Iowa First Meeting Minutes of Sole Director

Description

How to fill out First Meeting Minutes Of Sole Director?

If you wish to total, down load, or produce lawful file themes, use US Legal Forms, the greatest assortment of lawful varieties, which can be found online. Use the site`s easy and handy research to find the paperwork you will need. Various themes for business and individual purposes are sorted by classes and claims, or key phrases. Use US Legal Forms to find the Iowa First Meeting Minutes of Sole Director with a couple of clicks.

Should you be currently a US Legal Forms client, log in to the accounts and click on the Down load option to obtain the Iowa First Meeting Minutes of Sole Director. You can even accessibility varieties you earlier acquired in the My Forms tab of your respective accounts.

If you use US Legal Forms the very first time, refer to the instructions beneath:

- Step 1. Be sure you have selected the form for that proper area/nation.

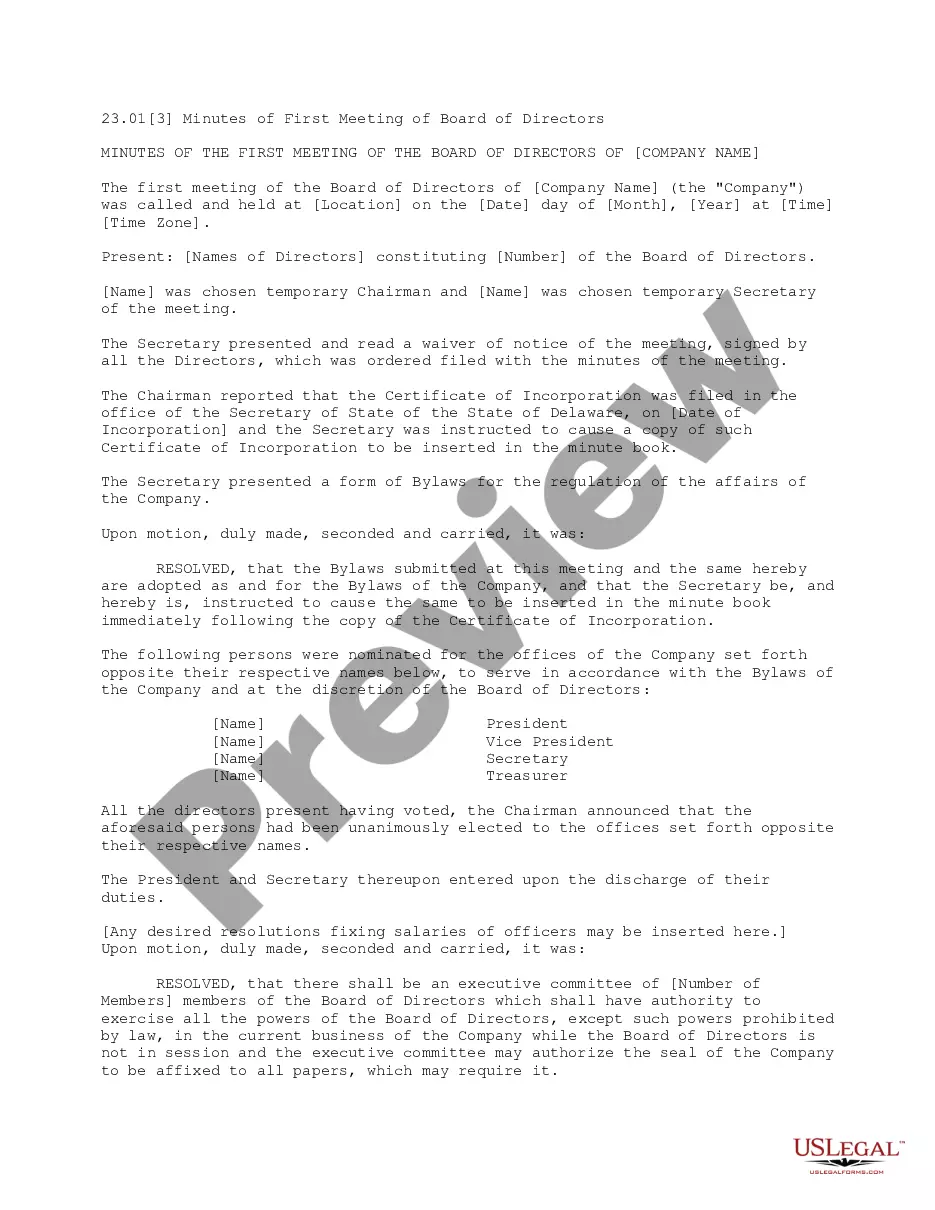

- Step 2. Use the Preview option to check out the form`s content material. Don`t overlook to learn the description.

- Step 3. Should you be unhappy with all the type, take advantage of the Look for field near the top of the display to discover other types from the lawful type design.

- Step 4. After you have located the form you will need, click the Get now option. Select the rates prepare you prefer and put your qualifications to sign up for an accounts.

- Step 5. Procedure the transaction. You should use your credit card or PayPal accounts to finish the transaction.

- Step 6. Choose the format from the lawful type and down load it on your own device.

- Step 7. Full, modify and produce or signal the Iowa First Meeting Minutes of Sole Director.

Every single lawful file design you purchase is your own property permanently. You may have acces to each and every type you acquired within your acccount. Click the My Forms area and decide on a type to produce or down load once more.

Remain competitive and down load, and produce the Iowa First Meeting Minutes of Sole Director with US Legal Forms. There are thousands of expert and state-certain varieties you can use for your business or individual requirements.

Form popularity

FAQ

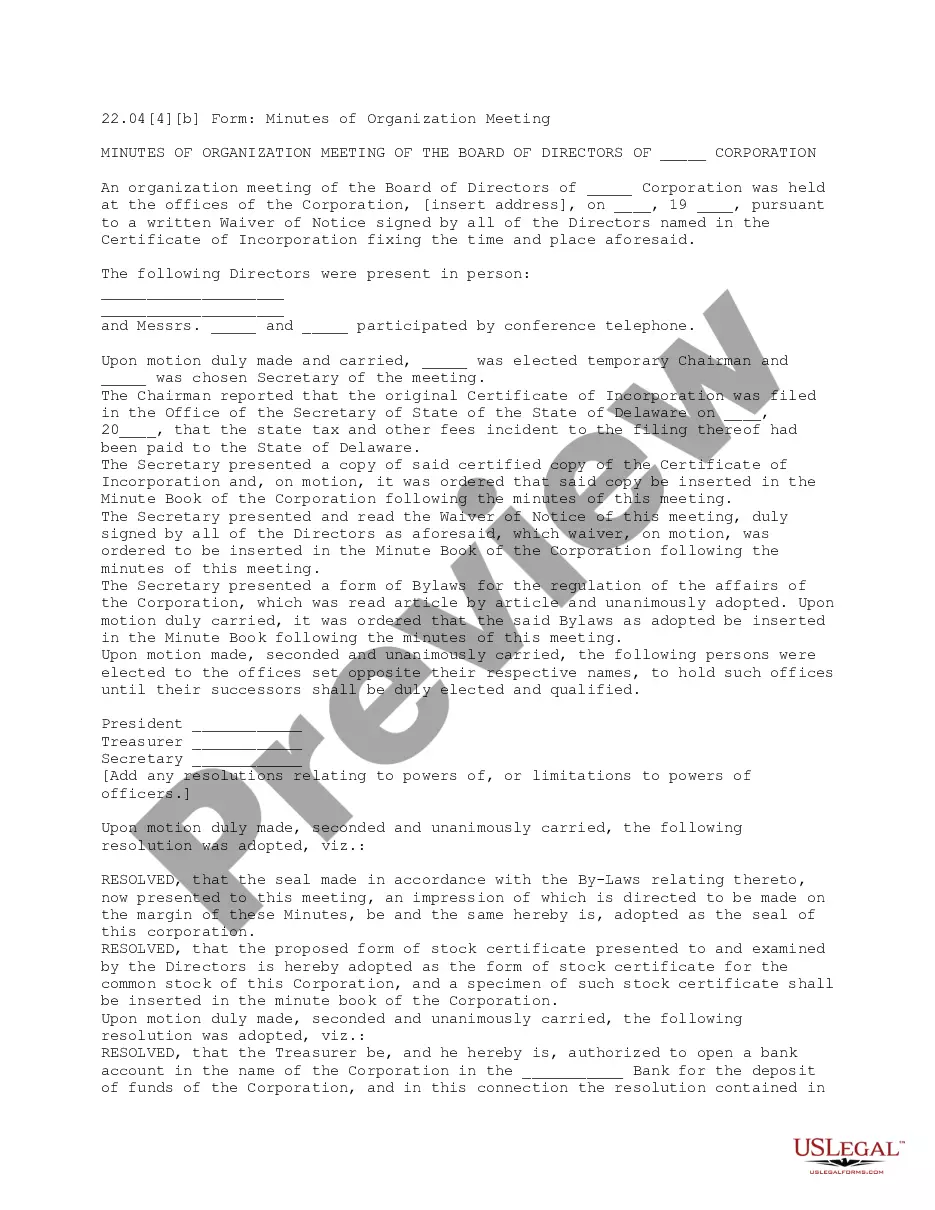

The first meeting of the sole director ratifies the actions of the incorporator, appoints the officers, gives authority to open a bank account, and allows for any other initial director tasks needed. Meeting minutes ensure that all these actions are documented in the corporate record.

Hear this out loud PauseMeeting minutes should include meeting specifics such as the date and time when the meeting begins, the place, the names and roles of attendees voting members, and important background information, or context. On the other hand, it's crucial to avoid personal opinions and prejudices.

Decision-making by directors Decisions are usually taken either by passing resolutions at a board meeting or by passing a written resolution. Although a sole director may be able to hold a board meeting, in practice, a sole director would usually make decisions by passing written resolutions.

What should board of directors first meeting minutes include? Your corporation's first directors meeting typically focuses on initial organizational tasks, including electing officers, setting their salaries, resolving to open a bank account, and ratifying bylaws and actions of the incorporators.

These are the essential items to include in your meeting minutes: Date. Time. Location. Participants. Topics discussed. Motions. Voting outcomes. Next meeting date and place.

How to write meeting minutes reports Make an outline. Prior to the meeting, create an outline by picking or designing a template. ... Include factual information. ... Write down the purpose. ... Record decisions made. ... Add details for the next meeting. ... Be concise. ... Consider recording. ... Edit and proofread.