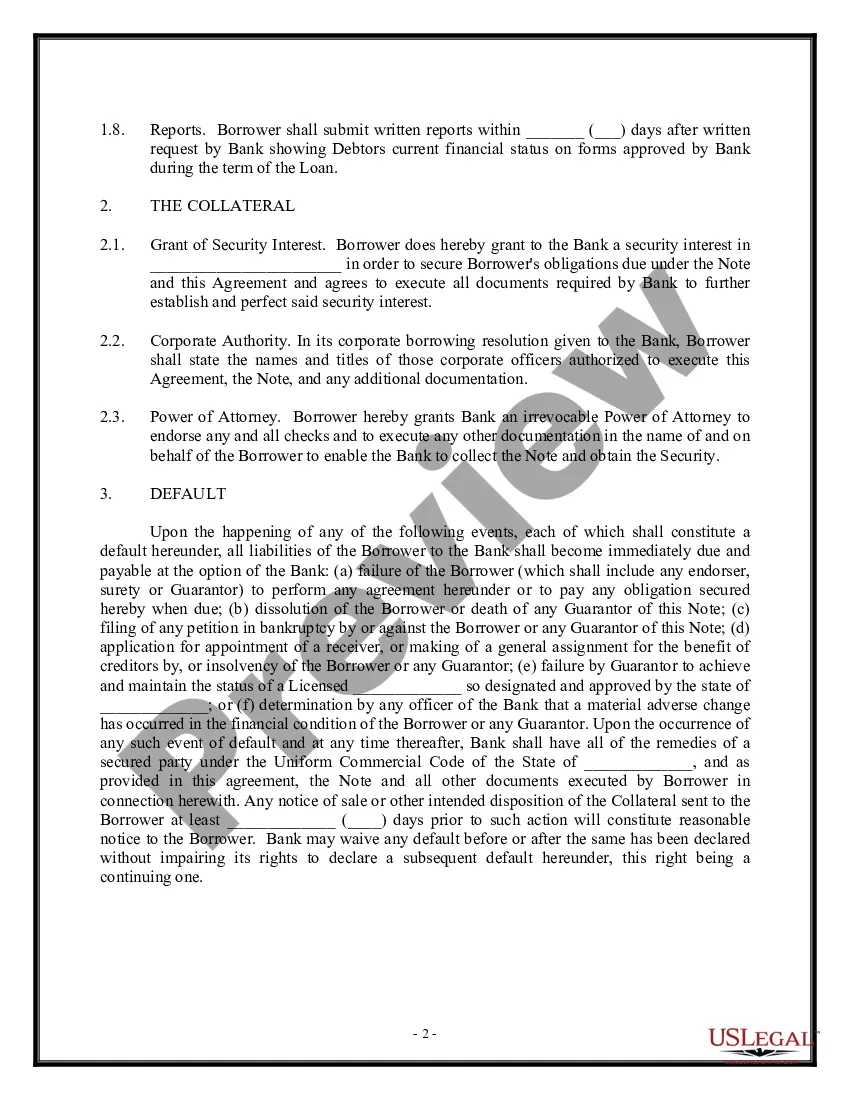

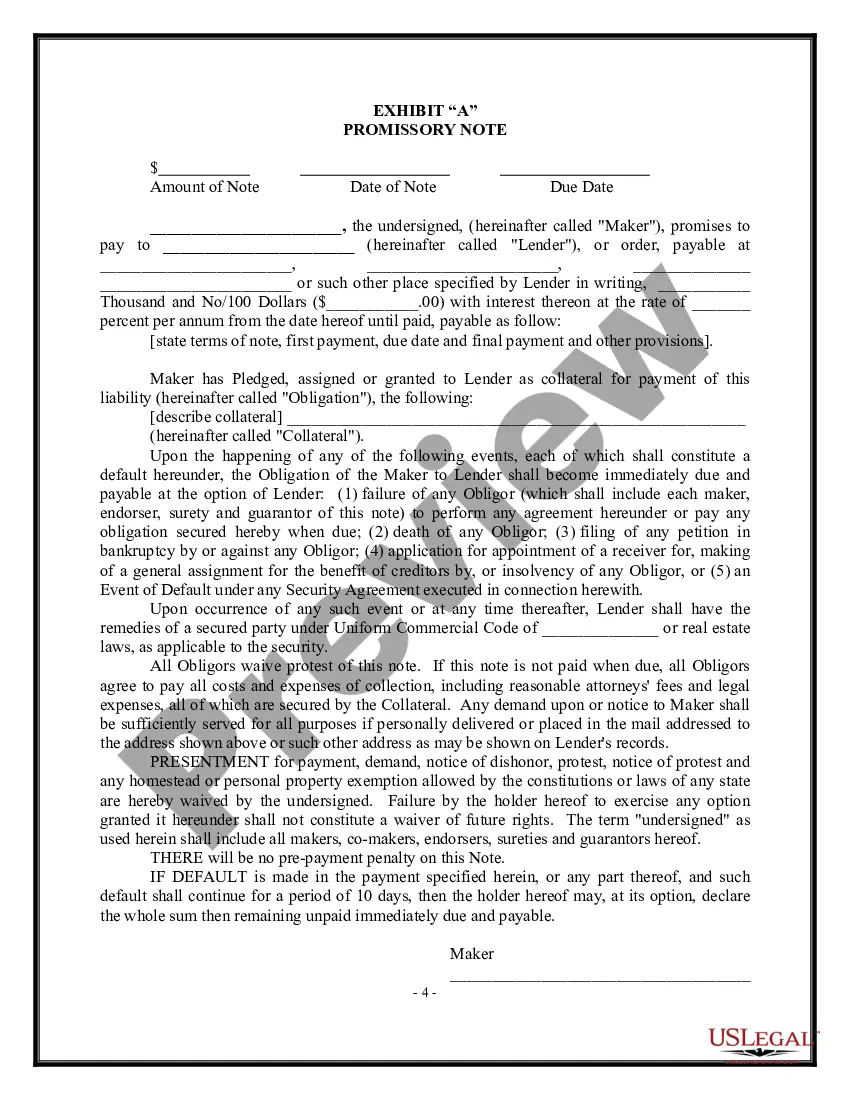

Idaho Loan Agreement — Short Form is a legally binding document that outlines the terms and conditions of a loan transaction between a lender and a borrower in the state of Idaho. This agreement is designed to provide a concise and simplified version of a loan agreement, while still ensuring that all essential elements are included. The Idaho Loan Agreement — Short Form typically includes crucial information such as the names and addresses of both parties involved, the loan amount, the repayment terms, and the interest rate. It also includes provisions regarding any collateral or security being used to secure the loan, as well as any applicable late payment penalties or default provisions. There are different types of Idaho Loan Agreement — Short Form, each tailored to specific loan arrangements. Some common variations include: 1. Personal Loan Agreement: This type of agreement is used when an individual is lending money to another individual, usually for personal reasons such as debt consolidation, home improvement, or education expenses. The agreement outlines the terms of the loan, including the repayment schedule and any additional provisions agreed upon by both parties. 2. Business Loan Agreement: This agreement is used when a business entity, such as a corporation or partnership, is lending money to another business entity. It includes specific provisions related to the business loan, such as the purpose of the loan, the repayment terms, and any applicable interest rates or fees. 3. Promissory Note: While not technically a loan agreement, a promissory note is often used in conjunction with a loan agreement and serves as a written promise to repay a specified amount of money by a certain date. It outlines the terms of repayment, including any interest or late payment fees. 4. Parent-Child Loan Agreement: This type of agreement is used when a parent is providing a loan to their child or vice versa. It ensures that both parties are protected and clarifies the terms of repayment, interest rates, and any other relevant conditions. Such agreements can be useful for larger expenses like education or buying a home. The Idaho Loan Agreement — Short Form is a valuable tool for both lenders and borrowers, as it helps ensure clarity, transparency, and legal protection for all parties involved. It is strongly recommended consulting with a legal professional or attorney when preparing or entering into a loan agreement to ensure compliance with Idaho state laws and to address any specific circumstances or needs.

Idaho Loan Agreement - Short Form

Description

How to fill out Idaho Loan Agreement - Short Form?

Choosing the right legal file design could be a battle. Obviously, there are a lot of layouts accessible on the Internet, but how can you obtain the legal form you will need? Make use of the US Legal Forms website. The support delivers a large number of layouts, such as the Idaho Loan Agreement - Short Form, which can be used for company and private requires. All the types are examined by specialists and meet up with federal and state demands.

In case you are presently signed up, log in for your profile and then click the Down load switch to have the Idaho Loan Agreement - Short Form. Utilize your profile to search throughout the legal types you might have acquired formerly. Proceed to the My Forms tab of your profile and obtain one more duplicate from the file you will need.

In case you are a new user of US Legal Forms, here are basic guidelines that you should adhere to:

- First, make sure you have selected the right form for your metropolis/state. You may examine the form using the Review switch and study the form information to ensure this is the right one for you.

- In the event the form will not meet up with your needs, make use of the Seach industry to find the proper form.

- Once you are certain that the form is proper, select the Acquire now switch to have the form.

- Choose the pricing program you want and type in the necessary information and facts. Design your profile and pay money for your order utilizing your PayPal profile or bank card.

- Pick the data file file format and download the legal file design for your device.

- Total, change and printing and signal the attained Idaho Loan Agreement - Short Form.

US Legal Forms may be the most significant collection of legal types that you can find different file layouts. Make use of the service to download professionally-made documents that adhere to status demands.