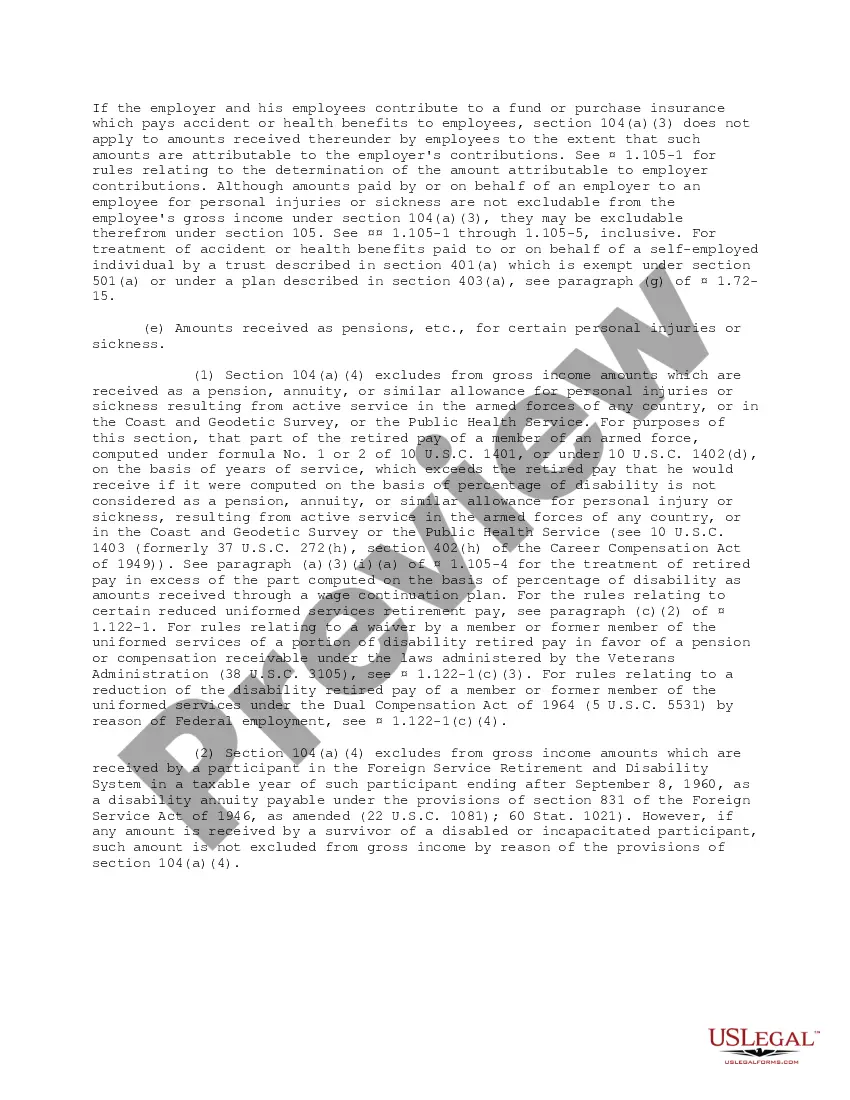

Statutory Guidelines [Appendix A(2) Tres. Reg 104-1] regarding compensation for injuries or sickness under workmen's compensation acts, damages, accident or health insurance, etc. as stated in the guidelines.

Iowa Compensation for Injuries or Sickness Treasury Regulation 104.1 is a significant regulation that outlines the tax treatment of amounts received by individuals as compensation for injuries or sickness. This regulation is crucial for individuals residing in Iowa, ensuring they receive fair treatment in terms of taxes on compensation received due to injuries or sickness. Understanding this regulation and its different types is essential for proper tax compliance in such cases. The primary purpose of Iowa Compensation for Injuries or Sickness Treasury Regulation 104.1 is to provide guidance on how to determine the tax ability of compensation received by individuals. It helps ensure fairness in the tax treatment of such amounts, considering the nature and purpose of the compensation. By providing clear guidelines, the regulation aims to protect the rights and interests of Iowa residents facing injuries or sickness. One type of Iowa Compensation for Injuries or Sickness Treasury Regulation 104.1 is compensation received as a result of personal physical injuries or physical sickness. This type of compensation generally follows tax-exempt treatment, allowing individuals to exclude the received amount from their taxable income. It acknowledges the need for financial relief for those suffering from physical harm or illness and ensures that they do not face additional tax burdens during such challenging times. Another type of compensation addressed by Iowa Compensation for Injuries or Sickness Treasury Regulation 104.1 is the compensation received for non-physical injuries or non-physical sickness. This includes emotional distress, mental anguish, or defamation-related cases where the harm is not physical in nature. Such types of compensation may be partially taxable, subject to certain limitations and conditions outlined in the regulation. In addition to the types mentioned above, Iowa Compensation for Injuries or Sickness Treasury Regulation 104.1 also covers compensation received for medical expenses related to injuries or sickness. This includes amounts received to cover medical bills, hospitalization costs, medication expenses, and other healthcare expenses. The regulation provides guidance on how to handle the tax treatment of such payments, ensuring fair and consistent taxation in these cases. Overall, Iowa Compensation for Injuries or Sickness Treasury Regulation 104.1 is a crucial regulation that ensures fair tax treatment for individuals receiving compensation due to injuries or sickness. It provides clarity on various types of compensation and guides taxpayers to appropriately report and handle such amounts on their tax returns. By adhering to this regulation, Iowa residents can ensure compliance with tax laws while obtaining relief for their physical or non-physical injuries and illnesses.Iowa Compensation for Injuries or Sickness Treasury Regulation 104.1 is a significant regulation that outlines the tax treatment of amounts received by individuals as compensation for injuries or sickness. This regulation is crucial for individuals residing in Iowa, ensuring they receive fair treatment in terms of taxes on compensation received due to injuries or sickness. Understanding this regulation and its different types is essential for proper tax compliance in such cases. The primary purpose of Iowa Compensation for Injuries or Sickness Treasury Regulation 104.1 is to provide guidance on how to determine the tax ability of compensation received by individuals. It helps ensure fairness in the tax treatment of such amounts, considering the nature and purpose of the compensation. By providing clear guidelines, the regulation aims to protect the rights and interests of Iowa residents facing injuries or sickness. One type of Iowa Compensation for Injuries or Sickness Treasury Regulation 104.1 is compensation received as a result of personal physical injuries or physical sickness. This type of compensation generally follows tax-exempt treatment, allowing individuals to exclude the received amount from their taxable income. It acknowledges the need for financial relief for those suffering from physical harm or illness and ensures that they do not face additional tax burdens during such challenging times. Another type of compensation addressed by Iowa Compensation for Injuries or Sickness Treasury Regulation 104.1 is the compensation received for non-physical injuries or non-physical sickness. This includes emotional distress, mental anguish, or defamation-related cases where the harm is not physical in nature. Such types of compensation may be partially taxable, subject to certain limitations and conditions outlined in the regulation. In addition to the types mentioned above, Iowa Compensation for Injuries or Sickness Treasury Regulation 104.1 also covers compensation received for medical expenses related to injuries or sickness. This includes amounts received to cover medical bills, hospitalization costs, medication expenses, and other healthcare expenses. The regulation provides guidance on how to handle the tax treatment of such payments, ensuring fair and consistent taxation in these cases. Overall, Iowa Compensation for Injuries or Sickness Treasury Regulation 104.1 is a crucial regulation that ensures fair tax treatment for individuals receiving compensation due to injuries or sickness. It provides clarity on various types of compensation and guides taxpayers to appropriately report and handle such amounts on their tax returns. By adhering to this regulation, Iowa residents can ensure compliance with tax laws while obtaining relief for their physical or non-physical injuries and illnesses.