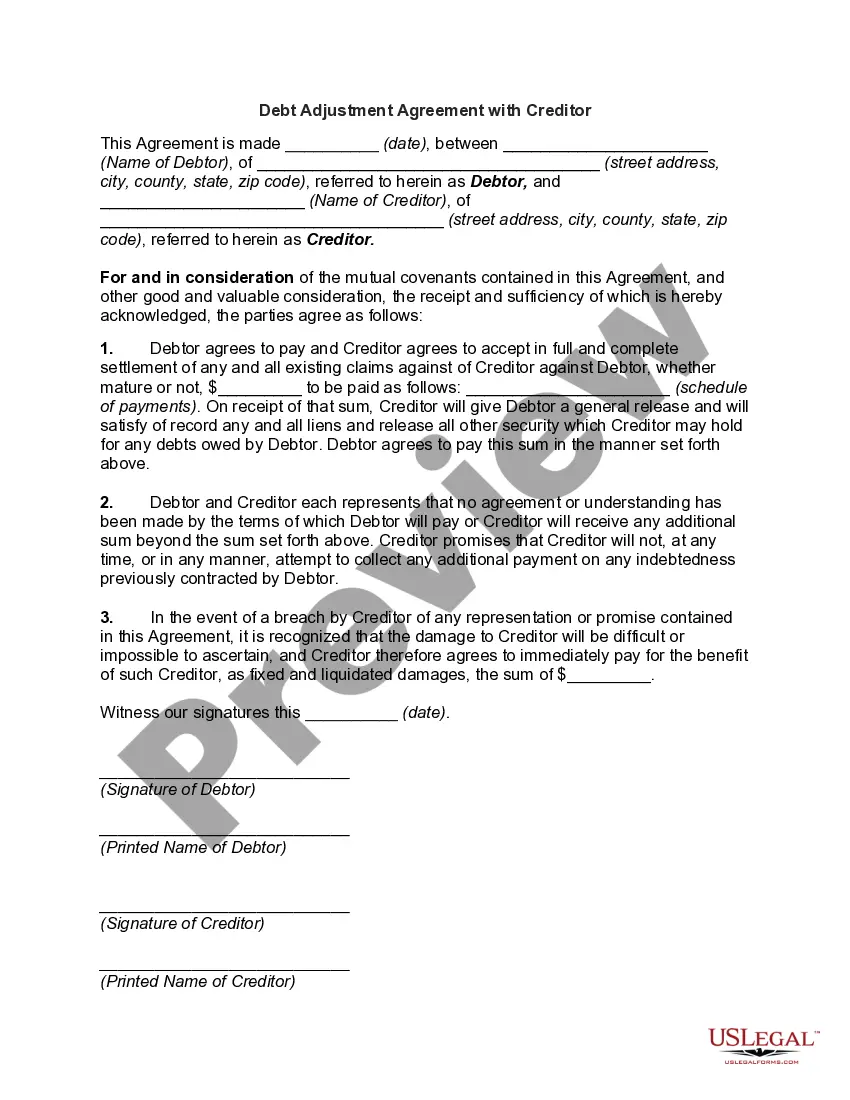

The Iowa Debt Adjustment Agreement with Creditor is a legal contract that outlines the terms and conditions for the repayment of debt between a debtor and a creditor in the state of Iowa. This agreement is designed to provide a structured and manageable repayment plan for individuals or businesses who are struggling to meet their financial obligations. The primary purpose of this agreement is to help debtors regain control of their finances by establishing a realistic and affordable repayment plan. It aims to prevent the debtor from falling into further financial distress and to assist them in avoiding bankruptcy. By entering into this agreement, debtors can negotiate with their creditors to reduce interest rates, waive penalties, or extend the repayment period to make the debt more manageable. There are several types of Iowa Debt Adjustment Agreements with Creditors available, depending on the individual circumstances and the type of debt being addressed. These may include: 1. Consumer Debt Adjustment Agreement: This type of agreement is tailored for individuals who have accumulated significant consumer debt, such as credit card bills, personal loans, or medical expenses. It allows debtors to restructure their payment schedule and reduce the financial burden. 2. Business Debt Adjustment Agreement: Designed specifically for businesses facing financial difficulties, this agreement helps restructure their outstanding debts and establish a new payment plan. It allows businesses to continue operations while managing their financial obligations. 3. Mortgage Debt Adjustment Agreement: This type of agreement focuses on renegotiating the terms of a mortgage loan. It often involves lowering the interest rate, extending the repayment period, or modifying other loan terms to make the mortgage more affordable for the debtor. 4. Student Loan Debt Adjustment Agreement: Student loan debt is a common financial burden for many individuals. This agreement helps debtors negotiate new repayment terms with their student loan lenders, such as lower monthly payments or an extended repayment period. In order to initiate an Iowa Debt Adjustment Agreement with a Creditor, the debtor typically seeks the assistance of a reputable debt adjustment agency or a bankruptcy attorney. These professionals help negotiate with creditors on behalf of the debtor and assist with drafting the agreement to ensure it complies with Iowa state laws. Overall, the Iowa Debt Adjustment Agreement with Creditor provides a legal framework for debtors to work towards resolving their financial difficulties in a structured and manageable manner. It aims to alleviate the stress associated with overwhelming debt and helps debtors regain control of their financial future.

Iowa Debt Adjustment Agreement with Creditor

Description

How to fill out Iowa Debt Adjustment Agreement With Creditor?

Are you presently in a place where you need paperwork for both organization or person uses virtually every day time? There are plenty of lawful document web templates available on the net, but finding kinds you can depend on is not simple. US Legal Forms offers a large number of form web templates, just like the Iowa Debt Adjustment Agreement with Creditor, which can be written to meet state and federal needs.

If you are presently informed about US Legal Forms web site and have a merchant account, simply log in. After that, you are able to acquire the Iowa Debt Adjustment Agreement with Creditor template.

Unless you offer an bank account and want to begin using US Legal Forms, adopt these measures:

- Get the form you require and make sure it is to the right town/state.

- Take advantage of the Preview option to examine the form.

- Look at the information to ensure that you have selected the appropriate form.

- In case the form is not what you`re searching for, take advantage of the Lookup field to discover the form that suits you and needs.

- When you obtain the right form, simply click Acquire now.

- Pick the costs program you want, fill out the required information and facts to generate your account, and pay for the transaction making use of your PayPal or Visa or Mastercard.

- Pick a handy file file format and acquire your copy.

Locate every one of the document web templates you possess purchased in the My Forms menus. You can get a extra copy of Iowa Debt Adjustment Agreement with Creditor at any time, if possible. Just click the needed form to acquire or printing the document template.

Use US Legal Forms, one of the most extensive assortment of lawful kinds, to conserve time and stay away from errors. The support offers expertly produced lawful document web templates which you can use for an array of uses. Make a merchant account on US Legal Forms and commence producing your lifestyle easier.

Form popularity

FAQ

Creditors are not obliged to accept a debt solution but they could accept a Debt Management Plan if they feel this is the best way for them to recover the money owed to them. You will have to put forward a firm and fair offer of payment to your creditors and outline how much you can afford to pay back each month.

Can creditors refuse your DMP? Yes. Creditors are not obliged to accept a debt solution but they could accept a Debt Management Plan if they feel this is the best way for them to recover the money owed to them.

Offer a specific dollar amount that is roughly 30% of your outstanding account balance. The lender will probably counter with a higher percentage or dollar amount. If anything above 50% is suggested, consider trying to settle with a different creditor or simply put the money in savings to help pay future monthly bills.

Typically, a creditor will agree to accept 40% to 50% of the debt you owe, although it could be as much as 80%, depending on whether you're dealing with a debt collector or the original creditor. In either case, your first lump-sum offer should be well below the 40% to 50% range to provide some room for negotiation.

Your creditors do not have to accept your offer of payment or freeze interest. If they continue to refuse what you are asking for, carry on making the payments you have offered anyway. Keep trying to persuade your creditors by writing to them again.

Typical debt settlement offers range from 10% to 50% of what you owe. The longer you allow debt to go unpaid, the greater your risk of being sued. Creditors are under no obligation to reduce your debt, even if you are working with a reputable debt settlement company.

Your creditors are not obligated to accept your offer at any point. They can keep on refusing your payment offers as well as your requests to freeze interest.

When you're negotiating with a creditor, try to settle your debt for 50% or less, which is a realistic goal based on creditors' history with debt settlement. If you owe $3,000, shoot for a settlement of up to $1,500.

When you work with a credit counseling agency, you'll meet with a counselor who will review your financial situation and help you understand your options. If a DMP is a good fit, the counselor can negotiate with your creditors on your behalf to create new payment plans.

10 Tips for Negotiating with CreditorsIs Negotiation the Right Move For You? It's important to think carefully about negotiation.Know Your Terms.Keep Your Story Straight.Ask Questions, and Don't Tolerate Bullying.Take Notes.Read and Save Your Mail.Talk to Creditors, Not Collection Agencies.Get It in Writing.More items...?