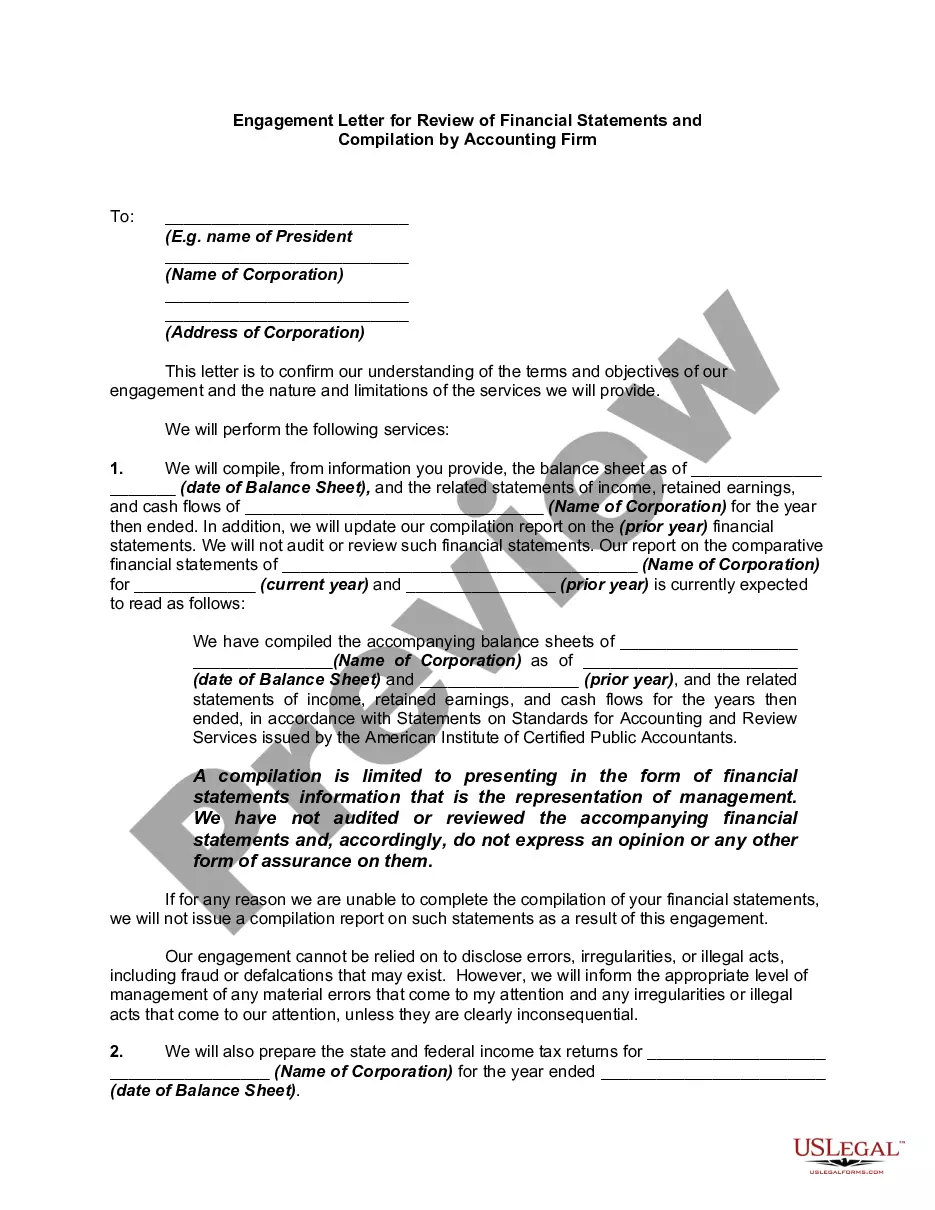

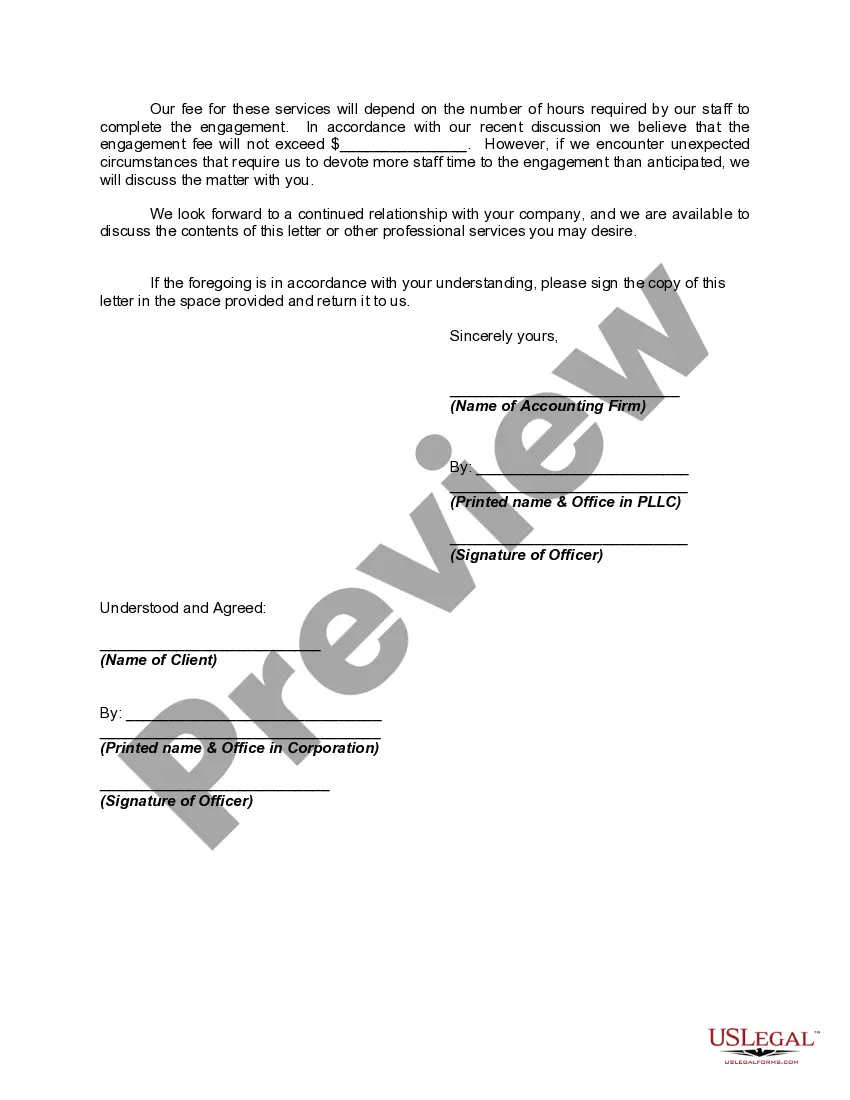

Compiled financial statements represent the most basic level of service that certified public accountants provide with respect to financial statements. In a compilation, the CPA must comply with certain basic requirements of professional standards, such as having a knowledge of the client's industry and applicable accounting principles, having a clear understanding with the client as to the services to be provided, and reading the financial statements to determine whether there are any obvious departures from generally accepted accounting principles (or, in some cases, another comprehensive basis of accounting used by the entity). It may be necessary for the CPA to perform "other accounting services" (such as creating a general ledger for the client, or assisting the client with adjusting entries for the books of the client (before the financial statements can be prepared). Upon completion, a report on the financial statements is issued that states a compilation was performed in accordance with AICPA professional standards, but no assurance is expressed that the statements are in conformity with generally accepted accounting principles. This is known as the expression of "no assurance." Compiled financial statements are often prepared for privately-held entities that do not need a higher level of assurance expressed by the CPA.

Idaho Engagement Letter for Review of Financial Statements and Compilation by Accounting Firm An engagement letter is a crucial document that formalizes the relationship between a business owner and an accounting firm in the state of Idaho. This letter outlines the terms, scope, and responsibilities of both parties involved in the engagement for the review of financial statements and compilation services. It sets clear expectations and ensures a smooth collaboration between the business and the accounting firm. Idaho Engagement Letter for Review of Financial Statements: This engagement letter specifically focuses on the process of reviewing financial statements. It is a detailed examination of the financial records and transactions of a business, providing limited assurance to users of the financial statements. A review engagement does not require the same level of testing and verification as an audit but involves analytical procedures and inquiries to assess the reasonableness of the financial information. Idaho Engagement Letter for Compilation of Financial Statements: This engagement letter pertains to the compilation of financial statements. Compilation is the process of presenting financial information without providing any assurance. The accounting firm assists the client in organizing and presenting their financial data in a proper format, ensuring compliance with the relevant accounting standards. However, no opinion or assurance is expressed regarding the accuracy or completeness of the financial information. Idaho Compilation Engagement Letter for Internal Use Only: This specific engagement letter is designed for cases where the compiled financial statements are solely for internal use. It highlights that the compiled information is not intended for external parties such as lenders, investors, or regulators but serves as an important tool for business owners to assess and manage their financial performance internally. Idaho Compilation Engagement Letter for External Use: This engagement letter is applicable when the compiled financial statements are intended for external users, such as potential investors, lenders, or regulatory authorities. It emphasizes the accounting firm's responsibility to ensure that the compiled financial statements comply with the applicable accounting standards and are free from material misstatements. Some common keywords related to the Idaho Engagement Letter for Review of Financial Statements and Compilation by Accounting Firm include: — Idaho engagemenletterte— - Review of financial statements — Compilation of financial statement— - Limited assurance — Analytical procedure— - Inquiries - Compliance with accounting standards — InternaSonnynl— - External use - Material misstatements — Assurance service— - Accounting firm - Business owner — FinanciaDATat— - Financial performance. Note: Please keep in mind that this is a generalized description, and it is always recommended consulting legal or accounting professionals for specific engagement letter requirements and compliance with the Idaho jurisdiction's regulations.Idaho Engagement Letter for Review of Financial Statements and Compilation by Accounting Firm An engagement letter is a crucial document that formalizes the relationship between a business owner and an accounting firm in the state of Idaho. This letter outlines the terms, scope, and responsibilities of both parties involved in the engagement for the review of financial statements and compilation services. It sets clear expectations and ensures a smooth collaboration between the business and the accounting firm. Idaho Engagement Letter for Review of Financial Statements: This engagement letter specifically focuses on the process of reviewing financial statements. It is a detailed examination of the financial records and transactions of a business, providing limited assurance to users of the financial statements. A review engagement does not require the same level of testing and verification as an audit but involves analytical procedures and inquiries to assess the reasonableness of the financial information. Idaho Engagement Letter for Compilation of Financial Statements: This engagement letter pertains to the compilation of financial statements. Compilation is the process of presenting financial information without providing any assurance. The accounting firm assists the client in organizing and presenting their financial data in a proper format, ensuring compliance with the relevant accounting standards. However, no opinion or assurance is expressed regarding the accuracy or completeness of the financial information. Idaho Compilation Engagement Letter for Internal Use Only: This specific engagement letter is designed for cases where the compiled financial statements are solely for internal use. It highlights that the compiled information is not intended for external parties such as lenders, investors, or regulators but serves as an important tool for business owners to assess and manage their financial performance internally. Idaho Compilation Engagement Letter for External Use: This engagement letter is applicable when the compiled financial statements are intended for external users, such as potential investors, lenders, or regulatory authorities. It emphasizes the accounting firm's responsibility to ensure that the compiled financial statements comply with the applicable accounting standards and are free from material misstatements. Some common keywords related to the Idaho Engagement Letter for Review of Financial Statements and Compilation by Accounting Firm include: — Idaho engagemenletterte— - Review of financial statements — Compilation of financial statement— - Limited assurance — Analytical procedure— - Inquiries - Compliance with accounting standards — InternaSonnynl— - External use - Material misstatements — Assurance service— - Accounting firm - Business owner — FinanciaDATat— - Financial performance. Note: Please keep in mind that this is a generalized description, and it is always recommended consulting legal or accounting professionals for specific engagement letter requirements and compliance with the Idaho jurisdiction's regulations.