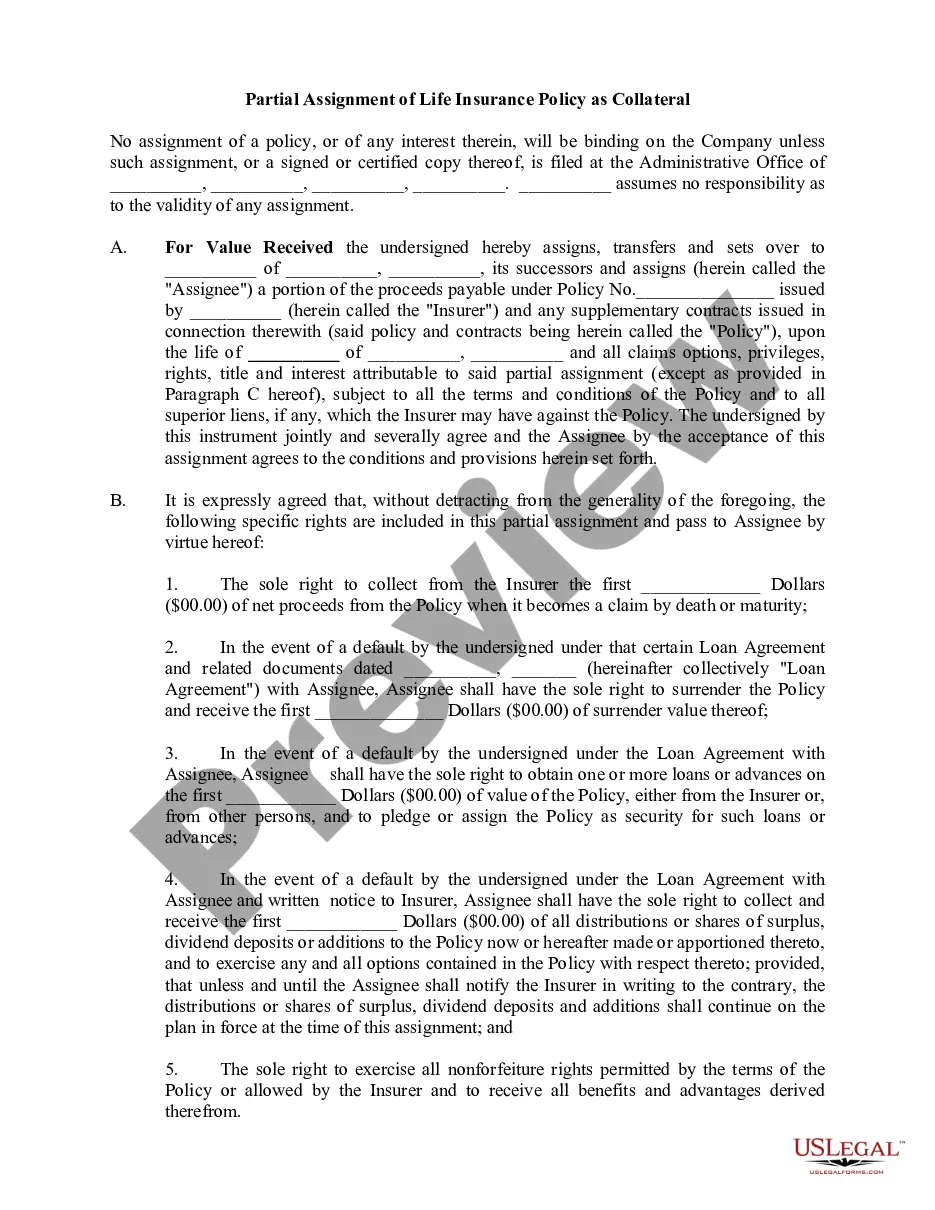

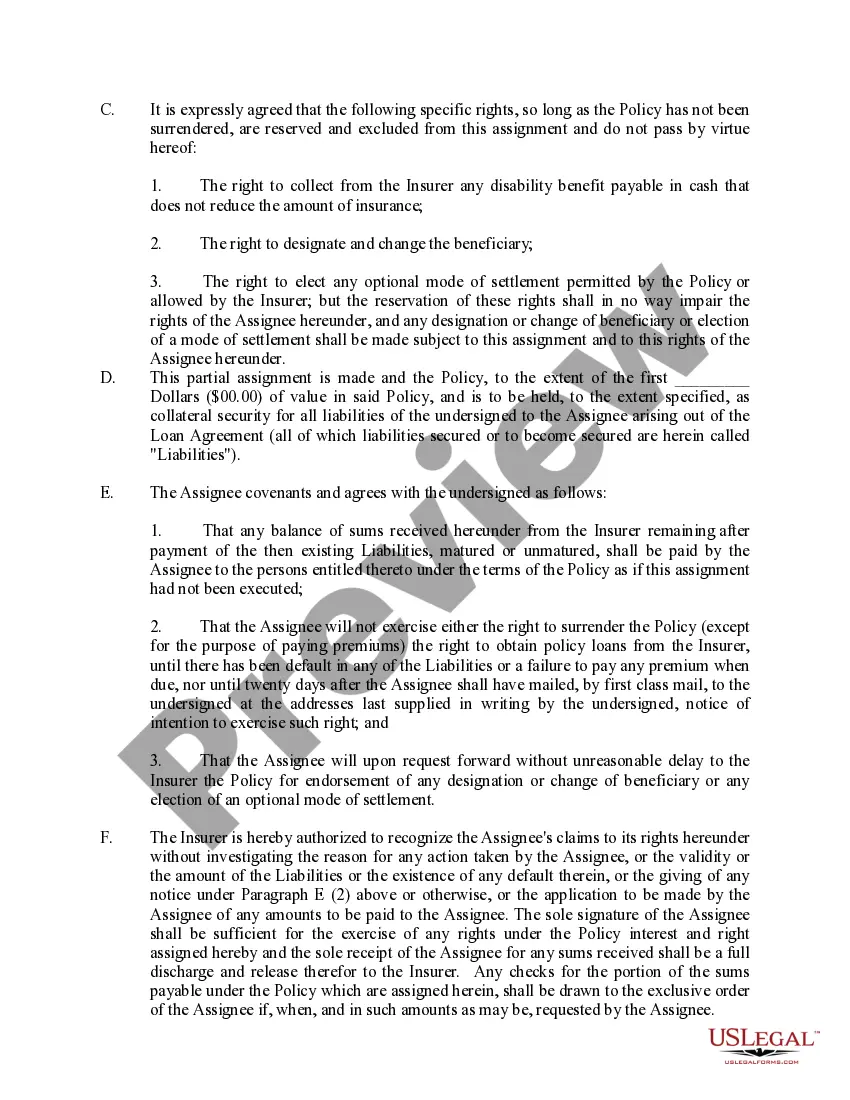

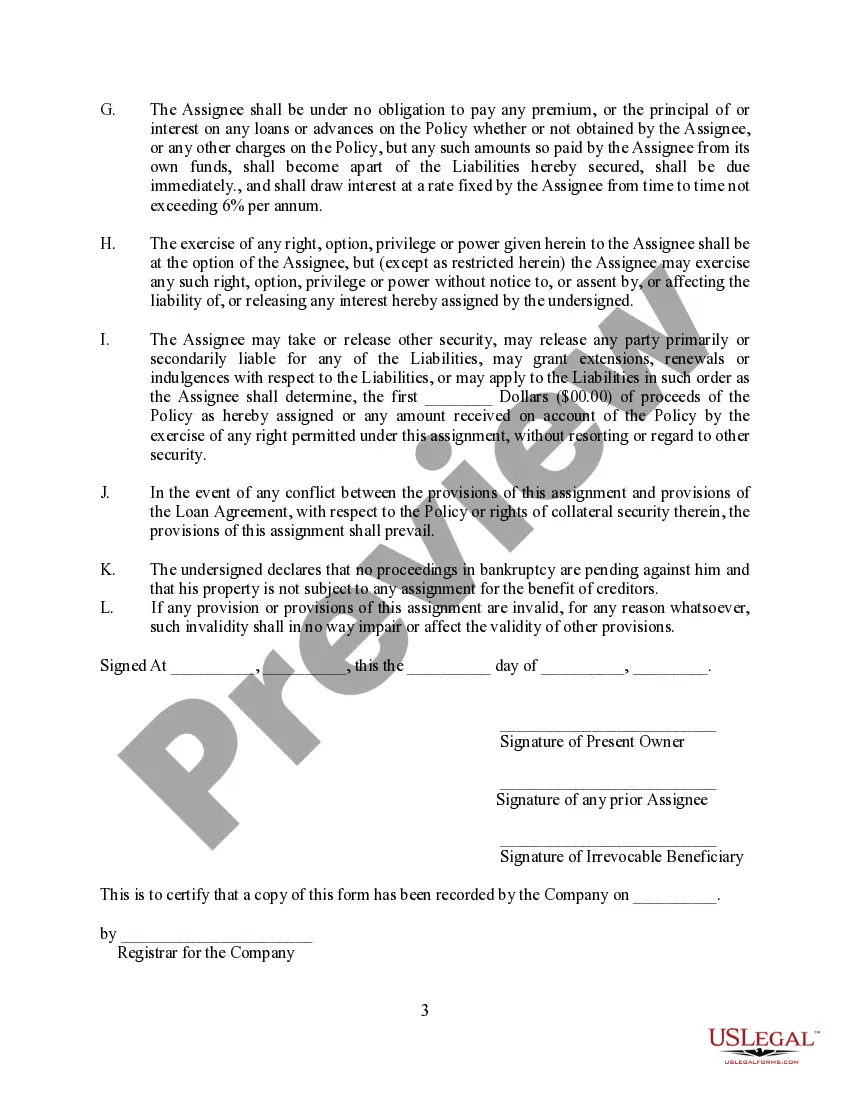

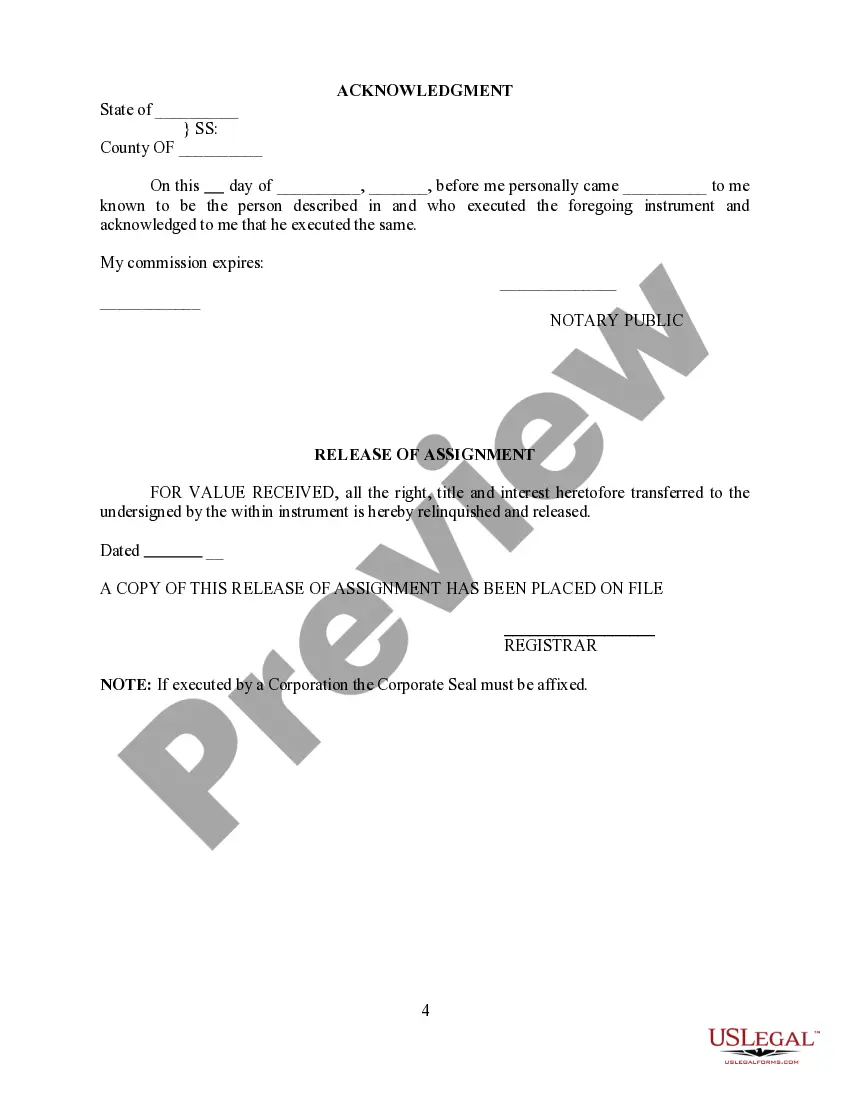

Idaho Partial Assignment of Life Insurance Policy as Collateral refers to a legal agreement that allows a policyholder to assign a portion of their life insurance policy's benefits as collateral for a loan. This arrangement is commonly used to secure loans or lines of credit, providing lenders with assurance in case the borrower is unable to repay the debt. It is important to note that partial assignment allows the policyholder to retain ownership and access to the remaining benefits and cash value of the policy. In Idaho, there are different types of partial assignments of life insurance policies, each with its own implications and conditions. Let's explore some of these variations: 1. Total Value Assignment: This type of assignment permits the policyholder to use the full value of their policy as collateral for a loan, up to a specified limit. In this case, the lender is entitled to receive the entire policy benefit in the event of the policyholder's death before repaying the loan. 2. Specific Loan Amount Assignment: With this type of partial assignment, the policyholder assigns only a specific amount of their policy's benefit as collateral, typically equivalent to the loan amount. If the policyholder passes away before repaying the loan, the lender can claim the predetermined assigned amount. 3. Percentage Assignment: In this scenario, the policyholder assigns a certain percentage of their policy's benefit as collateral. For instance, if a policyholder assigns 50% of their life insurance benefit, the lender can claim that percentage in the event of the policyholder's death. 4. Multiple Assignments: It is also possible for a policyholder to assign different portions of their life insurance policy as collateral to multiple creditors. However, this can make subsequent borrowing or modification of the policy more complicated. When considering a partial assignment of a life insurance policy as collateral in Idaho, it is crucial to consult with insurance and legal professionals to fully understand the terms, implications, and potential risks involved. Additionally, borrowers should carefully assess their ability to repay the loan in order to ensure they do not inadvertently jeopardize their life insurance coverage.

Idaho Partial Assignment of Life Insurance Policy as Collateral

Description

How to fill out Idaho Partial Assignment Of Life Insurance Policy As Collateral?

Have you been in a placement that you need papers for both business or individual uses almost every working day? There are a lot of legitimate papers web templates available on the Internet, but locating versions you can rely on is not straightforward. US Legal Forms gives a huge number of develop web templates, like the Idaho Partial Assignment of Life Insurance Policy as Collateral, which can be composed to fulfill federal and state demands.

Should you be currently informed about US Legal Forms web site and possess a merchant account, simply log in. After that, you can down load the Idaho Partial Assignment of Life Insurance Policy as Collateral format.

Should you not offer an accounts and would like to begin to use US Legal Forms, abide by these steps:

- Obtain the develop you need and make sure it is for that right town/area.

- Use the Review button to review the shape.

- Browse the explanation to ensure that you have chosen the correct develop.

- If the develop is not what you are trying to find, use the Research industry to get the develop that meets your needs and demands.

- If you obtain the right develop, simply click Acquire now.

- Pick the pricing plan you want, fill in the desired information to create your money, and pay money for the transaction making use of your PayPal or charge card.

- Choose a hassle-free file formatting and down load your backup.

Find each of the papers web templates you might have bought in the My Forms food selection. You can get a additional backup of Idaho Partial Assignment of Life Insurance Policy as Collateral at any time, if required. Just go through the needed develop to down load or produce the papers format.

Use US Legal Forms, one of the most comprehensive collection of legitimate types, to save time and steer clear of faults. The services gives professionally created legitimate papers web templates that can be used for a range of uses. Produce a merchant account on US Legal Forms and commence making your lifestyle a little easier.