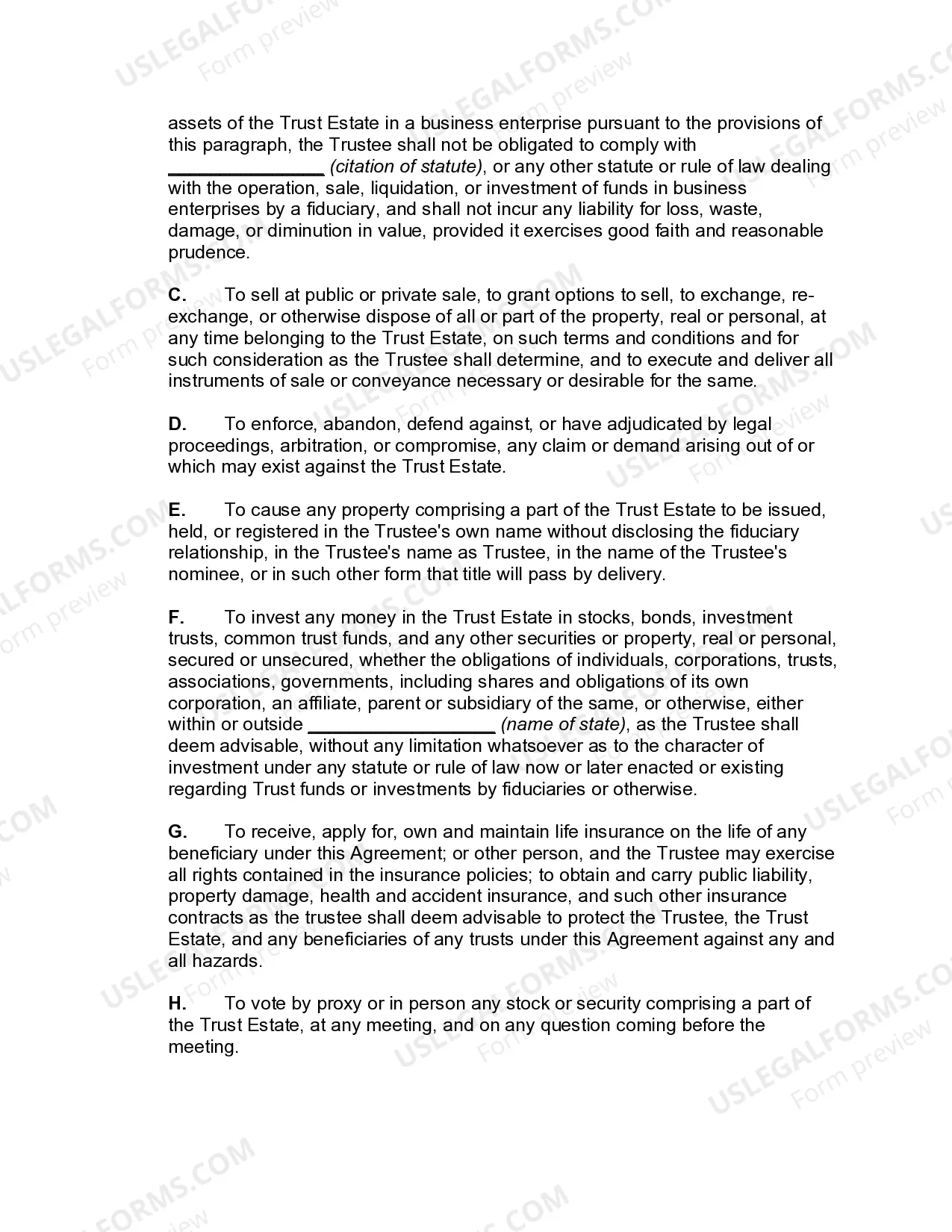

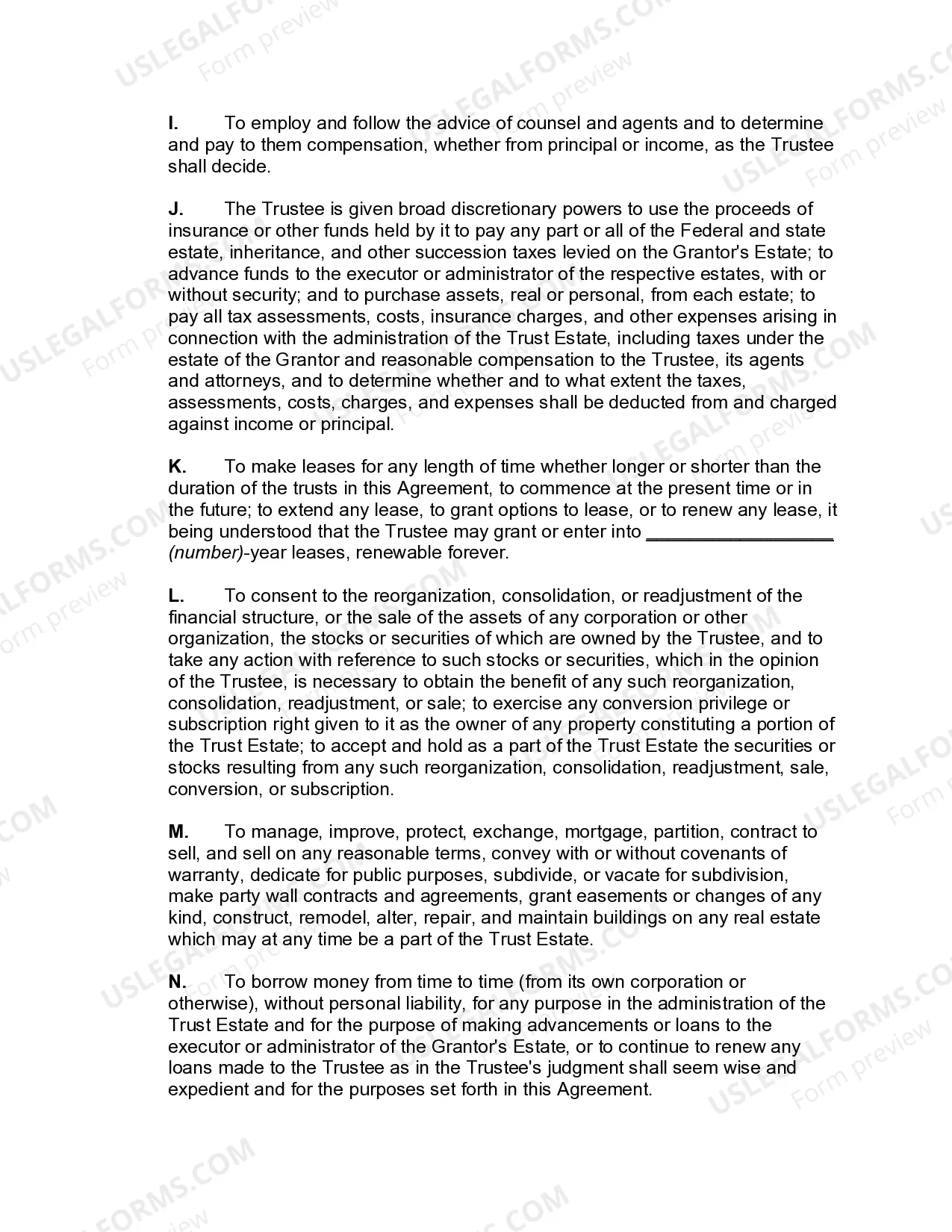

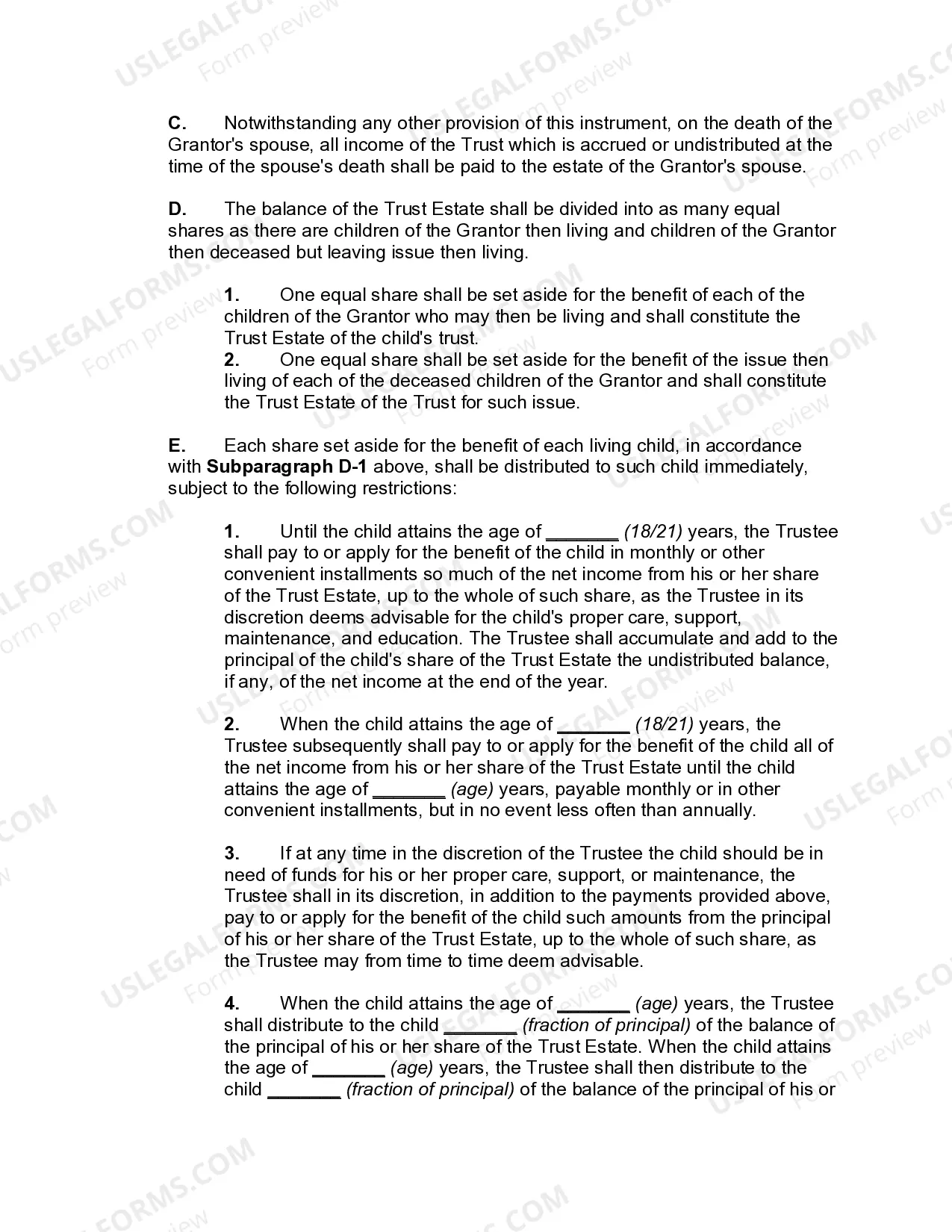

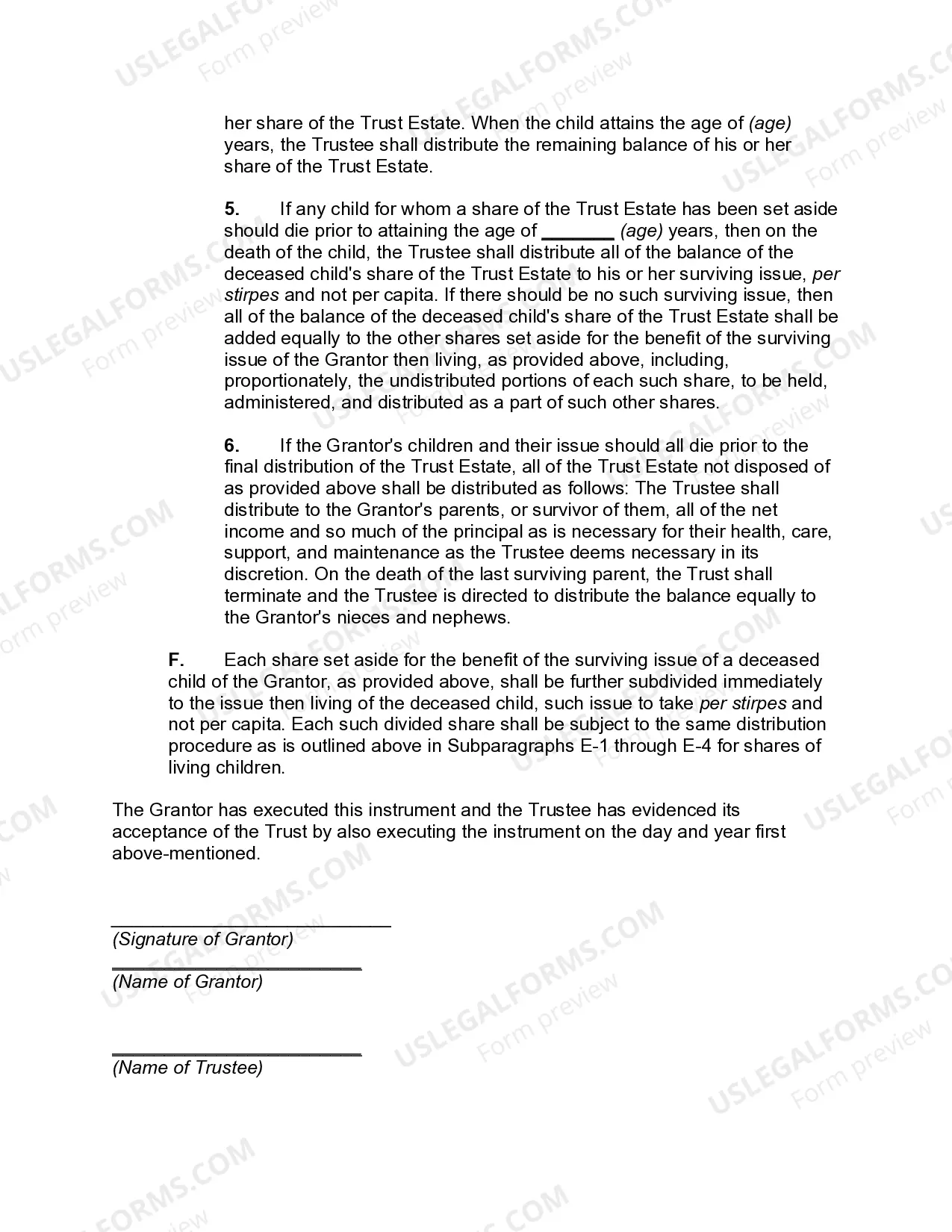

A Qualified Domestic Trust (DOT) Agreement in Iowa is a legal arrangement established for married couples in which one spouse is not a U.S. citizen and the other spouse is a U.S. citizen or resident. The purpose of a DOT Agreement is to allow the non-U.S. citizen spouse to receive certain assets from the U.S. citizen or resident spouse's estate without triggering hefty federal estate taxes. Under Iowa law, DOT Agreements are governed by the Internal Revenue Code (IRC) Section 2056A and the corresponding regulations. These agreements provide an opportunity for non-U.S. citizen spouses to benefit from their U.S. citizen or resident spouse's assets after their passing while deferring the payment of estate taxes until the non-U.S. citizen spouse receives distributions from the trust. The key feature of an Iowa DOT Agreement is that it must meet specific requirements set forth by the IRC. Some critical qualifications include: 1. U.S. Trustee Requirement: A DOT Agreement must appoint a U.S. citizen or U.S. bank as a trustee, ensuring compliance with federal tax reporting and withholding requirements. 2. Estate Tax Deferral: By creating a DOT Agreement, the federal estate taxes that would otherwise be imposed on the marital deduction portion of the estate can be postponed until distributions are made to the non-U.S. citizen spouse or the trust terminates. 3. Minimum Annual Distribution: The trust must provide for the distribution of income at least annually to the non-U.S. citizen spouse. Additionally, the agreement must limit distributions of principal without imposing federal estate taxes on those distributions. Iowa does not differentiate between different types of DOT Agreements, as the requirements and benefits are consistent across the state. However, it's essential to consult with an experienced estate planning attorney who can tailor the DOT Agreement to the specific needs and circumstances of the couple. In summary, an Iowa Qualified Domestic Trust Agreement is a legal tool that enables non-U.S. citizen spouses to receive assets from their U.S. citizen or resident spouse's estate without incurring immediate federal estate taxes. By meeting specific requirements outlined in the Internal Revenue Code, a DOT Agreement provides a tax-efficient solution to preserve and transfer wealth between spouses, ensuring the financial well-being of the non-U.S. citizen spouse even after the passing of the U.S. citizen or resident spouse.

Iowa Qualified Domestic Trust Agreement

Description

How to fill out Iowa Qualified Domestic Trust Agreement?

US Legal Forms - one of several largest libraries of lawful varieties in the States - provides a wide array of lawful document layouts it is possible to down load or produce. While using internet site, you will get 1000s of varieties for business and personal functions, sorted by classes, suggests, or key phrases.You can find the most recent types of varieties much like the Iowa Qualified Domestic Trust Agreement in seconds.

If you already possess a membership, log in and down load Iowa Qualified Domestic Trust Agreement from your US Legal Forms local library. The Obtain button will appear on each and every develop you view. You gain access to all previously downloaded varieties inside the My Forms tab of your own profile.

In order to use US Legal Forms the very first time, allow me to share easy instructions to help you get started:

- Be sure you have picked out the best develop for your city/state. Click on the Review button to review the form`s content. Browse the develop information to actually have selected the correct develop.

- If the develop doesn`t suit your specifications, utilize the Research area at the top of the screen to find the one which does.

- When you are happy with the form, confirm your choice by simply clicking the Get now button. Then, select the pricing plan you favor and give your accreditations to register on an profile.

- Process the purchase. Utilize your bank card or PayPal profile to perform the purchase.

- Choose the formatting and down load the form on your own product.

- Make adjustments. Fill out, revise and produce and signal the downloaded Iowa Qualified Domestic Trust Agreement.

Each web template you put into your bank account does not have an expiry particular date and is your own permanently. So, if you wish to down load or produce one more duplicate, just go to the My Forms portion and click in the develop you will need.

Obtain access to the Iowa Qualified Domestic Trust Agreement with US Legal Forms, one of the most extensive local library of lawful document layouts. Use 1000s of professional and condition-distinct layouts that satisfy your small business or personal requires and specifications.

Form popularity

FAQ

Purpose of Form Under certain circumstances, the trustee/designated filer uses Form 706-QDT to notify the IRS that the trust is exempt from future filing because the surviving spouse has become a U.S. citizen and meets the requirements listed under Part IIElections by the Trustee/Designated Filer, Line 4.

A qualified domestic trust (QDOT) allows a non-citizen surviving spouse of a deceased taxpayer to take advantage of the marital deduction on estate tax for any assets that are placed into the trust before the death of the decedent.

The QDOT should be taxed as a simple trust for income tax purposes. The assets transferred into the QDOT are eligible for the unlimited marital deduction. Each distribution from the QDOT triggers the federal estate tax.

The executor of a decedent's estate uses Form 706 to figure the estate tax imposed by Chapter 11 of the Internal Revenue Code. Form 706 is also used to compute the generation-skipping transfer (GST) tax imposed by Chapter 13 on direct skips.

To make a living trust in Iowa, you:Choose whether to make an individual or shared trust.Decide what property to include in the trust.Choose a successor trustee.Decide who will be the trust's beneficiariesthat is, who will get the trust property.Create the trust document.More items...

A domestic trust is any trust in which the following conditions are met: (1) A court within the U.S. must be able to exercise primary supervision over the administration of the trust. (2) One or more U.S. persons have the authority to control all substantial decisions of the trust.

The QDOT should be taxed as a simple trust for income tax purposes. The assets transferred into the QDOT are eligible for the unlimited marital deduction. Each distribution from the QDOT triggers the federal estate tax.

A QDOT (Qualified Domestic Trust) is a trust for the benefit of a surviving non-citizen spouse that defers the federal estate tax following the death of the first spouse. A Qualified Domestic Trust defers the federal estate tax because it qualifies for the unlimited marital deduction.

Can a QDOT Be Established after Death? Qualified Domestic Trusts don't need to be created as inter-vivos (or, still-living) trusts, but once a spouse passes away, the options become more limited. Post-mortem QDOTs can be created by your non-citizen spouse, but there are time constraints that you must be mindful of.

For estates that are less than those amounts, no QDOT is needed since no federal estate tax would be due. However, for estates greater than those amounts, no marital deduction will be allowed if the surviving spouse is not a U.S. citizen and does not become a citizen by the time that the estate tax return is filed.