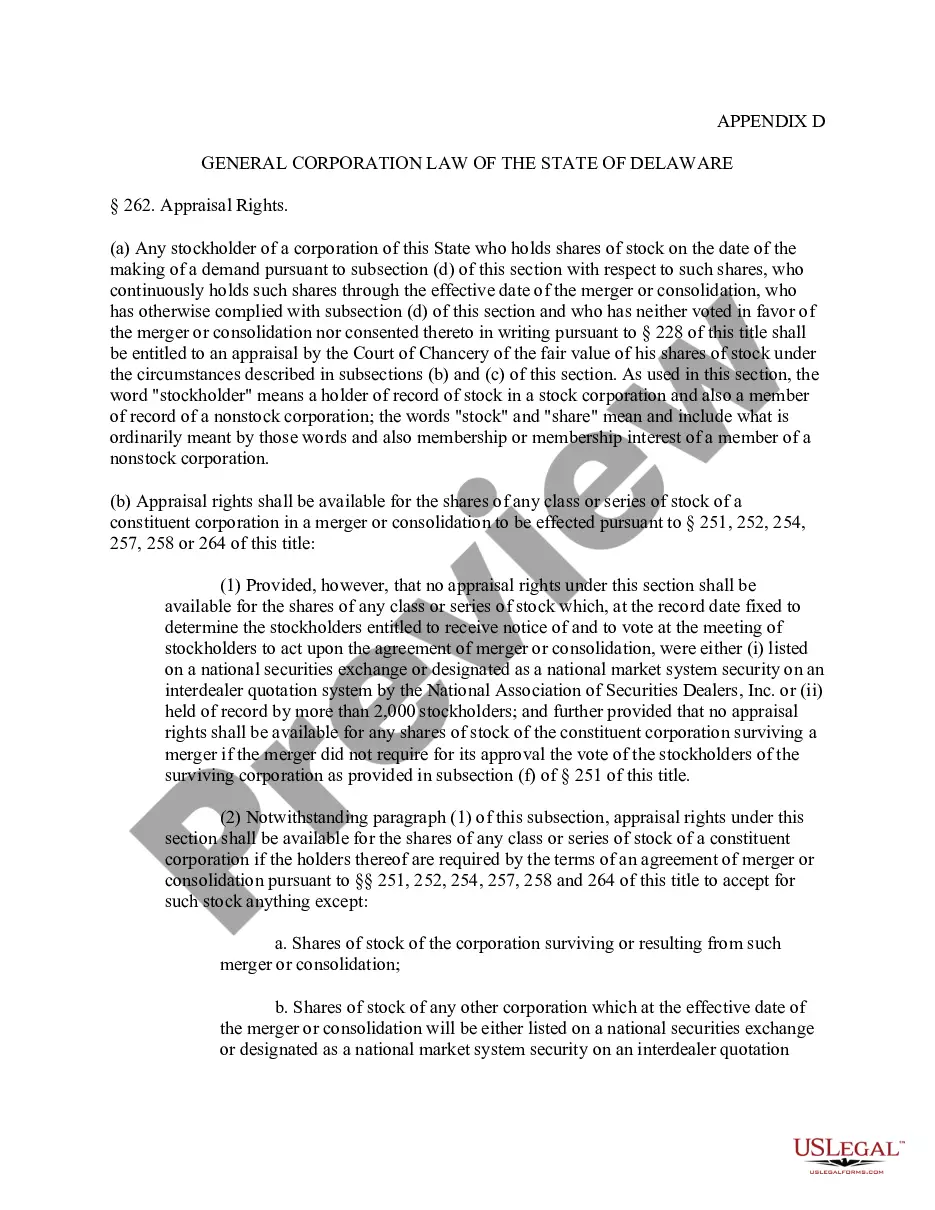

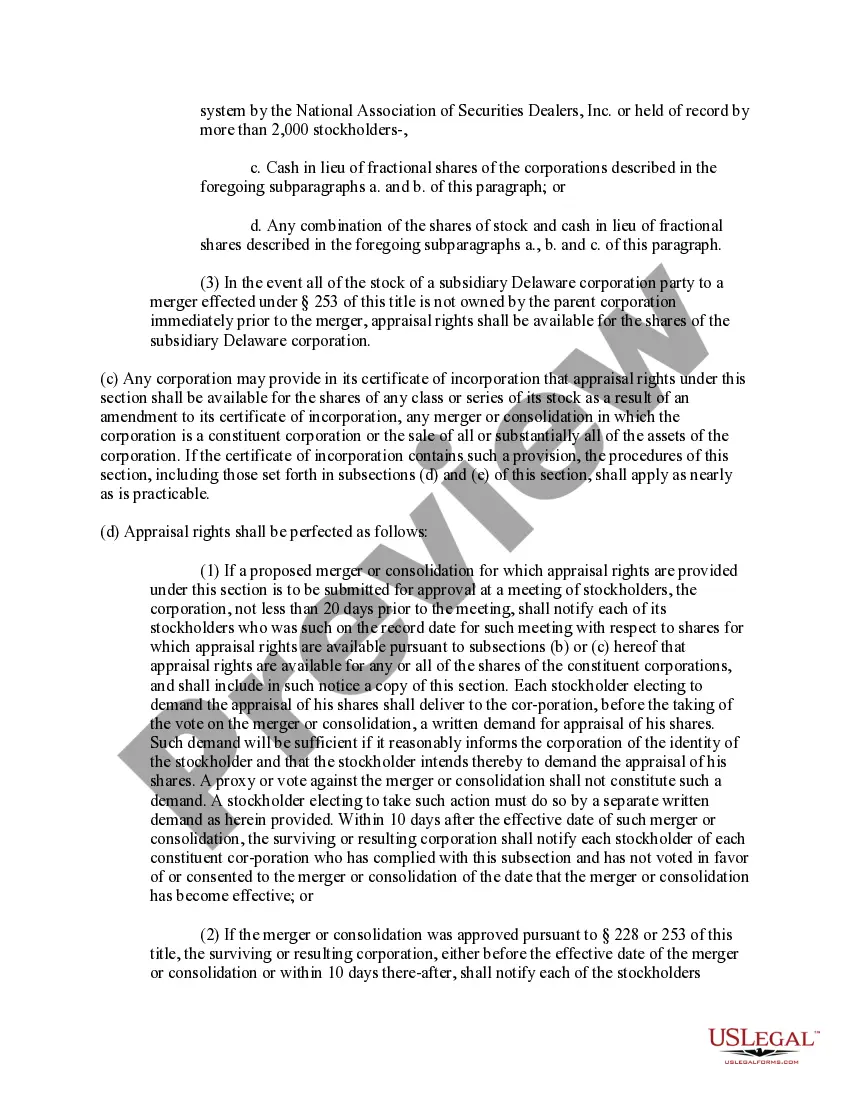

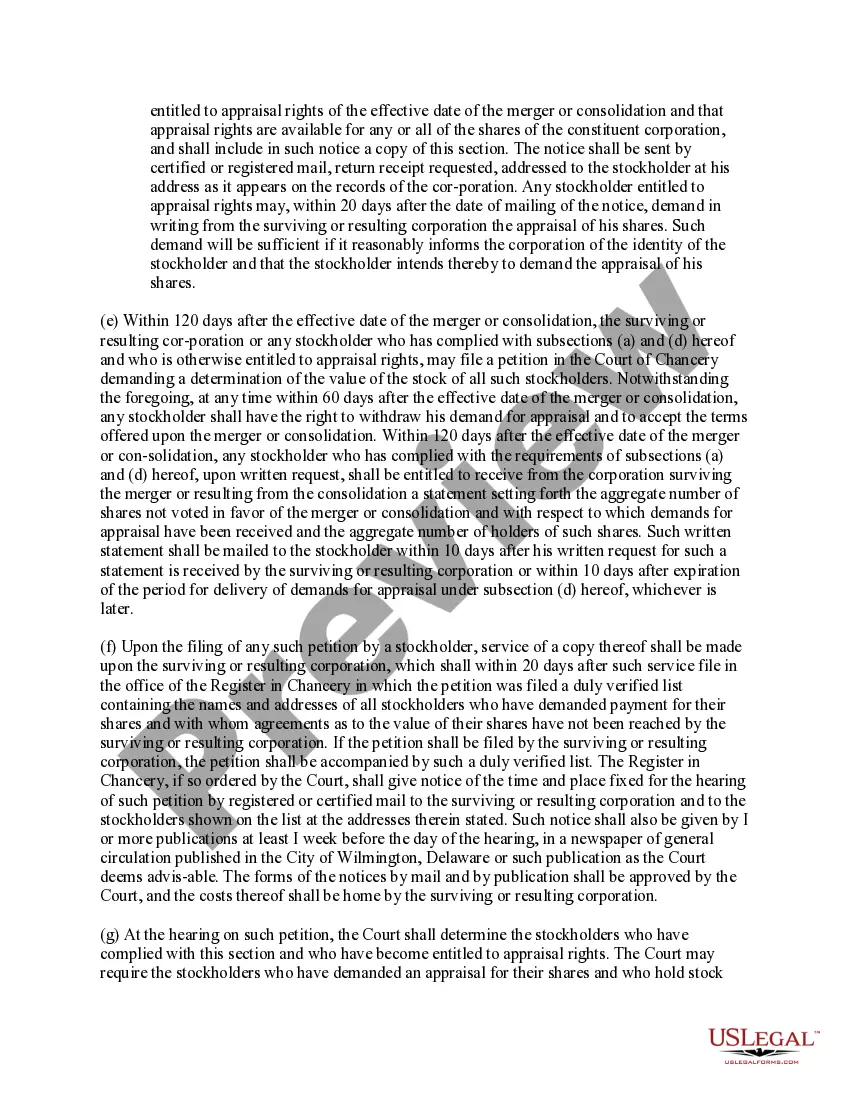

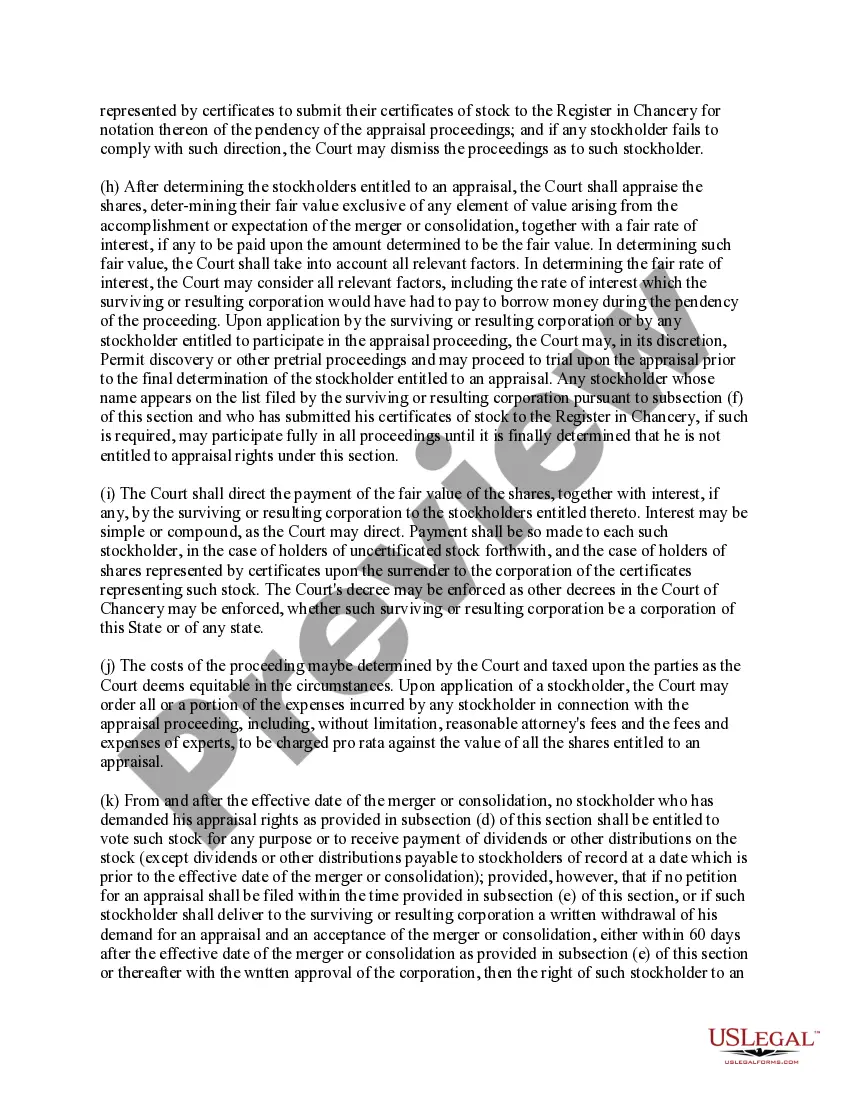

Iowa Section 262 of the Delaware General Corporation Law, also known as the appraisal rights provision, is a crucial statute that provides shareholders of a Delaware corporation with the right to have their shares appraised and to potentially receive fair value compensation in certain merger or consolidation situations. This provision is essential to protect shareholders' interests and ensure they receive just and equitable treatment when their company undergoes significant corporate actions. The Iowa Section 262 can be exercised by dissenting shareholders who oppose a proposed merger or consolidation with another entity. These shareholders have the option to dissent from the transaction and seek an appraisal of their shares to determine their fair value. By exercising their appraisal rights, shareholders can potentially receive payment for their shares that is higher than the merger consideration offered by the acquiring entity. However, Iowa Section 262 also imposes certain limitations and requirements for shareholders looking to invoke their appraisal rights. For instance, shareholders must meet specific procedural requirements, such as providing written notice of their intent to demand an appraisal, within a specified timeframe following the announcement of the proposed transaction. Failure to comply with these requirements may result in the loss of appraisal rights. It is important to note that there may be different types or variants of the Iowa Section 262 provision under the Delaware General Corporation Law, focusing on various aspects of appraisal rights. These may include: 1. Pre-merger Appraisal Rights: This type of Iowa Section 262 governs shareholders' rights to appraisal before a merger or consolidation is approved and finalized. It allows dissenting shareholders to demand an appraisal of their shares and potentially receive fair value compensation. 2. Post-merger Appraisal Rights: This variant of the Iowa Section 262 addresses shareholders' rights to appraisal after a merger or consolidation is completed. Dissenting shareholders can seek an appraisal of their shares to assess fair value and potentially receive compensation accordingly. 3. Exceptions and Limitations: This type of Iowa Section 262 provision may outline specific exceptions and limitations to appraisal rights. It may address scenarios where shareholders may not exercise their appraisal rights, such as in certain short-form mergers or transactions involving certain controlling shareholders. Iowa Section 262 of the Delaware General Corporation Law, with its several variations, represents a crucial legal framework for dissenting shareholders in Delaware corporations. It ensures that dissenting shareholders have a fair opportunity to protect their investment and obtain just compensation in merger or consolidation transactions. Adhering to the specific requirements and understanding the different types of Iowa Section 262 provisions is pivotal for shareholders seeking to exercise their appraisal rights effectively.

Iowa Section 262 of the Delaware General Corporation Law

Description

How to fill out Iowa Section 262 Of The Delaware General Corporation Law?

US Legal Forms - one of many biggest libraries of legal forms in America - provides a variety of legal file templates you can obtain or print out. While using site, you will get a huge number of forms for enterprise and personal uses, sorted by types, claims, or key phrases.You will discover the newest variations of forms much like the Iowa Section 262 of the Delaware General Corporation Law in seconds.

If you already have a registration, log in and obtain Iowa Section 262 of the Delaware General Corporation Law from the US Legal Forms library. The Down load button will show up on every develop you view. You gain access to all previously acquired forms in the My Forms tab of your respective profile.

In order to use US Legal Forms the first time, allow me to share simple guidelines to help you started out:

- Make sure you have selected the right develop to your town/state. Click on the Review button to examine the form`s articles. See the develop information to actually have selected the correct develop.

- In the event the develop does not suit your needs, utilize the Look for field towards the top of the display screen to find the the one that does.

- Should you be satisfied with the form, confirm your selection by clicking on the Acquire now button. Then, select the prices prepare you favor and supply your references to sign up for an profile.

- Process the purchase. Make use of your Visa or Mastercard or PayPal profile to complete the purchase.

- Find the formatting and obtain the form in your product.

- Make adjustments. Load, modify and print out and indicator the acquired Iowa Section 262 of the Delaware General Corporation Law.

Every single template you put into your account does not have an expiration date and is your own property eternally. So, if you want to obtain or print out another backup, just proceed to the My Forms segment and click in the develop you will need.

Obtain access to the Iowa Section 262 of the Delaware General Corporation Law with US Legal Forms, the most extensive library of legal file templates. Use a huge number of expert and status-particular templates that satisfy your small business or personal needs and needs.