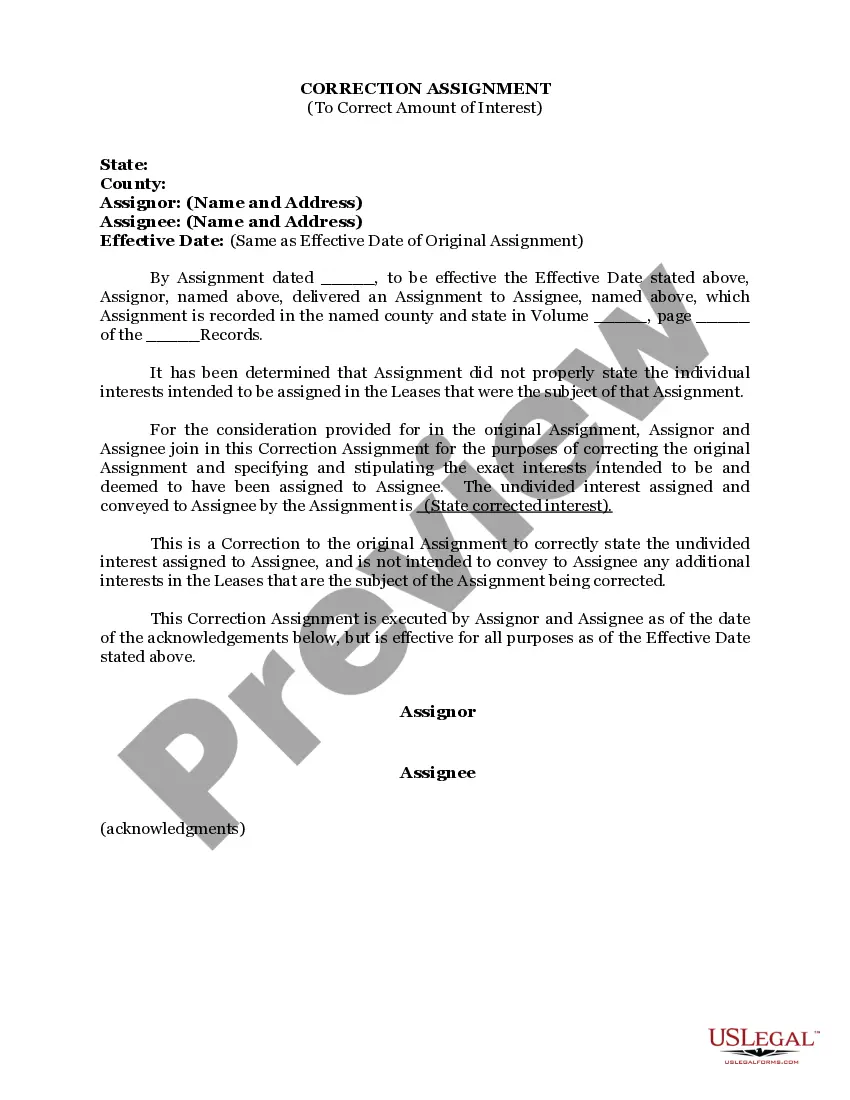

Iowa Correction Assignment to Correct Amount of Interest: Understanding the Purpose and Types The Iowa Correction Assignment to Correct Amount of Interest plays a vital role in maintaining accurate financial records and ensuring fair business practices within the state. This process is designed to rectify any errors or discrepancies related to the calculation or reporting of interest amounts in various financial transactions. Keywords: Iowa, Correction Assignment, Correct Amount of Interest, financial records, errors, discrepancies, calculation, reporting, interest amounts, financial transactions. As with any correction assignment, ensuring accurate interest calculations is crucial to prevent financial disputes and maintain trust among parties involved. The state of Iowa acknowledges this importance and has established specific procedures to address such issues effectively. Types of Iowa Correction Assignment to Correct Amount of Interest: 1. Correction Assignment for Miscalculated Interest: This type of correction assignment is necessary when there has been an error in the calculation of interest. It may occur due to incorrect data entry, faulty formulas, or other human or technical errors. The assigned party must identify the mistake, recalculate the accurate interest amount, and update the financial records accordingly. 2. Correction Assignment for Underreported or Overreported Interest: In some cases, the issue might not lie in the interest calculation itself, but rather in its reporting. Parties involved might unintentionally underreport or overreport the interest, leading to inaccurate financial statements. The Iowa Correction Assignment aims to rectify such errors by adjusting the reported interest amount to reflect the correct value as per the respective financial transaction. 3. Correction Assignment for Interest Rate Changes: Interest rates are subject to change based on various factors like market conditions, contractual agreements, or legal requirements. However, if these changes are not appropriately implemented or communicated, it can lead to discrepancies in the reported interest amounts. In such cases, the assigned party will correct the interest amount by applying the correct interest rate, ensuring compliance and accuracy in financial records. 4. Correction Assignment for Interest Recapitalization: Interest recapitalization refers to the process of adjusting interest amounts based on changes in principal balances or other factors specified in the financial agreements. Should any mistakes occur during this process, the Iowa Correction Assignment will be utilized to rectify them promptly. In conclusion, the Iowa Correction Assignment to Correct Amount of Interest is an essential mechanism to ensure accuracy and fairness in financial transactions involving interest calculations. By addressing miscalculations, underreported or overreported interest, interest rate changes, and interest recapitalization errors, this assignment plays a crucial role in maintaining trust and financial integrity in the state of Iowa.

Iowa Correction Assignment to Correct Amount of Interest

Description

How to fill out Iowa Correction Assignment To Correct Amount Of Interest?

Are you currently within a placement that you need to have papers for either organization or personal reasons just about every day? There are tons of legitimate document templates available on the Internet, but discovering types you can rely is not simple. US Legal Forms provides a huge number of develop templates, like the Iowa Correction Assignment to Correct Amount of Interest, that are created to satisfy federal and state specifications.

In case you are presently familiar with US Legal Forms website and also have an account, basically log in. Following that, you can obtain the Iowa Correction Assignment to Correct Amount of Interest template.

Should you not have an accounts and want to start using US Legal Forms, follow these steps:

- Discover the develop you require and make sure it is to the appropriate city/county.

- Utilize the Review option to analyze the shape.

- See the information to ensure that you have selected the right develop.

- In the event the develop is not what you`re seeking, use the Look for discipline to discover the develop that fits your needs and specifications.

- Whenever you discover the appropriate develop, click on Acquire now.

- Pick the prices prepare you want, fill out the specified information and facts to create your account, and buy your order using your PayPal or bank card.

- Select a convenient document file format and obtain your backup.

Locate every one of the document templates you possess purchased in the My Forms menu. You can aquire a additional backup of Iowa Correction Assignment to Correct Amount of Interest at any time, if required. Just go through the needed develop to obtain or print the document template.

Use US Legal Forms, the most comprehensive selection of legitimate varieties, to save time and prevent errors. The services provides professionally made legitimate document templates which can be used for a selection of reasons. Make an account on US Legal Forms and commence creating your lifestyle a little easier.