Generally, a contract to employ a certified public accountant need not be in writing.

However, such contracts often call for services of a highly complex and technical nature, and hence they should be explicit in their terms, and they should be in writing. In particular, a written employment contract is necessary in order to avoid misunderstanding with the employer regarding the amount of the accountant's fee or compensation and the nature of its computation. This form is a generic example that may be referred to when preparing such a form for your particular state. It is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a form in a particular jurisdiction.

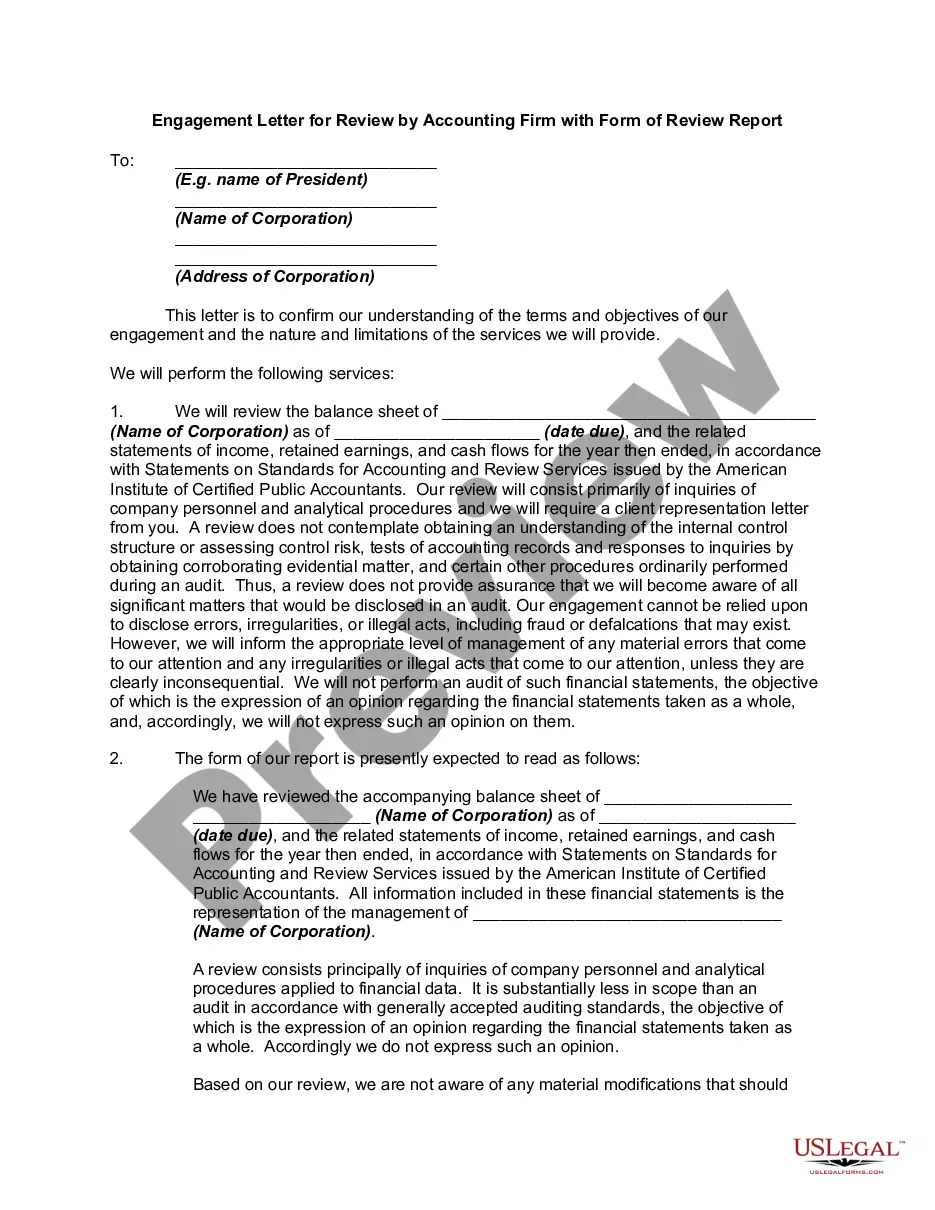

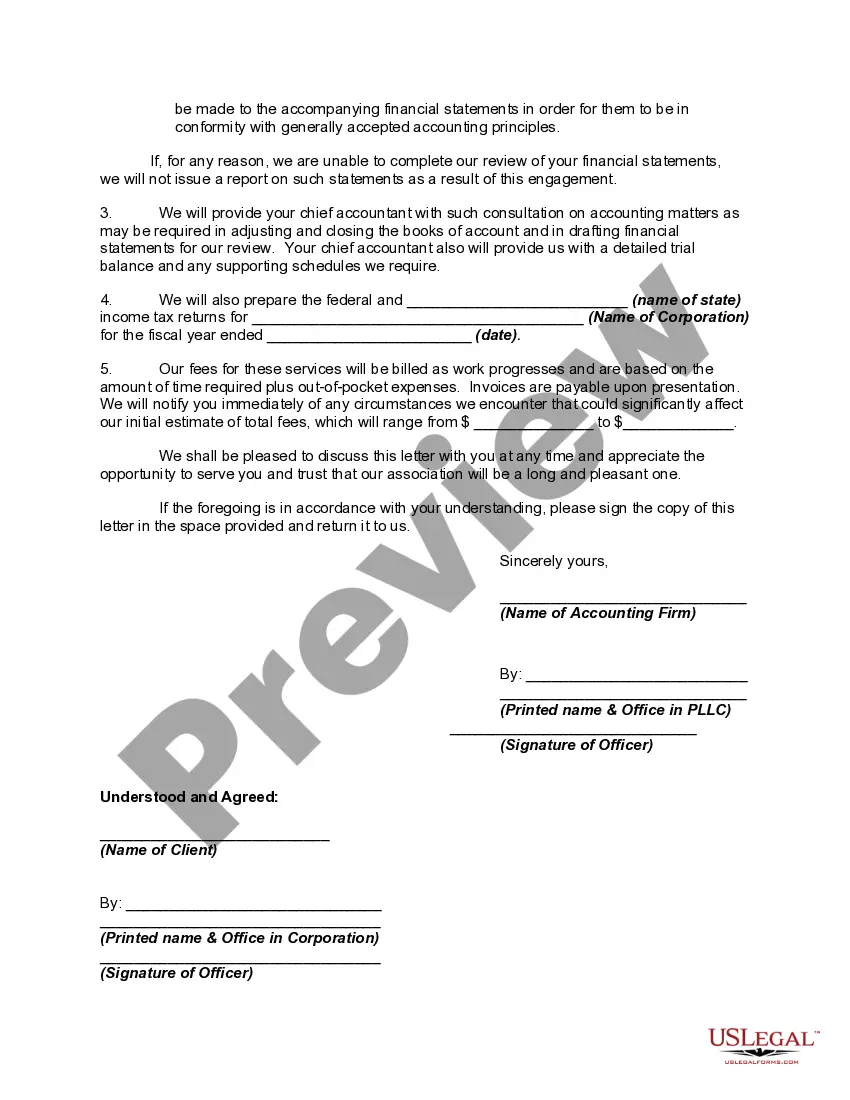

An Idaho engagement letter for review by an accounting firm with a form of review report is a critical document that outlines the terms, conditions, and expectations of an engagement between the accounting firm and its client in the state of Idaho. This engagement letter is specifically designed for conducting review engagements, which provide limited assurance on the financial statements and related information. The Idaho engagement letter for review serves as a legal agreement that clarifies the responsibilities of both parties and establishes the scope of the review engagement. It ensures that the accounting firm and the client are on the same page and avoid any misunderstandings or disputes down the line. Let's delve into the key components of the Idaho engagement letter for review: 1. Background Information: The engagement letter starts by identifying the accounting firm, the client, and any other relevant parties. It provides a brief overview of the client's business and the purpose of the engagement. 2. Objectives and Scope: This section outlines the specific objectives of the review engagement, such as assessing whether the financial statements are prepared in accordance with the applicable financial reporting framework. It also defines the limitations, responsibilities, and restrictions on the accounting firm's procedures. 3. Reporting: The engagement letter describes the format of the report that the accounting firm will issue upon completion of the review. In Idaho, the most common form of report issued for review engagements is the "Accountant's Review Report." 4. Materiality: The letter details the concept of materiality, including the materiality threshold to be used in the review. Materiality establishes the level at which errors or omissions in the financial statements could influence the decisions of users. 5. Independence: The engagement letter emphasizes the accounting firm's independence and confirms compliance with relevant professional codes of ethics. 6. Timelines and Fees: This section includes the expected completion date of the review, as well as a breakdown of the fees and billing arrangements. It may also address any additional costs or out-of-pocket expenses that might be incurred. 7. Work to Be Performed: The engagement letter specifies the procedures that the accounting firm will undertake during the review process. This typically includes analytical and inquiry procedures, but may vary depending on the client's specific needs. Additional types of Idaho engagement letters for review may exist based on the specific industry or business requirements, such as: 1. Nonprofit Organizations: Engagement letters tailored for review engagements of nonprofit organizations, considering unique accounting and reporting requirements. 2. Government Entities: Engagement letters catered towards review engagements of government entities, which often require compliance with specific regulations and reporting standards. 3. Financial Institutions: Engagement letters designed specifically for review engagements of banks, credit unions, or other financial institutions, which align with the industry-specific regulations imposed by regulatory bodies. It is essential for both the accounting firm and the client to carefully review, understand, and agree to the terms and conditions outlined in the Idaho engagement letter for review. By establishing clear expectations and responsibilities, this document ensures transparency, professionalism, and a successful review engagement process.