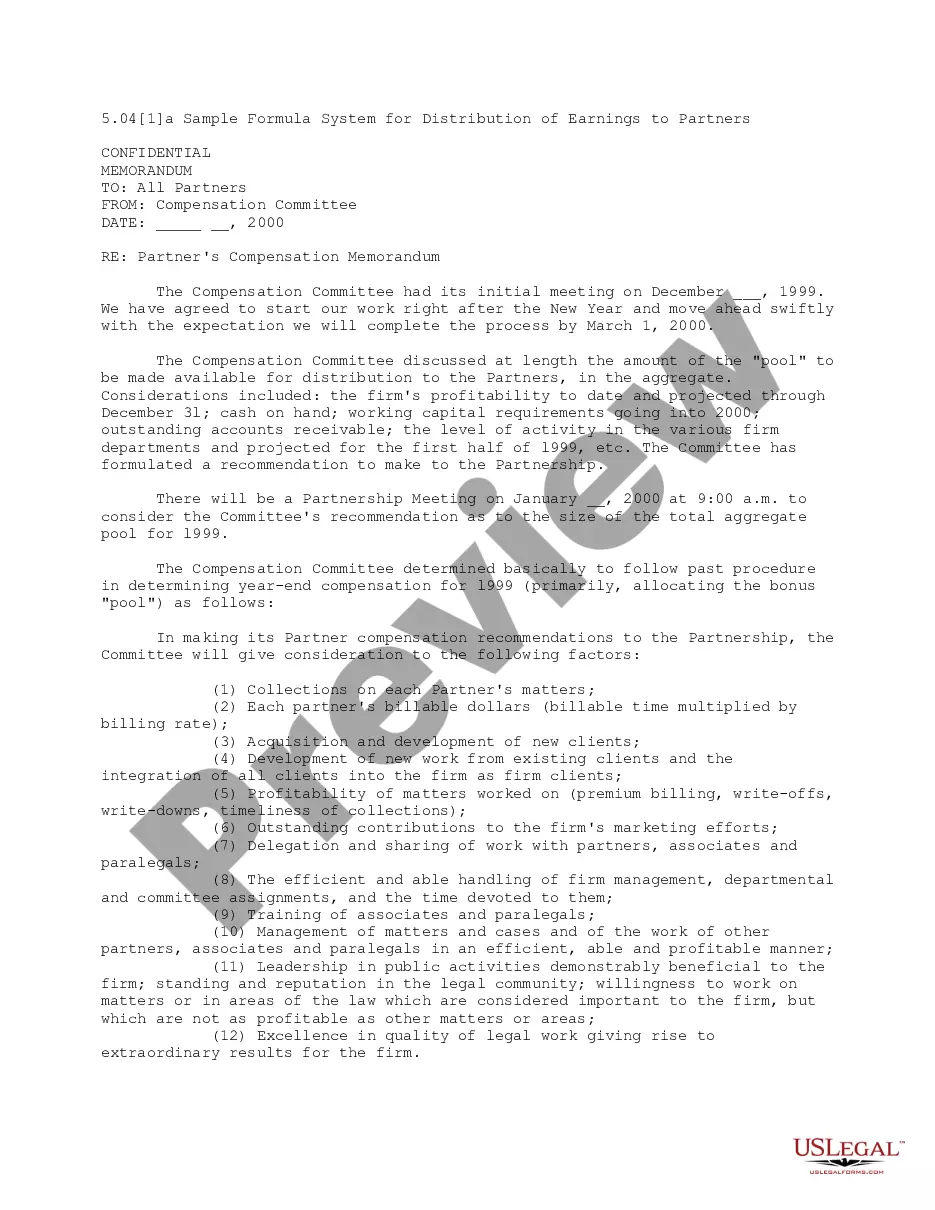

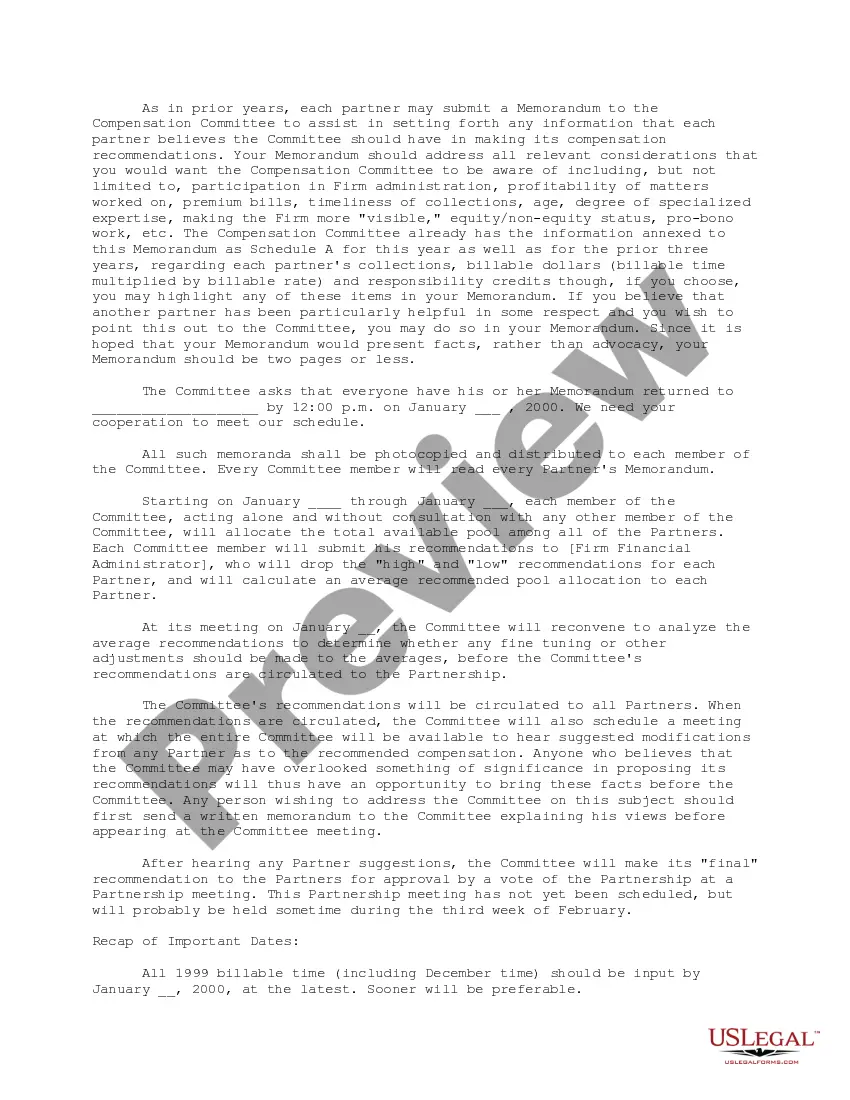

This Formula System for Distribution of Earnings to Partners provides a list of provisions to conside when making partner distribution recommendations. Some of the factors to consider are: Collections on each partner's matters, acquisition and development of new clients, profitablity of matters worked on, training of associates and paralegals, contributions to the firm's marketing practices, and others.

The Iowa Formula System for Distribution of Earnings to Partners is a method commonly utilized in partnership agreements to determine how profits are allocated among partners. This formula provides a structured approach to distributing earnings based on specific criteria agreed upon by partners. The Iowa Formula System is based on three vital components: the liquidation value, the partner's capital account, and the partner's fixed percentage. These factors play a crucial role in determining each partner's share of the profits. The liquidation value represents the amount that each partner would receive if the partnership were to be dissolved and all assets were sold. This value is typically determined by assessing the fair market value of the partnership's assets at the time of dissolution. The partner's capital account determines the proportionate share of the partner's capital investment in relation to the total capital invested by all partners. This account reflects each partner's contributions to the partnership, including initial investments and additional capital injections over time. Partnerships using the Iowa Formula System allocate earnings based on the fixed percentage assigned to each partner. This percentage is typically outlined in the partnership agreement and represents the partner's entitlement to a portion of the partnership's profits. When calculating the distribution of earnings, the Iowa Formula System follows a specific formula: (Partner's Capital Account ÷ Total Capital Accounts) × Fixed Percentage. This calculation ensures that each partner receives a fair share of the profits based on their capital investment and fixed percentage entitlement. Different types of Iowa Formula Systems for Distribution of Earnings to Partners may exist, depending on the specific needs and preferences of the partners involved. Variations could include adjustments for a partner's level of involvement in the partnership's day-to-day operations, special provisions for certain partners, or predetermined allocation percentages within specific ranges. In conclusion, the Iowa Formula System for Distribution of Earnings to Partners offers a structured approach to profit allocation in partnerships. By considering the liquidation value, partner's capital account, and fixed percentage, this formula ensures fair distribution of earnings among partners. The flexibility of this system allows for customization based on the unique characteristics and requirements of each partnership.