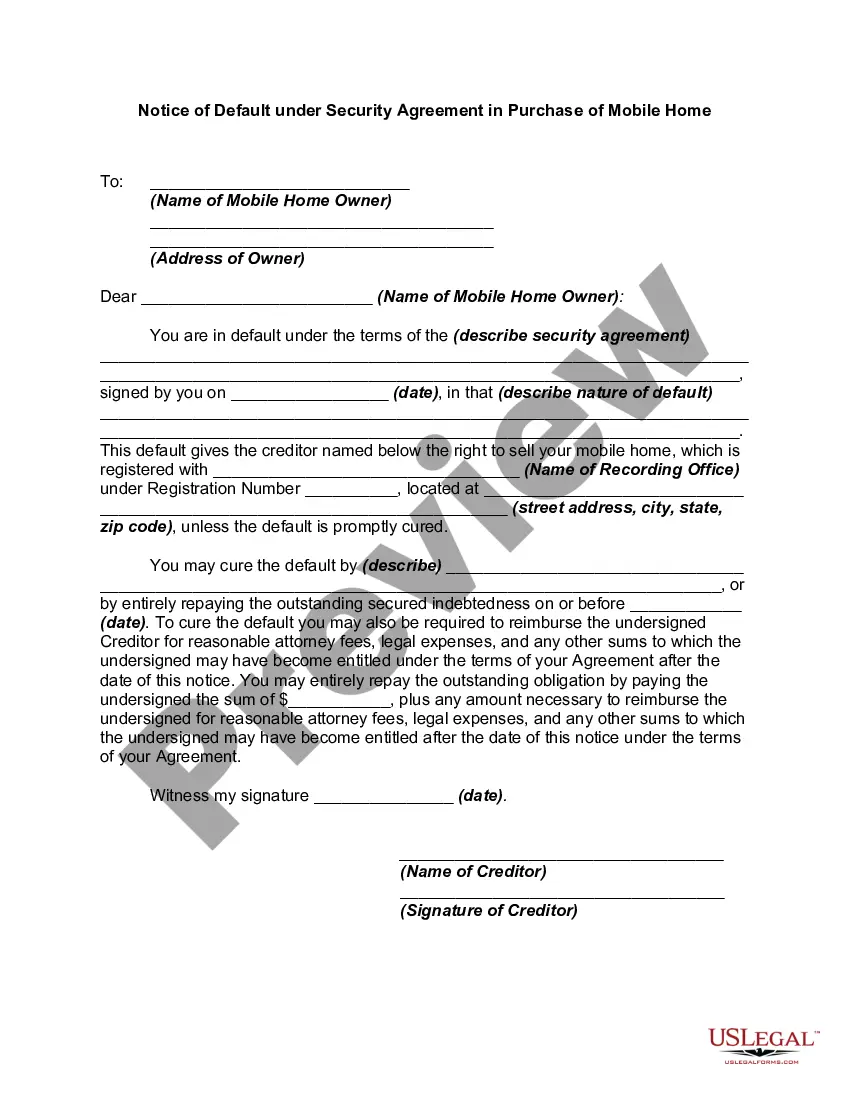

Keywords: Idaho, Notice of Default, Security Agreement, Purchase of Mobile Home A Notice of Default under Security Agreement in the Purchase of a Mobile Home is a legal document that serves as a warning or notification to the borrower in Idaho, informing them that they have failed to fulfill their obligations outlined in the security agreement related to the purchase of a mobile home. When a borrower defaults on their payments or breaches the terms of their agreement, the lender has the right to initiate the foreclosure process on the mobile home. There are two main types of Notice of Default in Idaho under a Security Agreement in the Purchase of a Mobile Home: 1. Pre-Foreclosure Notice: This notice is sent by the lender to the borrower when they have missed payments or violated the terms of the agreement. The purpose of this notice is to inform the borrower of their default status and provide them with a specific period to cure the default by making the required payments or rectifying the breach. The notice typically includes details such as the outstanding amount, the actions required to cure the default, and the timeframe given to comply before further legal actions are taken. 2. Foreclosure Sale Notice: If the borrower fails to cure the default within the given timeframe mentioned in the pre-foreclosure notice, the lender may proceed with initiating foreclosure proceedings. The foreclosure sale notice is then issued to the borrower, informing them of the lender's intent to sell the mobile home to recover the owed debt. This notice provides specific details about the foreclosure sale, including the date, time, and location of the sale. It also notifies the borrower of their right to redeem the property by paying off the outstanding debt before the sale date. It is important for borrowers to carefully review and understand the terms mentioned in the Notice of Default under Security Agreement in the Purchase of a Mobile Home in Idaho. Failure to take appropriate action to cure the default within the given timeframes may result in the loss of the mobile home and negative impacts on the borrower's credit history. Seeking legal advice is advised for borrowers facing default situations to understand their rights and explore possible alternatives to foreclosure.

Idaho Notice of Default under Security Agreement in Purchase of Mobile Home

Description

How to fill out Idaho Notice Of Default Under Security Agreement In Purchase Of Mobile Home?

If you want to total, down load, or print out legal record layouts, use US Legal Forms, the most important selection of legal kinds, which can be found on the web. Utilize the site`s simple and convenient lookup to get the paperwork you will need. Numerous layouts for organization and person reasons are categorized by categories and suggests, or keywords and phrases. Use US Legal Forms to get the Idaho Notice of Default under Security Agreement in Purchase of Mobile Home within a handful of click throughs.

If you are previously a US Legal Forms consumer, log in to the accounts and then click the Acquire button to obtain the Idaho Notice of Default under Security Agreement in Purchase of Mobile Home. Also you can gain access to kinds you in the past delivered electronically within the My Forms tab of the accounts.

If you are using US Legal Forms the very first time, follow the instructions under:

- Step 1. Make sure you have chosen the form to the appropriate city/country.

- Step 2. Use the Preview option to look over the form`s information. Never overlook to learn the explanation.

- Step 3. If you are not satisfied with the type, make use of the Search discipline at the top of the screen to get other models in the legal type template.

- Step 4. When you have identified the form you will need, click on the Buy now button. Opt for the rates plan you choose and put your credentials to register for an accounts.

- Step 5. Process the deal. You may use your Мisa or Ьastercard or PayPal accounts to perform the deal.

- Step 6. Find the formatting in the legal type and down load it on your own gadget.

- Step 7. Comprehensive, revise and print out or signal the Idaho Notice of Default under Security Agreement in Purchase of Mobile Home.

Every single legal record template you get is your own property permanently. You have acces to every single type you delivered electronically within your acccount. Go through the My Forms section and choose a type to print out or down load once again.

Contend and down load, and print out the Idaho Notice of Default under Security Agreement in Purchase of Mobile Home with US Legal Forms. There are thousands of skilled and condition-particular kinds you can use to your organization or person demands.