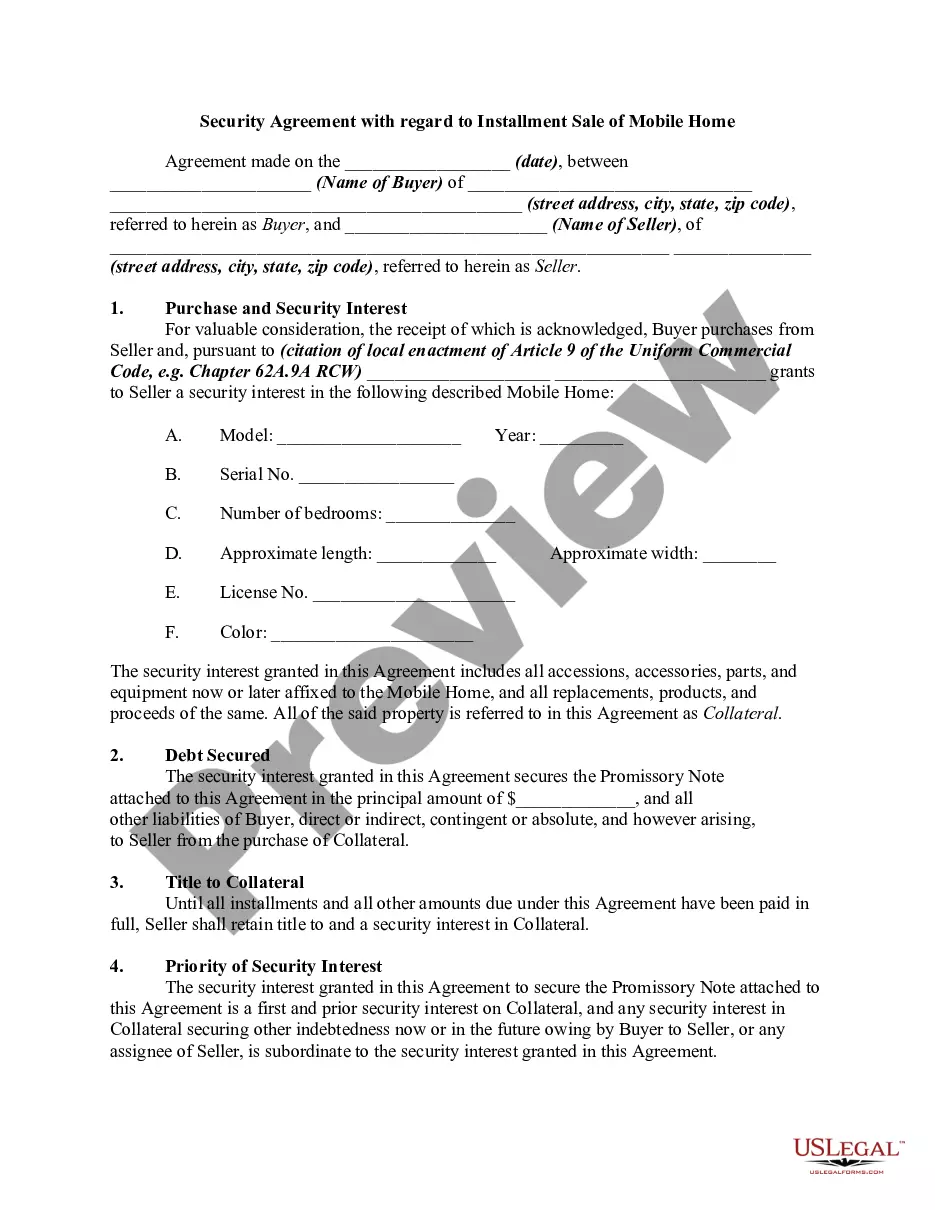

Idaho Chattel Mortgage on Mobile Home

Description

How to fill out Chattel Mortgage On Mobile Home?

Are you presently in a situation where you require documents for occasional business or personal purposes nearly every day? There are numerous legal document templates available online, but finding ones you can rely on is not easy. US Legal Forms offers a vast collection of document templates, such as the Idaho Chattel Mortgage on Mobile Home, that are drafted to comply with federal and state regulations.

If you are currently familiar with the US Legal Forms website and have an account, simply Log In. After that, you can download the Idaho Chattel Mortgage on Mobile Home template.

If you do not have an account and wish to start using US Legal Forms, follow these instructions: Find the document you need and ensure it is for your specific city/state. Use the Review button to inspect the form. Read the description to ensure you have selected the correct document. If the form is not what you are looking for, use the Search field to find the document that meets your criteria and needs. Once you find the right document, click Purchase now. Choose the pricing plan you want, complete the required information to create your account, and make a purchase using your PayPal or credit card. Select a convenient document format and download your copy. Access all the document templates you have purchased in the My documents section. You can obtain another copy of the Idaho Chattel Mortgage on Mobile Home anytime if needed. Simply click on the necessary document to download or print the template.

- Use US Legal Forms, the most comprehensive collection of legal documents, to save time and avoid mistakes.

- The service provides professionally crafted legal document templates that can be utilized for a variety of purposes.

- Create an account on US Legal Forms and start making your life a bit easier.

Form popularity

FAQ

In Idaho, seniors may qualify for property tax reduction programs that can lower or eliminate property taxes based on age and income. Generally, seniors who are 65 or older can apply for these benefits. If you own a mobile home and are considering your tax situation, knowing about an Idaho Chattel Mortgage on Mobile Home can provide additional financial strategies.

Items not classified as real property include movable personal belongings, vehicles, and mobile homes that are not permanently affixed to land. These items can be sold or transferred without the complexities associated with real property. If you are financing a mobile home and need clarity on its classification, an Idaho Chattel Mortgage on Mobile Home might be the right option to explore.

Real property in Idaho includes land and anything permanently attached to it, such as buildings or structures. This definition distinguishes real property from personal property, which can include movable items. If you are looking to understand how an Idaho Chattel Mortgage on Mobile Home fits into this definition, it is essential to consider how your home is classified.

A manufactured home is classified as personal property unless it is permanently attached to land. In this case, it can be considered real property. If you are unsure about the classification of your manufactured home, understanding the implications of an Idaho Chattel Mortgage on Mobile Home can help you make informed decisions.

In Idaho, a mobile home is generally not considered real property unless it is affixed to land and the owner has taken steps to convert it. This conversion involves recording a declaration of intent to convert the mobile home into real property. If you are exploring financing options, an Idaho Chattel Mortgage on Mobile Home may be a suitable choice for your needs.

A chattel mortgage typically covers movable personal property, such as manufactured homes, vehicles, and equipment. Specifically, an Idaho Chattel Mortgage on Mobile Home applies to homes that are not attached to the land they sit on. This means that you can use the mortgage to finance your mobile home while retaining the freedom to relocate it. For detailed guidance on securing a chattel mortgage, consider leveraging the resources available through US Legal Forms.

Yes, manufactured homes are considered chattel when they are not permanently affixed to the land. This classification means that they can be financed using an Idaho Chattel Mortgage on Mobile Home. Chattel mortgages allow homeowners to secure loans against these movable properties, providing flexibility and options for financing. If you’re considering a manufactured home, understanding its status as chattel can help you make informed financial decisions.