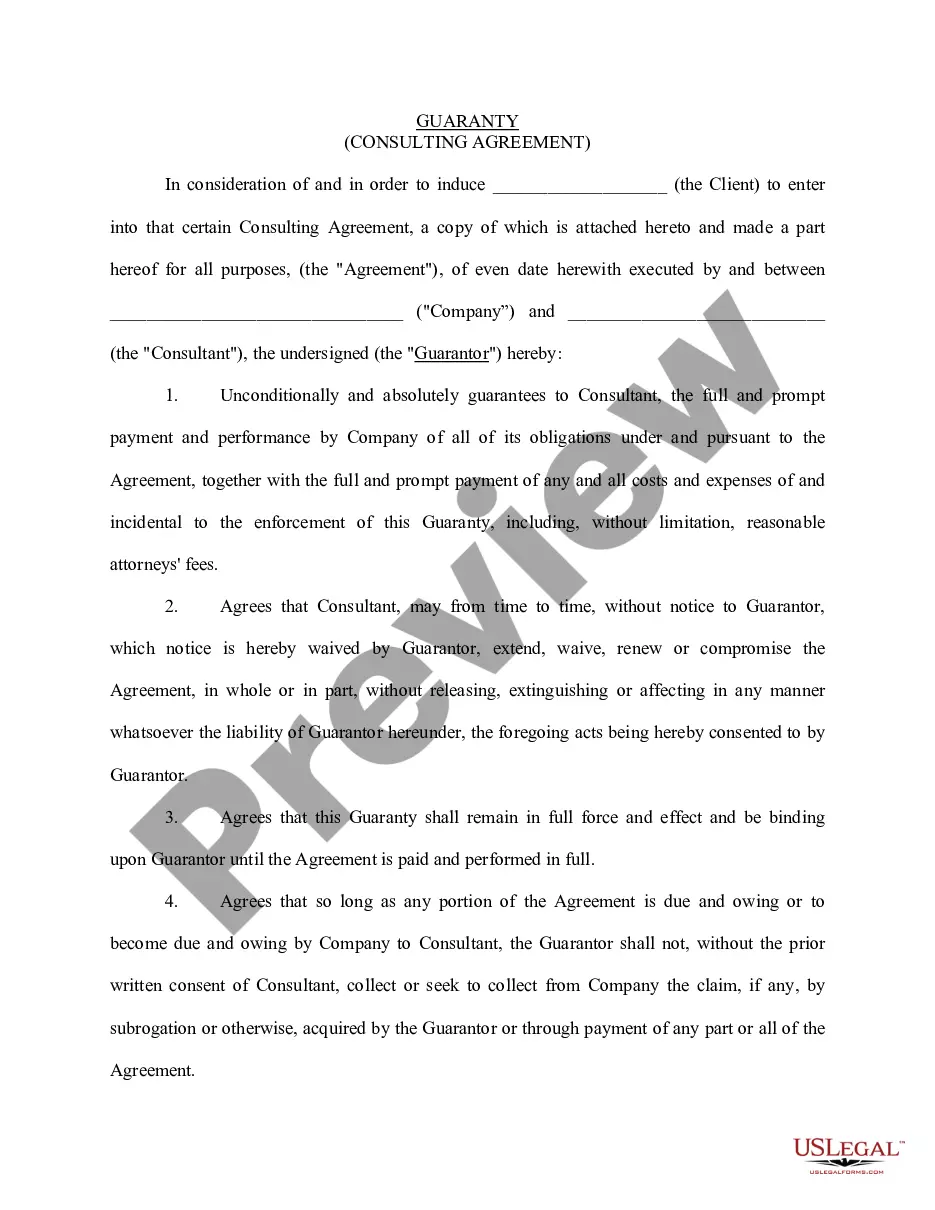

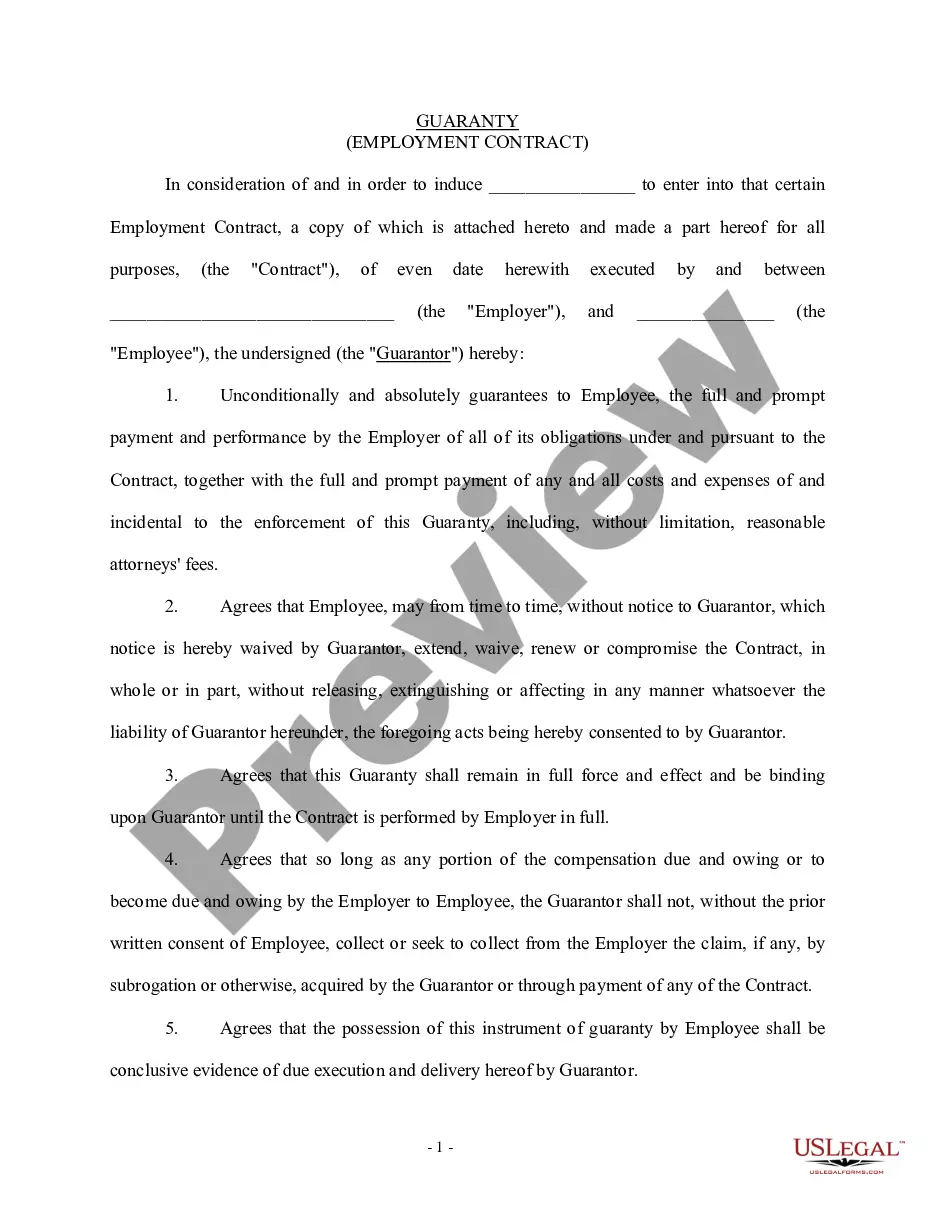

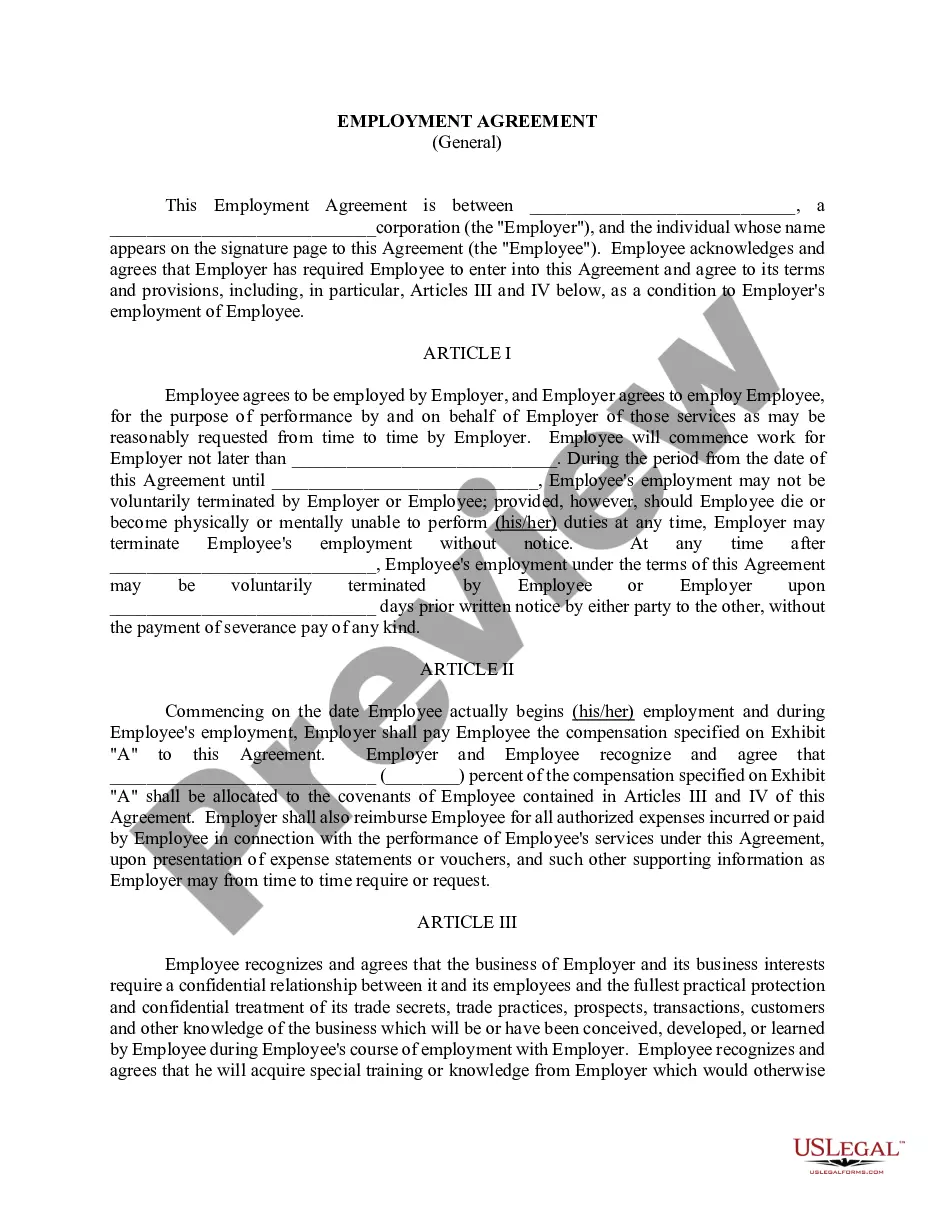

Iowa Personal Guaranty of Another Person's Agreement to Pay Consultant

Description

How to fill out Personal Guaranty Of Another Person's Agreement To Pay Consultant?

US Legal Forms - among the largest collections of legal documents in the United States - offers a broad array of legal document templates that you can download or print.

By using the website, you can discover thousands of forms for business and personal purposes, organized by categories, states, or keywords. You can find the latest versions of documents such as the Iowa Personal Guaranty of Another Person's Agreement to Pay Consultant in just minutes.

If you already possess a membership, Log In and download the Iowa Personal Guaranty of Another Person's Agreement to Pay Consultant from your US Legal Forms library. The Download option will be available on each document you view. You can access all previously saved forms in the My documents tab in your profile.

Process the transaction. Use a credit card or PayPal account to complete the transaction.

Select the format and download the document to your device. Make adjustments. Fill out, modify, print, and sign the saved Iowa Personal Guaranty of Another Person's Agreement to Pay Consultant. Every document you save in your account does not have an expiration date and is yours indefinitely. Therefore, to download or print another copy, simply navigate to the My documents section and click on the document you need. Access the Iowa Personal Guaranty of Another Person's Agreement to Pay Consultant with US Legal Forms, the most extensive collection of legal document templates. Utilize thousands of professional and state-specific templates that fulfill your business or personal needs.

- If you are using US Legal Forms for the first time, here are some simple steps to get started.

- Make sure you have selected the correct form for your city/state.

- Click the Review button to examine the content of the form.

- Check the form details to confirm that you have selected the right document.

- If the form does not meet your requirements, utilize the Search field at the top of the screen to find one that does.

- Once you are happy with the form, confirm your choice by clicking the Purchase now button.

- Then, select the payment plan you prefer and provide your information to register for an account.

Form popularity

FAQ

An otherwise valid and enforceable personal guarantee can be revoked later in several different ways. A guaranty, much like any other contract, can be revoked later if both the guarantor and the lender agree in writing. Some debts owed by personal guarantors can also be discharged in bankruptcy.

7 Ways to Avoid a Personal GuaranteeBuy insurance.Raise the interest rate.Increase Reporting.Increased the Frequency of Payments.Add a Fidelity Certificate.Limit the Guarantee Time Period.Use Other Collateral.

Your personal guarantee may be unenforceable due to circumstances outside of your contract. This may include being misled by the creditor, if a key fact was omitted from the contract, co-guarantor issues, suspicions of fraud, or if the facility provided by the bank changed significantly since you signed the guarantee.

If you sign a personal guarantee, you are personally liable for the loan balance or a portion thereof. If your business later defaults on the loan, anyone who signed the personal guarantee can be held responsible for the remaining balance, even after the lender forecloses on the loan collateral.

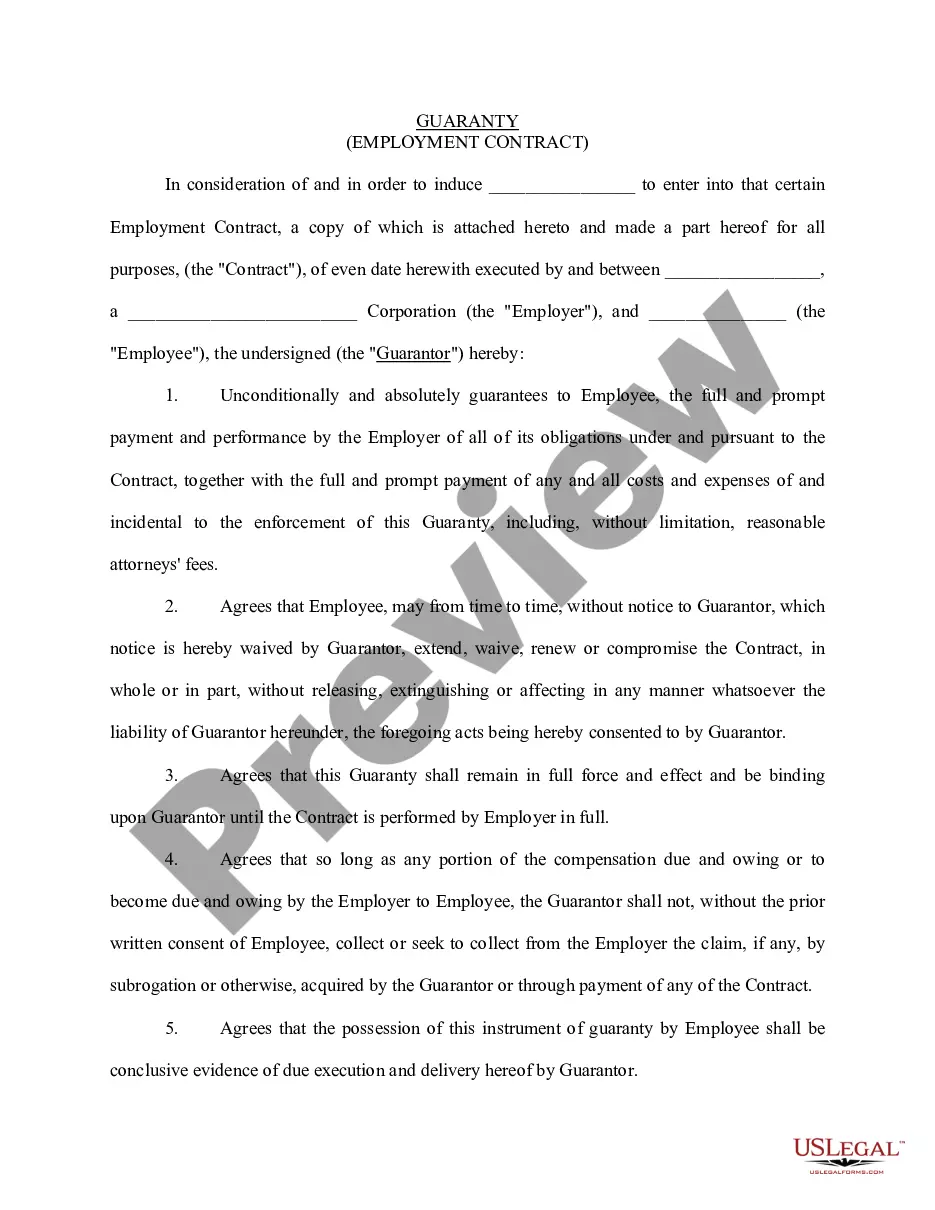

A personal guaranty is not enforceable without consideration A contract is an enforceable promise. The enforceability of a contract comes from one party's giving of consideration to the other party. Here, the bank gives a loan (the consideration) in exchange for the guarantor's promise to repay it.

A personal guarantee can be enforced the same way as any debt. If the business owner does not pay, the creditor can bring a lawsuit to receive a judgment and levy the owner's personal assets to cover the debt. The exact terms of a personal guarantee specify a creditor's options under the guarantee.

The guaranty shall continue in full force and effect and may only be terminated in a writing delivered to Y thirty days before termination of the guaranty and such termination shall not eliminate the guaranty as to sums already advanced.

A personal guarantee is an individual's legal promise to repay credit issued to a business for which they serve as an executive or partner. Personal guarantees help businesses get credit when they aren't as established or have an inadequate credit history to qualify on their own.

A surety cannot be treated as a bank guarantee. A surety is liable for any performance risk shown by a principal; the bank guarantee is liable only for the financial risk of a contracted project.

A guarantor is a financial term describing an individual who promises to pay a borrower's debt in the event that the borrower defaults on their loan obligation. Guarantors pledge their own assets as collateral against the loans.