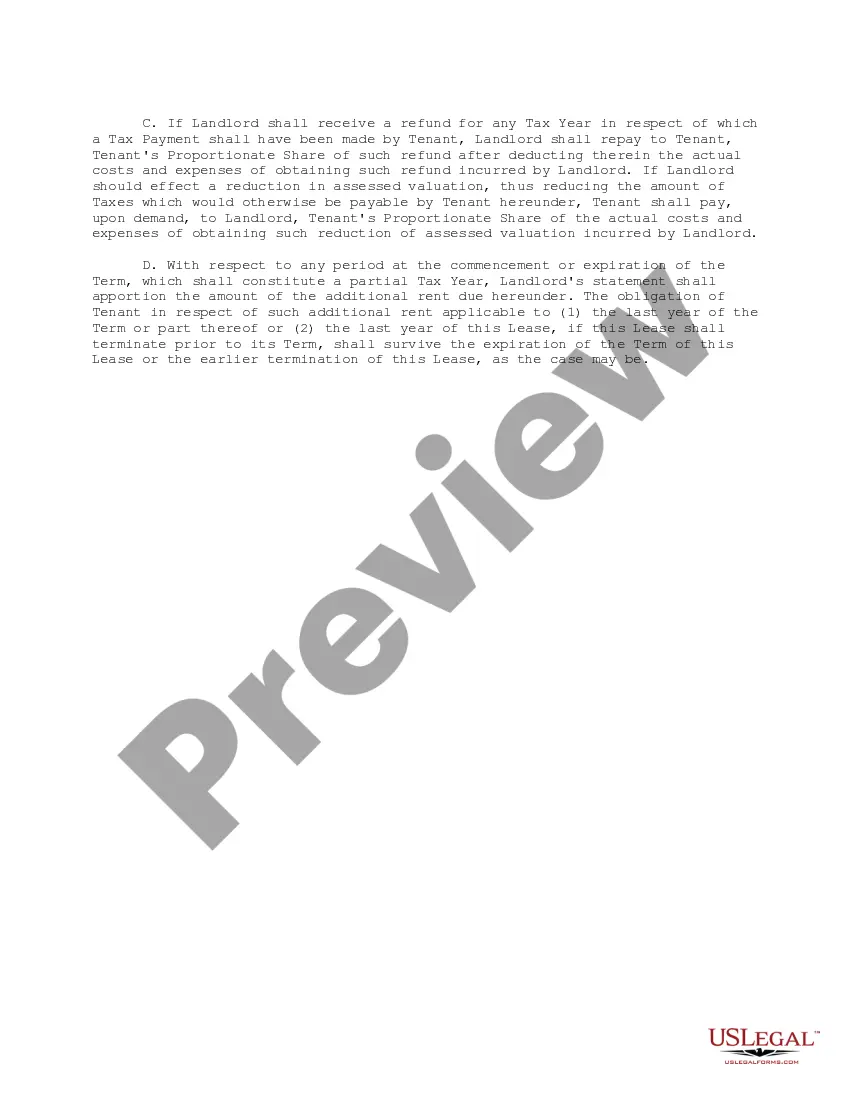

This form is a clause regarding additional rent element of an office lease providing for tax increases. The tax increases pertain to assessments and special assessments levied, assessed or imposed upon the building and/or the land under, including any land(s) dedicated to the use of, the building, by any governmental bodies or authorities.

The Iowa Tax Increase Clause, also known as the Taxpayer Trust Fund Amendment, is a constitutional provision in the state of Iowa that aims to restrict tax increases and protect taxpayer rights. Enacted in 1992, this clause places constraints on the government's ability to increase taxes without obtaining majority support from Iowa citizens. Under the Iowa Tax Increase Clause, any legislation that proposes a tax increase must be approved by either a two-thirds majority vote of both the Iowa House of Representatives and Senate or by a majority vote in a statewide referendum. This requirement ensures that tax increases are not implemented without the consent of the taxpayers themselves. The purpose of the Iowa Tax Increase Clause is to promote fiscal responsibility and transparency in government by allowing citizens to directly participate in decisions regarding tax hikes. By imposing these restrictions, the clause aims to protect taxpayers from excessive tax burdens and to encourage lawmakers to carefully consider the impact of tax increases on the economy and individual residents. It is important to note that there are no distinct "types" of the Iowa Tax Increase Clause. However, its provisions apply across different types of taxes, including income tax, sales tax, property tax, and other state-imposed levies. Any proposed tax increase, regardless of its nature, must adhere to the requirements set forth by the Tax Increase Clause. In summary, the Iowa Tax Increase Clause is a constitutional provision that ensures tax increases are subject to strict approval processes, requiring either super majority support from legislators or approval through a statewide referendum. Its aim is to safeguard taxpayers' rights and promote responsible fiscal governance in Iowa.The Iowa Tax Increase Clause, also known as the Taxpayer Trust Fund Amendment, is a constitutional provision in the state of Iowa that aims to restrict tax increases and protect taxpayer rights. Enacted in 1992, this clause places constraints on the government's ability to increase taxes without obtaining majority support from Iowa citizens. Under the Iowa Tax Increase Clause, any legislation that proposes a tax increase must be approved by either a two-thirds majority vote of both the Iowa House of Representatives and Senate or by a majority vote in a statewide referendum. This requirement ensures that tax increases are not implemented without the consent of the taxpayers themselves. The purpose of the Iowa Tax Increase Clause is to promote fiscal responsibility and transparency in government by allowing citizens to directly participate in decisions regarding tax hikes. By imposing these restrictions, the clause aims to protect taxpayers from excessive tax burdens and to encourage lawmakers to carefully consider the impact of tax increases on the economy and individual residents. It is important to note that there are no distinct "types" of the Iowa Tax Increase Clause. However, its provisions apply across different types of taxes, including income tax, sales tax, property tax, and other state-imposed levies. Any proposed tax increase, regardless of its nature, must adhere to the requirements set forth by the Tax Increase Clause. In summary, the Iowa Tax Increase Clause is a constitutional provision that ensures tax increases are subject to strict approval processes, requiring either super majority support from legislators or approval through a statewide referendum. Its aim is to safeguard taxpayers' rights and promote responsible fiscal governance in Iowa.