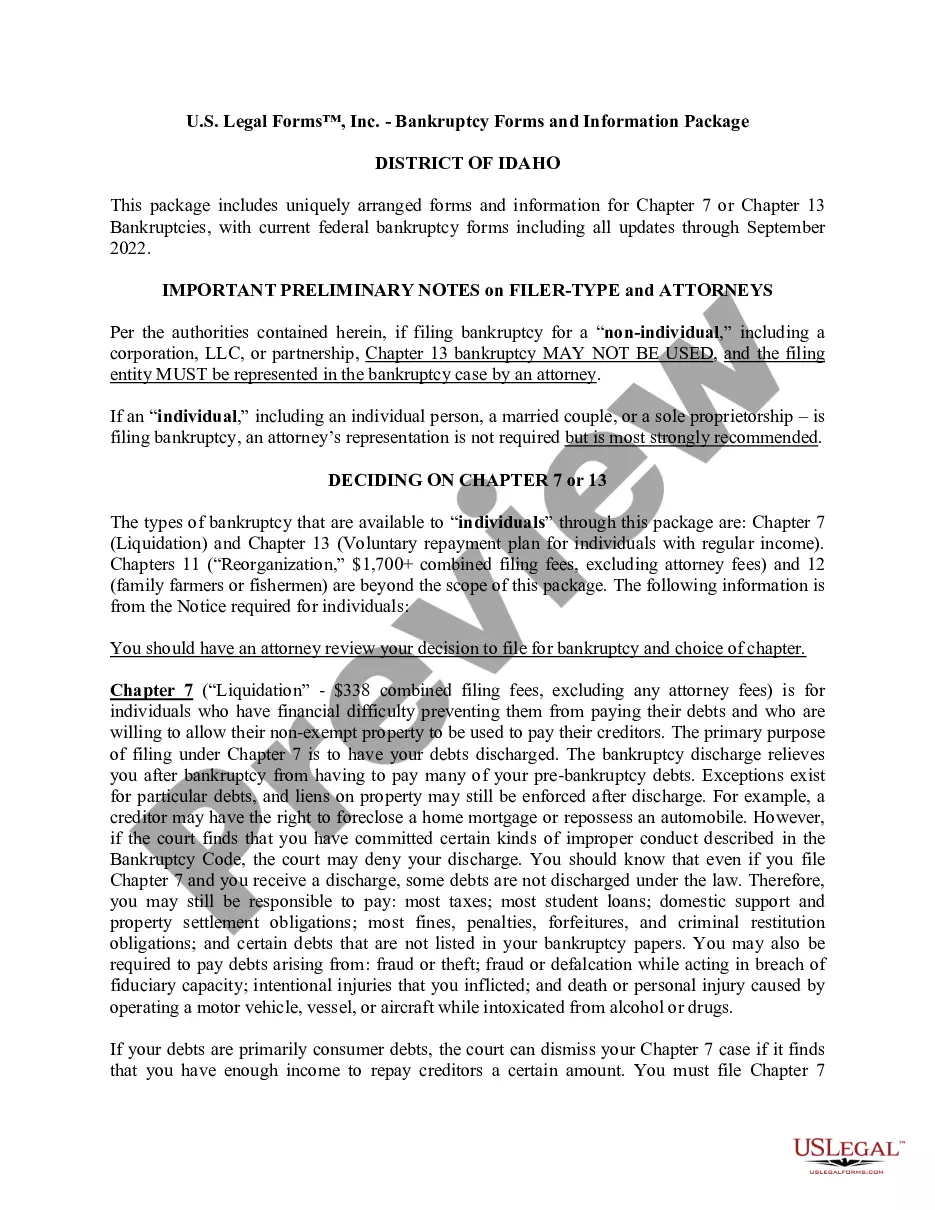

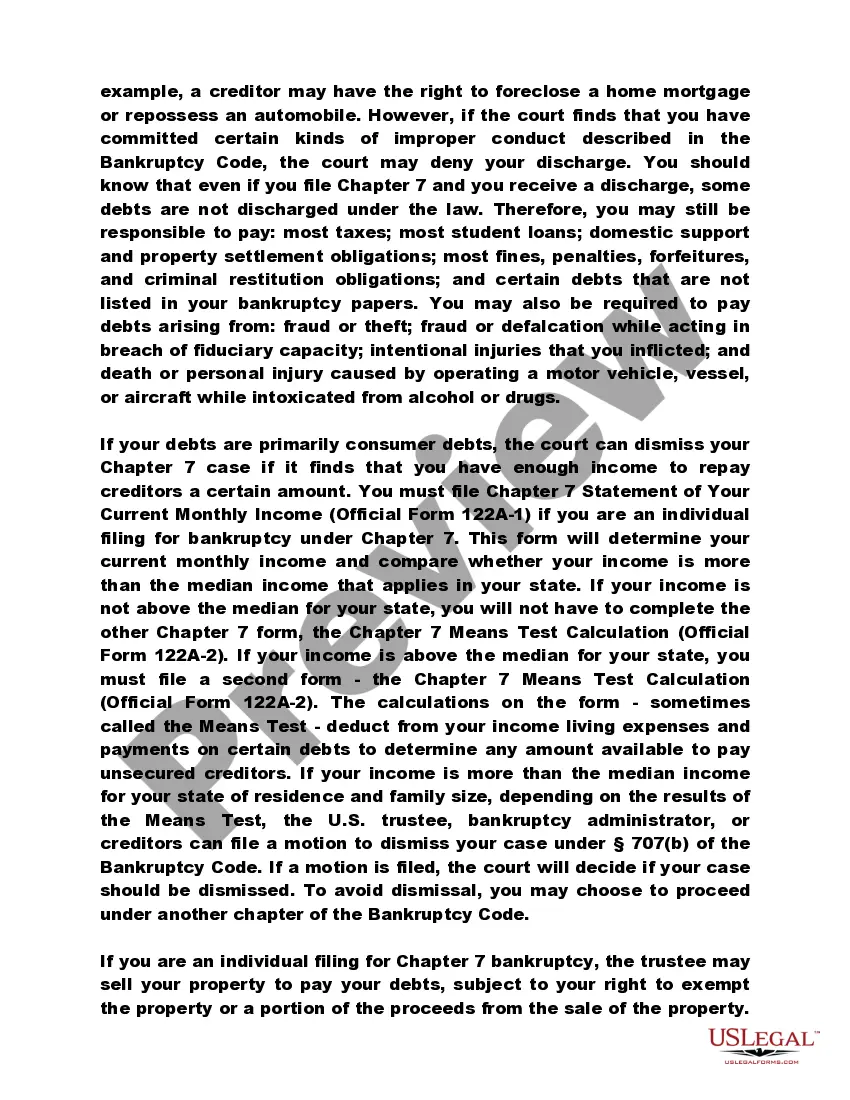

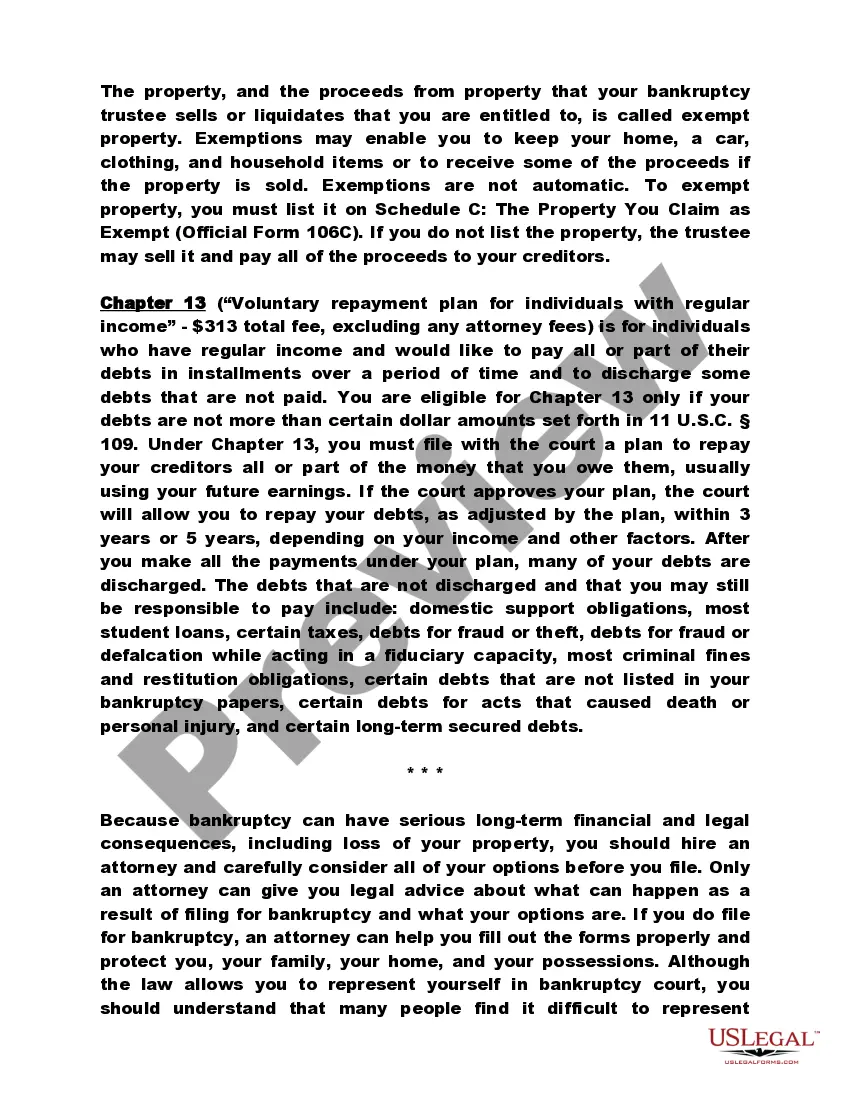

Uniquely packaged forms and information for Chapter 7 or 13 bankruptcies, including detailed instructions and other resources. Click and view the Free Preview for the latest revision dates and a complete overview of contents.

Idaho Bankruptcy Guide and Forms Package for Chapters 7 or 13

Instant download

Description Chapter 7 Bankruptcy Idaho

Free preview Example Of Chapter 13 Payment Plan

How to fill out Idaho Bankruptcy Guide And Forms Package For Chapters 7 Or 13?

In search of Idaho Bankruptcy Guide and Forms Package for Chapters 7 or 13 forms and filling out them can be quite a challenge. To save lots of time, costs and energy, use US Legal Forms and find the right template specially for your state within a couple of clicks. Our legal professionals draw up all documents, so you simply need to fill them out. It is really that easy.

Log in to your account and come back to the form's page and save the sample. All your downloaded examples are saved in My Forms and are accessible all the time for further use later. If you haven’t subscribed yet, you should sign up.

Take a look at our thorough guidelines on how to get the Idaho Bankruptcy Guide and Forms Package for Chapters 7 or 13 sample in a few minutes:

- To get an entitled example, check its validity for your state.

- Check out the example using the Preview option (if it’s offered).

- If there's a description, read it to know the specifics.

- Click on Buy Now button if you found what you're searching for.

- Pick your plan on the pricing page and create an account.

- Select you want to pay out by way of a card or by PayPal.

- Save the form in the favored file format.

Now you can print out the Idaho Bankruptcy Guide and Forms Package for Chapters 7 or 13 template or fill it out making use of any web-based editor. No need to worry about making typos because your template may be employed and sent, and published as many times as you wish. Try out US Legal Forms and access to over 85,000 state-specific legal and tax files.

Form popularity

FAQ

In many cases, Chapter 7 bankruptcy is a better fit than Chapter 13 bankruptcy. For instance, Chapter 7 is quicker, many filers can keep all or most of their property, and filers don't pay creditors through a three- to five-year Chapter 13 repayment plan.

A chapter 13 bankruptcy is also called a wage earner's plan. It enables individuals with regular income to develop a plan to repay all or part of their debts. Under this chapter, debtors propose a repayment plan to make installments to creditors over three to five years.

With Chapter 7, those types of debts are wiped out with your filing's court approval, which can take a few months. Under Chapter 13, you need to continue making payments on those balances throughout your court-instructed repayment plan; afterwards, the unsecured debts may be discharged.

Chapter 13 Is Likely to Worsen Your Finances When your Chapter 13 case is dismissed, you are often in a far worse financial position. That's because the interest on your unpaid debts has continued to mount as you've struggled to make payments. And once you're out of bankruptcy protection, you have more debt than ever.

A Chapter 13 bankruptcy involves repaying some or all of your debt over a three- to- five-year period, while a Chapter 7 bankruptcy involves wiping out most of your debts without paying them back.In that way, a Chapter 13 may be better for your credit than a Chapter 7.

In many cases, Chapter 7 bankruptcy is a better fit than Chapter 13 bankruptcy. For instance, Chapter 7 is quicker, many filers can keep all or most of their property, and filers don't pay creditors through a three- to five-year Chapter 13 repayment plan.

Chapter 11 bankruptcy works well for businesses and individuals whose debt exceeds the Chapter 13 bankruptcy limits. In most cases, Chapter 13 is the better choice for qualifying individuals and sole proprietors.

Generally, a debtor can convert a bankruptcy case one time with court approval.To convert a Chapter 7 case to Chapter 13, the debtor must meet the eligibility requirements for filing a Chapter 13 case. That includes having enough income to repay creditors under a payment plan.

Key Takeaways. Chapter 7 bankruptcy doesn't require a repayment plan but does require you to liquidate or sell nonexempt assets to pay back creditors.Chapter 13 bankruptcy eliminates qualified debt through a repayment plan over a three- or five-year period.