Iowa Plan of complete liquidation and dissolution

Description

How to fill out Plan Of Complete Liquidation And Dissolution?

US Legal Forms - among the biggest libraries of legitimate types in the States - offers a variety of legitimate document templates you are able to obtain or print. While using website, you will get 1000s of types for organization and person uses, categorized by categories, claims, or search phrases.You will find the most recent types of types much like the Iowa Plan of complete liquidation and dissolution within minutes.

If you already have a registration, log in and obtain Iowa Plan of complete liquidation and dissolution from the US Legal Forms catalogue. The Down load switch can look on each and every kind you perspective. You gain access to all in the past downloaded types from the My Forms tab of your respective accounts.

In order to use US Legal Forms initially, listed here are simple guidelines to obtain started:

- Be sure you have picked the correct kind for your personal area/county. Click on the Review switch to examine the form`s content material. Look at the kind information to ensure that you have chosen the correct kind.

- If the kind doesn`t fit your specifications, take advantage of the Research area at the top of the display screen to get the the one that does.

- If you are content with the shape, verify your choice by simply clicking the Purchase now switch. Then, choose the rates plan you like and supply your credentials to sign up to have an accounts.

- Process the purchase. Make use of your bank card or PayPal accounts to perform the purchase.

- Choose the formatting and obtain the shape in your system.

- Make alterations. Load, revise and print and sign the downloaded Iowa Plan of complete liquidation and dissolution.

Each template you included in your money does not have an expiry day and is your own property forever. So, if you wish to obtain or print one more backup, just visit the My Forms segment and click around the kind you require.

Get access to the Iowa Plan of complete liquidation and dissolution with US Legal Forms, by far the most extensive catalogue of legitimate document templates. Use 1000s of expert and status-particular templates that meet your small business or person needs and specifications.

Form popularity

FAQ

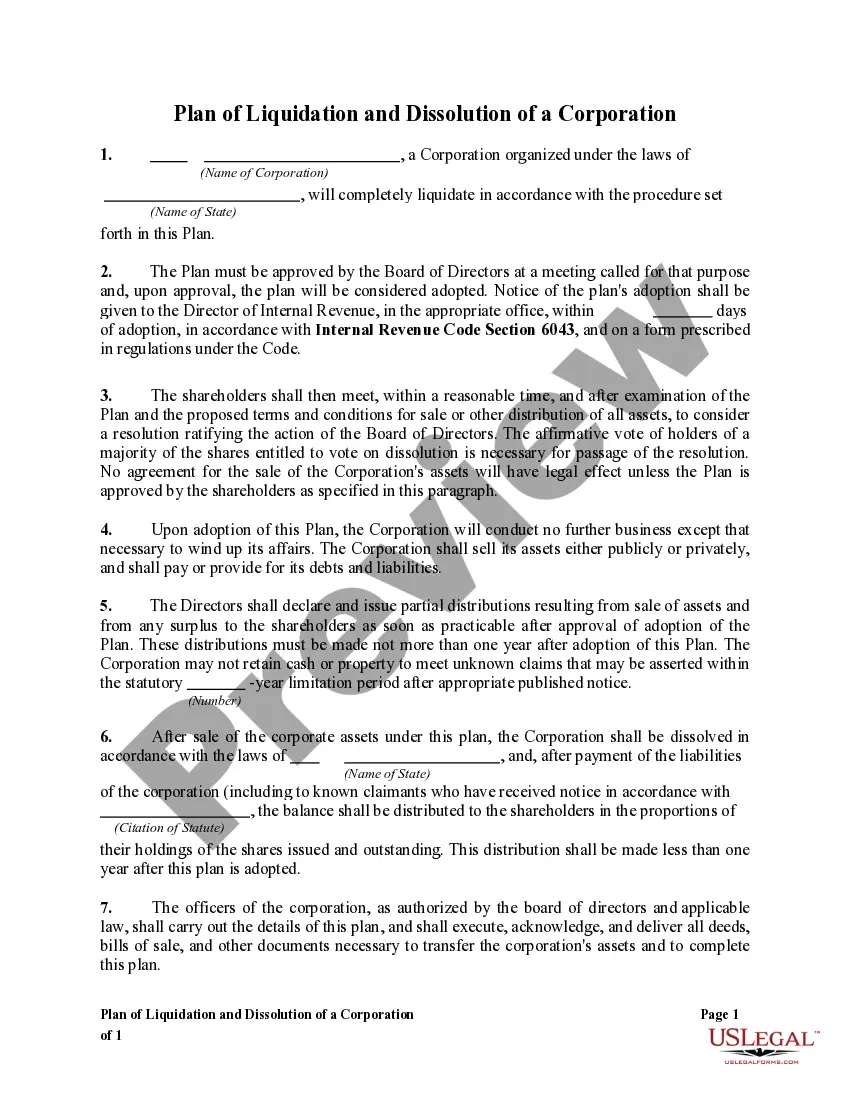

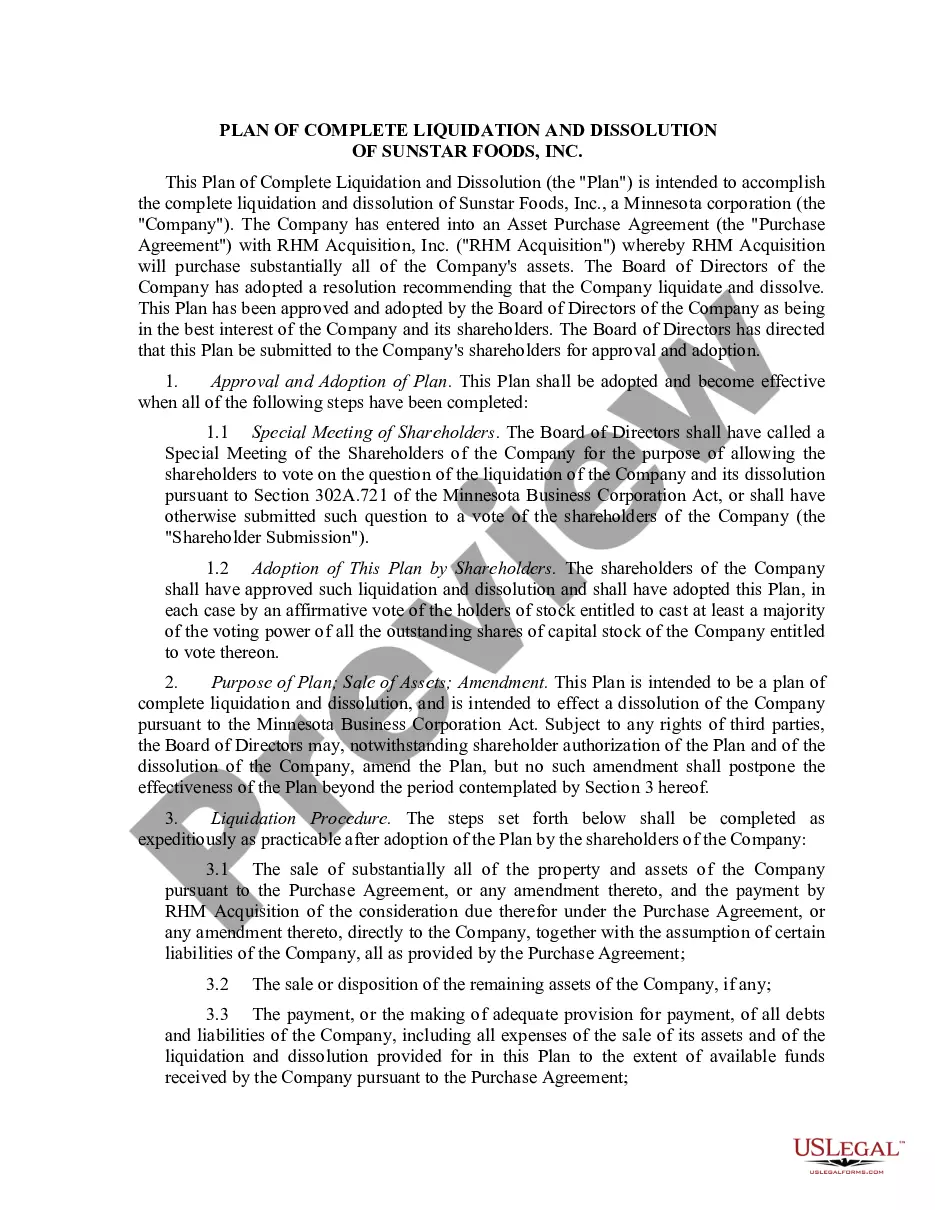

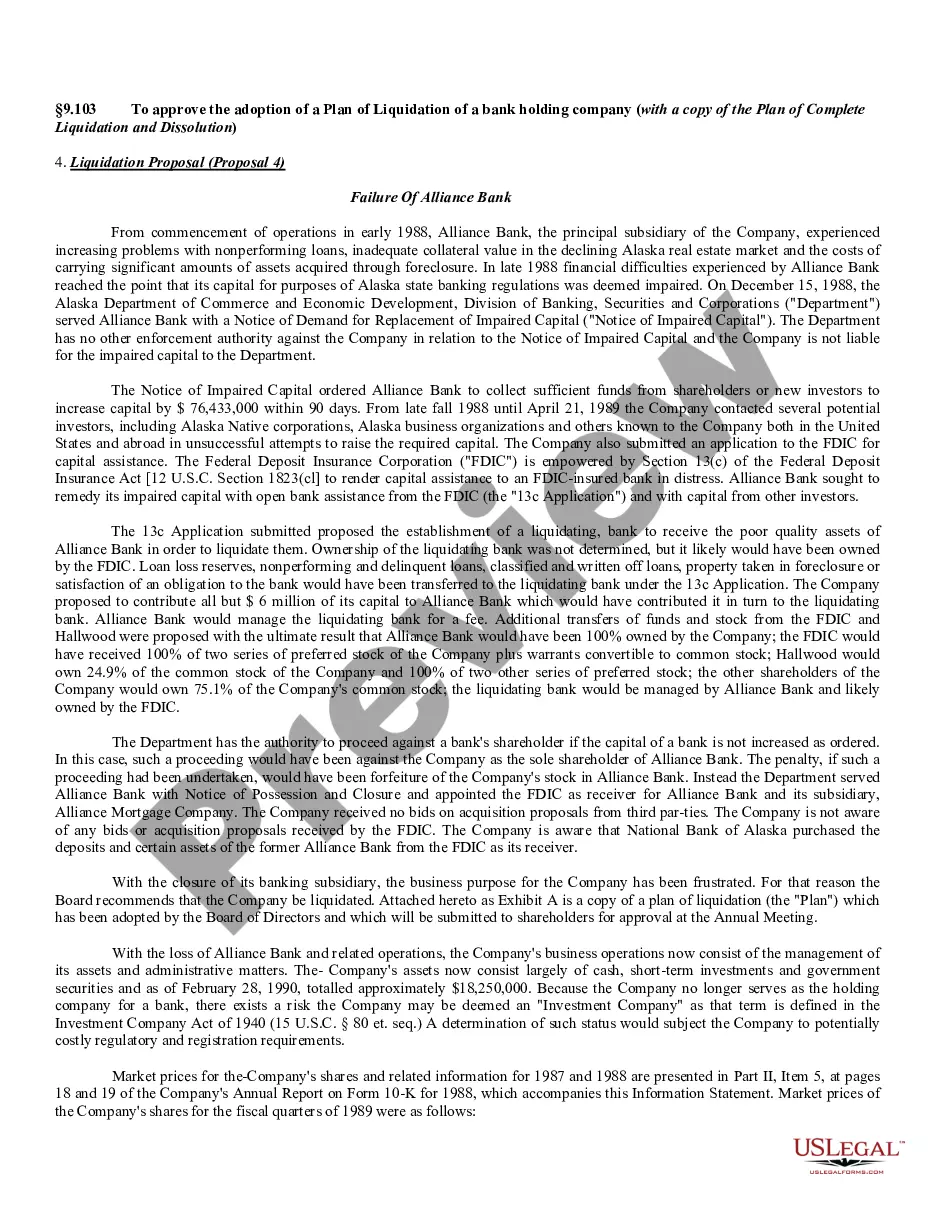

A plan of dissolution is a written description of how an entity intends to dissolve, or officially and formally close the business. A plan of dissolution will include a description of how any remaining assets and liabilities will be distributed.

The liquidating corporation distributes all of its assets to its shareholders, the assets are distributed in one or a series of distributions, the distributions are in redemption of all of the corporation's stock, the distributions are made pursuant to a plan of liquidation.

What are the differences between liquidation and dissolution? Dissolving a company through the process of dissolution often takes place when a company is solvent, but is no longer trading. Liquidation however, occurs due to a company having financial difficulties and therefore being unable to keep up with their debts.

To help you have a better understanding of what you should do, here is a simple step-by-step guide: Step 1: File the Articles of Dissolution. As stated earlier, dissolving an LLC requires you to submit formal paperwork. ... Step 2: Close any business tax accounts. ... Step 3: Complete the winding-up process.

A plan of dissolution is a written description of how an entity intends to dissolve, or officially and formally close the business. A plan of dissolution will include a description of how any remaining assets and liabilities will be distributed.

How do you dissolve an Iowa Corporation? To dissolve your Iowa corporation, file Articles of Dissolution with the Secretary of State (SOS). There is no SOS dissolution form. Draft your Articles of Dissolution and submit the document and filing fee to the Iowa Secretary of State, Business Services Division (SOS).

The quick answer. Liquidate means a formal closing down by a liquidator when there are still assets and liabilities to be dealt with. Dissolving a company is where the business is struck off the register at Companies House because it is now inactive.

A plan of liquidation and dissolution that can be used for the dissolution of a Delaware corporation wholly owned by a US parent corporation when the parties intend to qualify the dissolution as a tax-free liquidation under Sections 332 and 337 of the Internal Revenue Code.