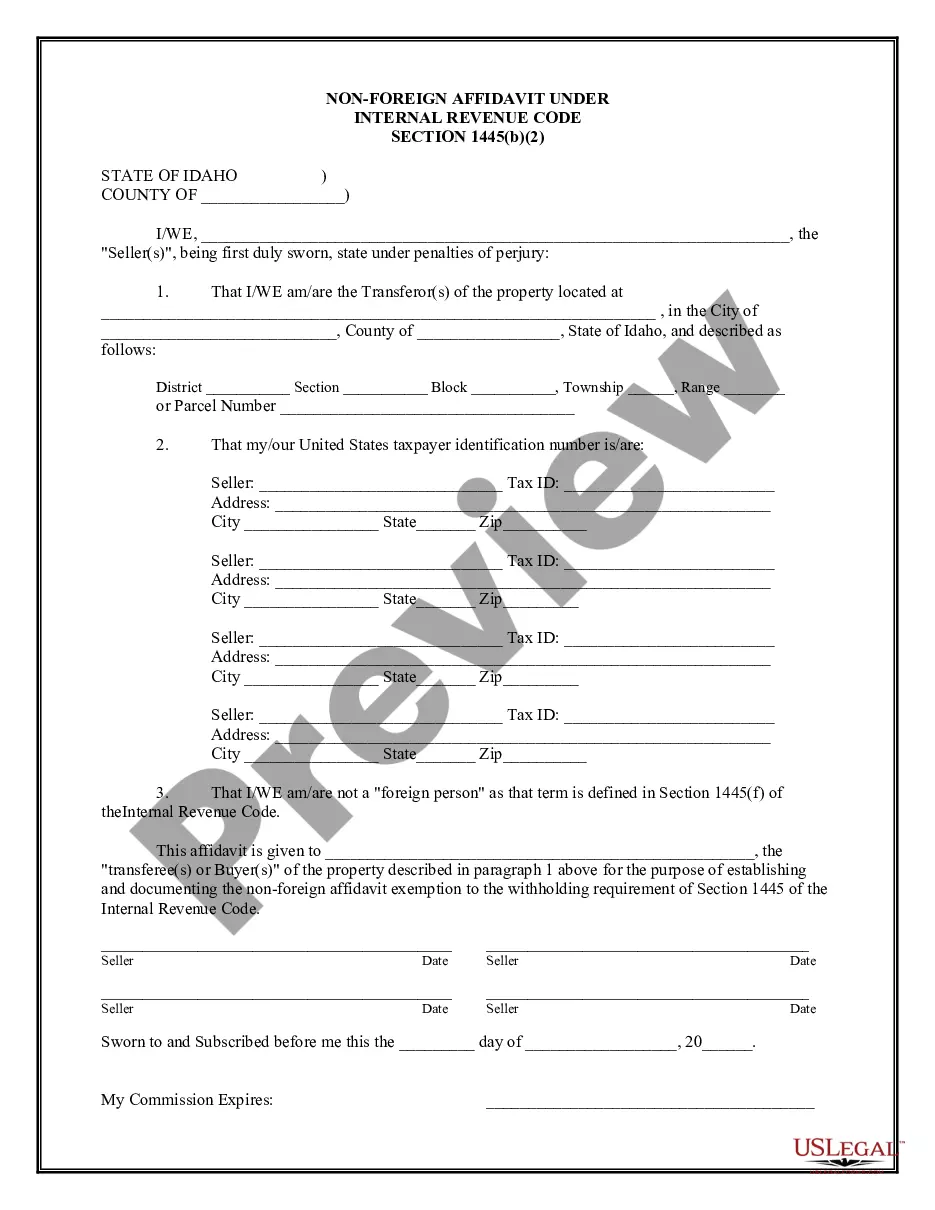

This Non-Foreign Affdavit Under Internal Revenue Code 1445 is for a seller of real property to sign stating that he or she is not a foreign person as defined by the Internal Revenue Code Section 26 USC 1445. This document must be signed and notarized.

Idaho Non-Foreign Affidavit Under IRC 1445

Instant download

Description

Free preview

How to fill out Idaho Non-Foreign Affidavit Under IRC 1445?

Searching for Idaho Non-Foreign Affidavit Under IRC 1445 templates and completing them could be a problem. To save time, costs and effort, use US Legal Forms and find the correct sample specifically for your state within a couple of clicks. Our lawyers draw up each and every document, so you just have to fill them out. It truly is that easy.

Log in to your account and return to the form's page and save the sample. All your saved templates are saved in My Forms and therefore are accessible always for further use later. If you haven’t subscribed yet, you need to register.

Look at our comprehensive instructions on how to get your Idaho Non-Foreign Affidavit Under IRC 1445 sample in a couple of minutes:

- To get an eligible sample, check its validity for your state.

- Look at the sample utilizing the Preview option (if it’s accessible).

- If there's a description, go through it to learn the details.

- Click Buy Now if you found what you're looking for.

- Select your plan on the pricing page and create your account.

- Choose you want to pay by a credit card or by PayPal.

- Download the form in the favored file format.

You can print out the Idaho Non-Foreign Affidavit Under IRC 1445 template or fill it out making use of any web-based editor. Don’t concern yourself with making typos because your template may be used and sent, and printed out as often as you wish. Try out US Legal Forms and access to above 85,000 state-specific legal and tax documents.

Form popularity

FAQ

The Foreign Investment in Real Property Transfer Act (FIRPTA) requires any buyer of a U.S. real property interest to withhold ten percent of the amount realized by a foreign seller. 26 USC § 1445(a).

Persons purchasing U.S. real property interests (transferees) from foreign persons, certain purchasers' agents, and settlement officers are required to withhold 15% (10% for dispositions before February 17, 2016) of the amount realized on the disposition (special rules for foreign corporations).

A foreign person includes a nonresident alien individual, foreign corporation, foreign partnership, foreign trust, foreign estate, and any other person that is not a U.S. person. It also includes a foreign branch of a U.S. financial institution if the foreign branch is a qualified intermediary.

What Is a Certification of Non-Foreign Status? With a Certification of Non-Foreign Status, the seller of real estate is certifying under penalty of perjury, that the seller is not foreign. Therefore, the seller and the transaction will not have the withholding requirements.

The disposition of a U.S. real property interest by a foreign person (the transferor) is subject to the Foreign Investment in Real Property Tax Act of 1980 (FIRPTA) income tax withholding. FIRPTA authorized the United States to tax foreign persons on dispositions of U.S. real property interests.

This document, included in the seller's opening package, requests that the seller swears under penalty of perjury that they are not a non-resident alien for purposes of United States income taxation. A Seller unable to complete this affidavit may be subject to withholding up to 15%.

FIRPTA Exemptions The sales price is $300,000 or less, and. The buyer signs affidavit at or before closing stating they intend to use property for personal purposes for at least 50% of time property occupied for the each of the first two 12 month periods immediately after closing.

You or a member of your family must have definite plans to reside at the property for at least 50% of the number of days the property is used by any person during each of the first two 12-month periods following the date of transfer.

The disposition of a U.S. real property interest by a foreign person (the transferor) is subject to income tax withholding (IRC section 1445). The transferee is the withholding agent.If the transferor is a foreign person and you fail to withhold, you may be held liable for the tax.