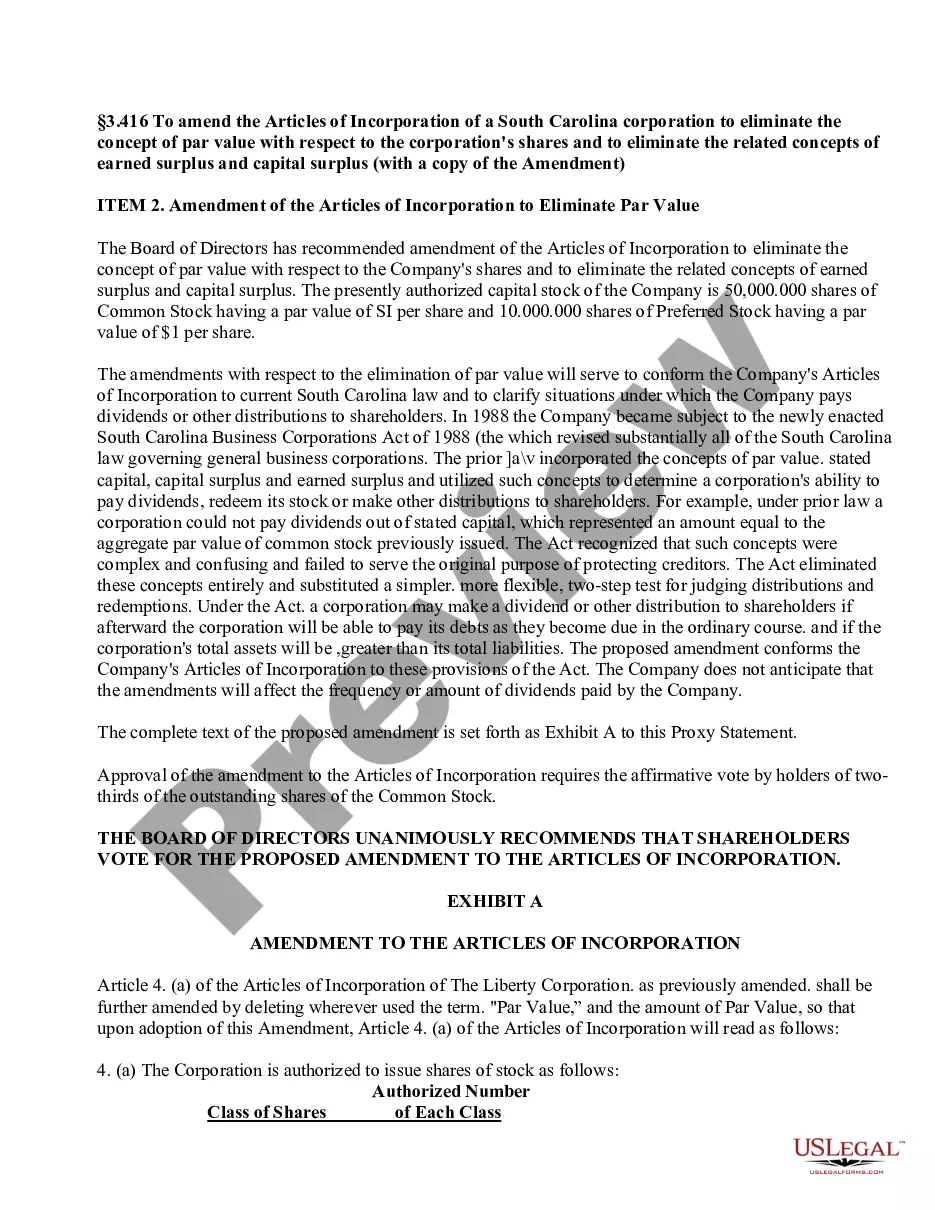

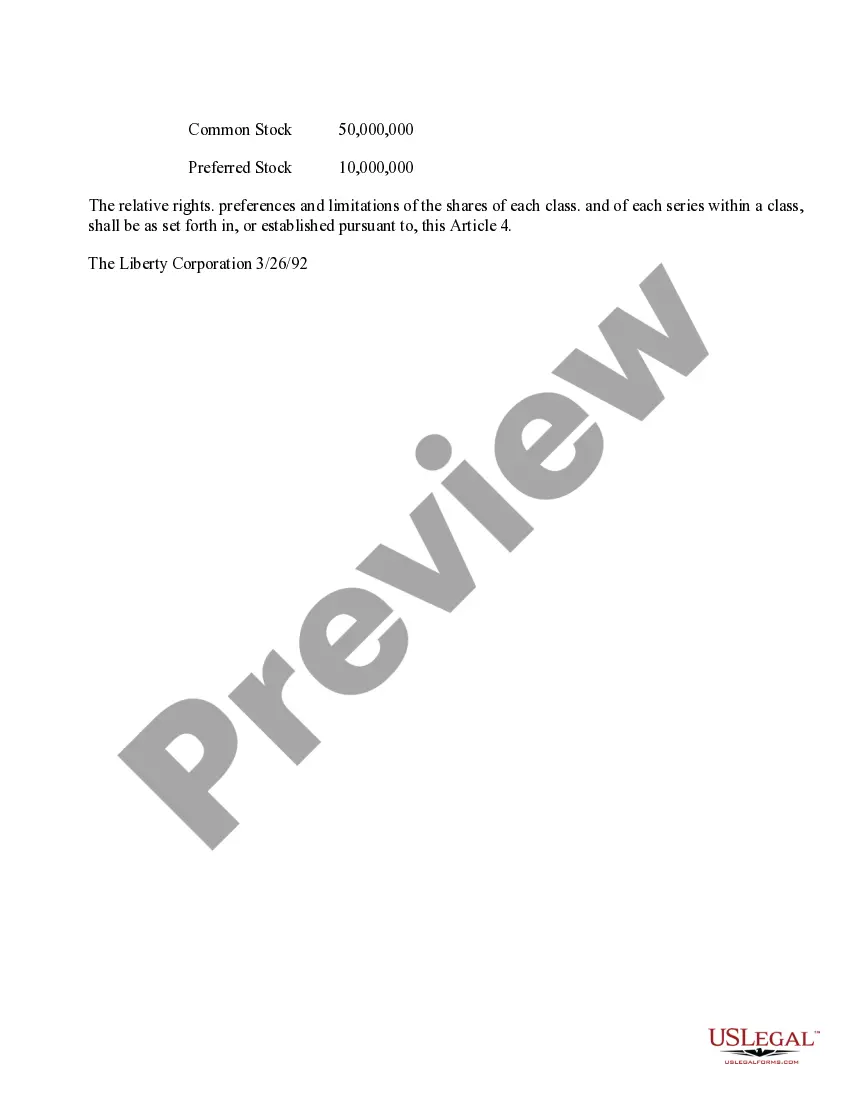

The Iowa Amendment to the Articles of Incorporation allows companies to eliminate the concept of par value for their shares. Par value refers to the minimum price for which each share can be issued and is usually set at a nominal value such as $0.01 or $0.10. By eliminating par value, companies gain more flexibility in determining the price of their shares, as there is no longer a minimum threshold. This amendment is crucial for companies seeking to adapt to changing market conditions, attract potential investors, or accommodate for future fundraising rounds. Moreover, eliminating par value can simplify share transactions and decrease administrative burdens, as there are no longer strict pricing requirements. There are primarily two types of Iowa Amendments relating to the elimination of par value: 1. Iowa Amendment to Eliminate Par Value: This amendment is the standard and most common amendment that simply eliminates the concept of par value from a company's articles of incorporation. It provides companies the freedom to assign any value they see fit to their shares, whether below or above the previous par value requirement. 2. Iowa Amendment to Set Stated Capital: In some cases, companies may choose to eliminate par value but still establish a stated capital for their shares. Stated capital represents the book value of shares, reflecting the total capital received from the issuance of those shares. This amendment allows companies to determine the stated capital based on their specific needs, goals, and financial strategies. These Iowa Amendments to the Articles of Incorporation are essential tools for companies looking for greater flexibility in pricing their shares and adapting to market changes. By eliminating par value, companies can optimize their capital structure and simplify share transactions, ultimately positioning themselves for growth and success in the dynamic business landscape.

Iowa Amendment to the articles of incorporation to eliminate par value

Description

How to fill out Iowa Amendment To The Articles Of Incorporation To Eliminate Par Value?

You may spend hrs on the web looking for the legal papers design which fits the federal and state requirements you require. US Legal Forms offers 1000s of legal varieties which are analyzed by specialists. You can actually acquire or print the Iowa Amendment to the articles of incorporation to eliminate par value from our services.

If you have a US Legal Forms profile, you may log in and then click the Obtain option. Afterward, you may comprehensive, edit, print, or indicator the Iowa Amendment to the articles of incorporation to eliminate par value. Each and every legal papers design you buy is yours eternally. To get an additional version of the purchased kind, go to the My Forms tab and then click the related option.

If you are using the US Legal Forms web site initially, stick to the straightforward recommendations beneath:

- Very first, make certain you have selected the right papers design for that state/area that you pick. Browse the kind information to make sure you have selected the right kind. If readily available, make use of the Preview option to appear with the papers design too.

- If you want to get an additional version from the kind, make use of the Research field to obtain the design that suits you and requirements.

- Upon having located the design you want, click Buy now to proceed.

- Pick the costs prepare you want, key in your accreditations, and register for a merchant account on US Legal Forms.

- Full the deal. You can use your Visa or Mastercard or PayPal profile to cover the legal kind.

- Pick the file format from the papers and acquire it in your system.

- Make adjustments in your papers if necessary. You may comprehensive, edit and indicator and print Iowa Amendment to the articles of incorporation to eliminate par value.

Obtain and print 1000s of papers templates using the US Legal Forms web site, that offers the most important assortment of legal varieties. Use skilled and status-certain templates to take on your business or person needs.

Form popularity

FAQ

To make amendments to your Iowa articles of incorporation, submit amendments to the Iowa Secretary of State, Business Services (SOS). The document can be filed by mail, fax, or in person.

Par value means the minimum price at which a corporation can sell its shares to its shareholders. Setting a par value is required when forming a corporation in some states, but it is not required when forming a corporation in other states, such as Oregon.

490.1505 Activities not constituting doing business.

A par value of $0.01 for common stocks in finance means that the declared value of the common stock in the articles of incorporation is $0.01. The other term for par value is face value because it is the amount on the face of the corporation's charter or the stock certificate.

490.1106 Articles of merger or share exchange.

Time limits for most types of civil cases in Iowa range from two to five years, while most serious misdemeanors have a three-year statute of limitations.