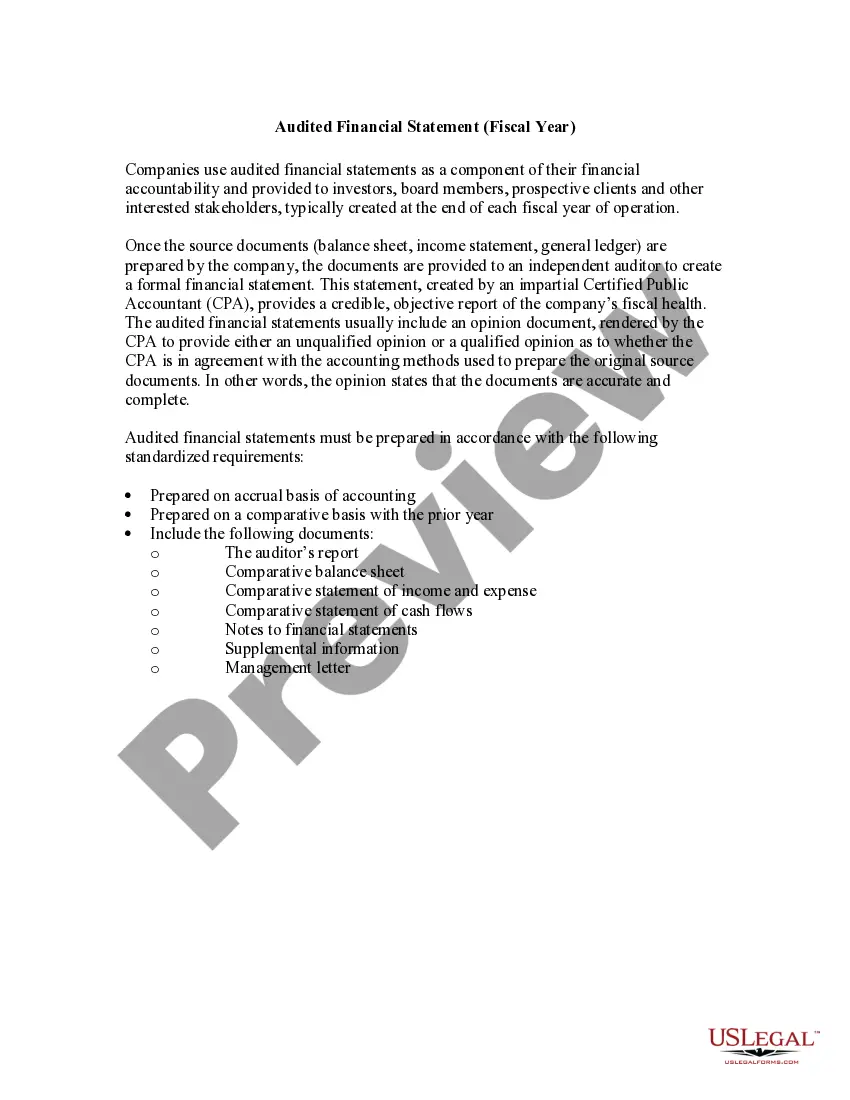

As most commonly used in legal settings, an audit is an examination of financial records and documents and other evidence by a trained accountant. Audits are conducted of records of a business or governmental entity, with the aim of ensuring proper accounting practices, recommendations for improvements, and a balancing of the books. An audit performed by employees is called "internal audit," and one done by an independent (outside) accountant is an "independent audit." Auditors may refuse to sign the audit to guarantee its accuracy if only limited records are produced.

Idaho Report of Independent Accountants after Audit of Financial Statements

Category:

State:

Multi-State

Control #:

US-01939BG

Format:

Word

Instant download

Description

How to fill out Report Of Independent Accountants After Audit Of Financial Statements?

Are you in a circumstance where you require documents for both business or personal purposes almost daily.

There are countless valid document templates available online, but finding ones you can rely on is challenging.

US Legal Forms offers thousands of template documents, such as the Idaho Report of Independent Accountants following the Audit of Financial Statements, which can be tailored to meet federal and state requirements.

Choose a convenient file format and download your copy.

Access all the document templates you have ordered in the My documents section. You can retrieve another version of the Idaho Report of Independent Accountants after Audit of Financial Statements at any time, if required. Just click on the desired template to download or print the format.

- If you are already familiar with the US Legal Forms website and have an account, simply Log In.

- Then, you can download the Idaho Report of Independent Accountants after Audit of Financial Statements template.

- If you do not have an account and wish to start using US Legal Forms, follow these steps.

- Find the template you need and ensure it is appropriate for your specific location/region.

- Use the Preview button to review the form.

- Examine the information to confirm you have selected the correct template.

- If the template is not what you are seeking, utilize the Search field to locate the form that fulfills your needs and criteria.

- When you find the right template, click Purchase now.

- Select the pricing plan you prefer, complete the necessary details to create your account, and finalize an order using your PayPal or credit card.

Form popularity

FAQ

The function of an independent audit is to provide an objective evaluation of a company's financial statements. This process helps ensure accuracy and transparency, building trust among stakeholders. The Idaho Report of Independent Accountants after Audit of Financial Statements plays a vital role in this by documenting the auditor’s findings and opinions.

An unmodified audit report is a type of opinion issued by auditors when they find no significant issues with a company's financial statements. This type of report indicates that the financials fairly represent the company’s performance. An unmodified Idaho Report of Independent Accountants after Audit of Financial Statements can boost investor confidence.

Typically, companies are required to provide at least three years of audited financial statements when seeking to go public. These statements should reflect the company's financial performance over time. The Idaho Report of Independent Accountants after Audit of Financial Statements can help potential investors assess the company before making decisions.

An independent accountant is a financial professional who offers accounting services without any affiliations or conflicts of interest with the client. This independence is essential for ensuring unbiased evaluations. The Idaho Report of Independent Accountants after Audit of Financial Statements is typically prepared by such professionals to ensure its reliability.

An independent auditor in accounting is a qualified professional who is not connected to the company being audited. Their role is crucial in providing an impartial review of the financial statements. This impartiality ensures that the Idaho Report of Independent Accountants after Audit of Financial Statements reflects a fair assessment of the company's financial health.

Yes, audited financial statements are generally public information for companies that are publicly traded. These statements must be filed with regulatory authorities, allowing investors and the general public access. The Idaho Report of Independent Accountants after Audit of Financial Statements also becomes part of public records, contributing to transparency.

An independent audit report is created by an external auditor, while a statutory audit report is required by law for certain organizations. Both serve to enhance trust in financial reporting, but a statutory audit focuses on compliance with legal requirements. The Idaho Report of Independent Accountants after Audit of Financial Statements is an example of an independent audit report.

An independent audit report is a formal evaluation provided by an external auditor after reviewing a company's financial statements. This report outlines the auditor's opinion on whether the financial statements truly represent the company's financial position. You will find crucial insights within the Idaho Report of Independent Accountants after Audit of Financial Statements.

An independent financial audit is a comprehensive examination of a company's financial statements conducted by an external auditor. This type of audit aims to provide objective assurance regarding the fairness of these statements. The resulting Idaho Report of Independent Accountants after Audit of Financial Statements serves as a trustworthy tool for stakeholders making financial decisions.

Auditing usually refers to the review of a company's financial statements by an internal or external party. Independent auditing, on the other hand, involves third-party auditors who are not affiliated with the company. This ensures objectivity, enhancing the credibility of the Idaho Report of Independent Accountants after Audit of Financial Statements.