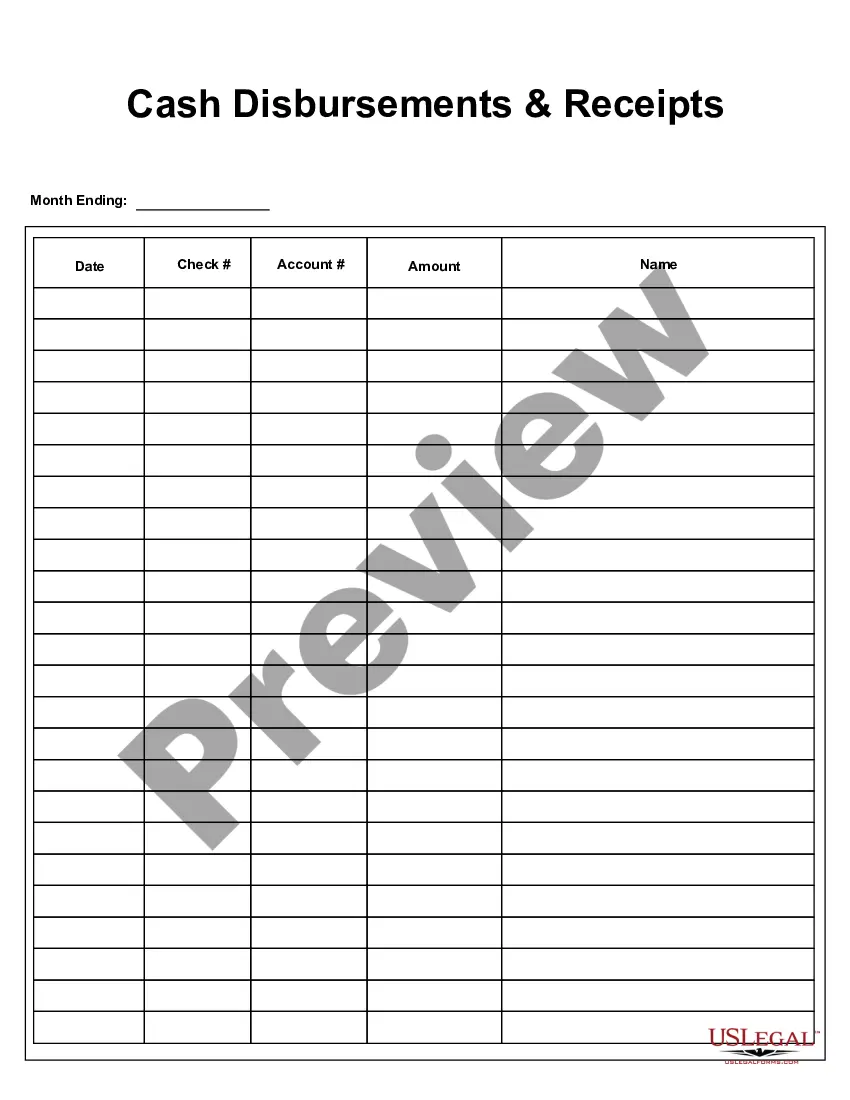

Iowa Cash Disbursements and Receipts Iowa Cash Disbursements and Receipts refer to the financial transactions involving the inflow and outflow of cash in the state of Iowa, United States. These transactions are crucial for tracking and managing the state's financial resources accurately. Iowa, being a governmental entity, follows specific processes and regulations to ensure transparency, accountability, and efficient management of cash disbursements and receipts. Cash disbursements in Iowa typically involve the payment of funds from the state treasury to various recipients, such as state agencies, vendors, employees, and contractors. These disbursements encompass a wide range of expenditures, including salaries and wages, procurement of goods and services, debt payments, grants and subsidies, and other authorized expenses. Each disbursement undergoes a thorough review process to verify its legitimacy and compliance with established financial rules. On the other hand, cash receipts in Iowa refer to the collection of funds by the state government. These receipts primarily originate from various sources, including taxes, fines, fees, licenses, permits, and other revenues generated by Iowa's governmental activities. Effective management of cash receipts is crucial for ensuring the availability of financial resources to support state operations, infrastructure development, public services, and other essential initiatives. There are several types of Iowa Cash Disbursements and Receipts, which play a significant role in the state's financial ecosystem. Some key variations and categories include: 1. Payroll Disbursements: Encompassing salary, wages, and benefit payments to state employees, payroll disbursements constitute a major portion of Iowa's cash outflow. 2. Vendor Disbursements: These disbursements involve payments to approved vendors and suppliers who provide goods, services, and equipment necessary for state operations. Proper contract management and compliance are crucial in this category. 3. Grants and Subsidies Disbursements: Iowa disburses cash for grants and subsidies to support various initiatives, such as education, healthcare, infrastructure projects, social welfare programs, and economic development. 4. Debt Payments: Iowa's cash disbursements also cover debt payments, including principal and interest payments for loans, bonds, and other financial obligations of the state. 5. Tax Receipts: One of the primary sources of cash receipts in Iowa is through the collection of taxes, such as income tax, sales tax, property tax, and other levies imposed by the state. These revenues enable the government to fund public services and meet its fiscal responsibilities. 6. License and Permit Receipts: Iowa collects cash through the issuance of licenses and permits across various sectors, such as business licenses, professional permits, vehicle registration fees, and other regulatory charges. 7. Fine and Fee Receipts: Cash receipts also include fines, penalties, and fees imposed for violations of state laws and regulations, traffic offenses, licenses and permit violations, and other non-tax related penalties. It is worth noting that Iowa's accounting processes, systems, and reporting frameworks comply with established governmental accounting standards to ensure accuracy, consistency, and transparency in documenting cash disbursements and receipts. Regular audits and financial reviews are conducted to maintain fiscal integrity and public trust in the state's financial operations.

Iowa Cash Disbursements and Receipts

Description

How to fill out Iowa Cash Disbursements And Receipts?

US Legal Forms - among the biggest libraries of legitimate kinds in the USA - offers a wide array of legitimate record themes it is possible to acquire or printing. Utilizing the website, you can get thousands of kinds for organization and individual reasons, sorted by groups, states, or keywords and phrases.You will discover the latest variations of kinds such as the Iowa Cash Disbursements and Receipts within minutes.

If you currently have a monthly subscription, log in and acquire Iowa Cash Disbursements and Receipts from your US Legal Forms collection. The Acquire switch will appear on every form you look at. You have accessibility to all previously downloaded kinds inside the My Forms tab of your respective accounts.

In order to use US Legal Forms the first time, allow me to share basic recommendations to help you get started off:

- Be sure to have picked out the proper form to your metropolis/area. Go through the Preview switch to examine the form`s articles. Look at the form description to ensure that you have selected the right form.

- In the event the form does not match your needs, make use of the Search area near the top of the display to discover the one that does.

- Should you be content with the shape, confirm your decision by clicking on the Acquire now switch. Then, pick the costs program you prefer and offer your credentials to register for the accounts.

- Method the deal. Make use of your Visa or Mastercard or PayPal accounts to accomplish the deal.

- Choose the formatting and acquire the shape on your own system.

- Make modifications. Fill up, edit and printing and signal the downloaded Iowa Cash Disbursements and Receipts.

Each web template you put into your account lacks an expiration time and is yours permanently. So, if you would like acquire or printing an additional backup, just check out the My Forms area and then click in the form you want.

Obtain access to the Iowa Cash Disbursements and Receipts with US Legal Forms, one of the most extensive collection of legitimate record themes. Use thousands of professional and status-specific themes that fulfill your business or individual requires and needs.