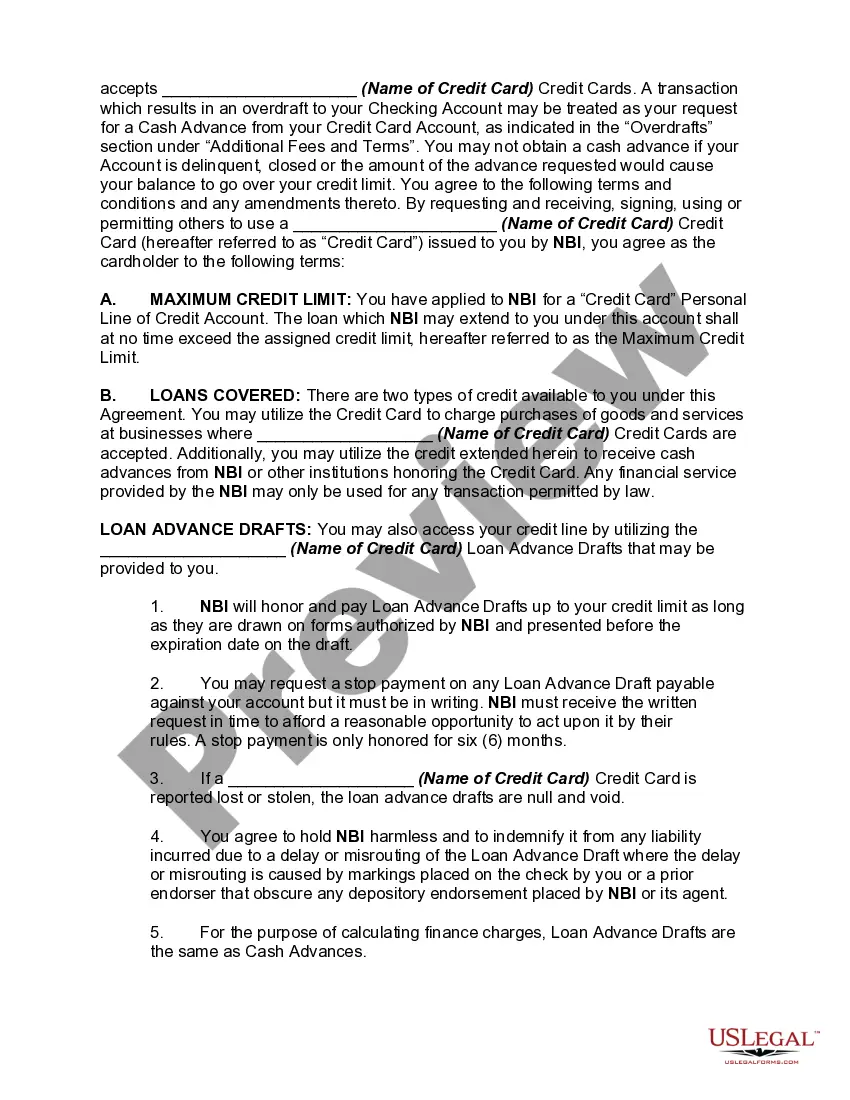

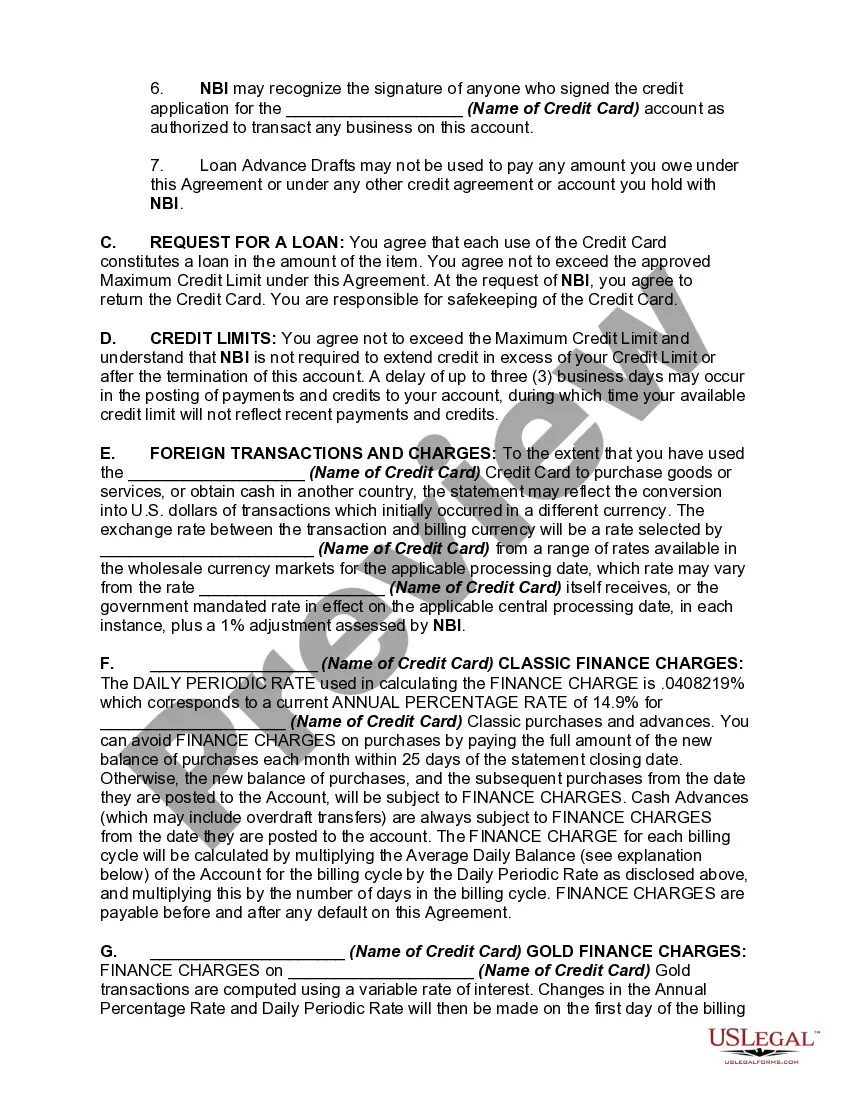

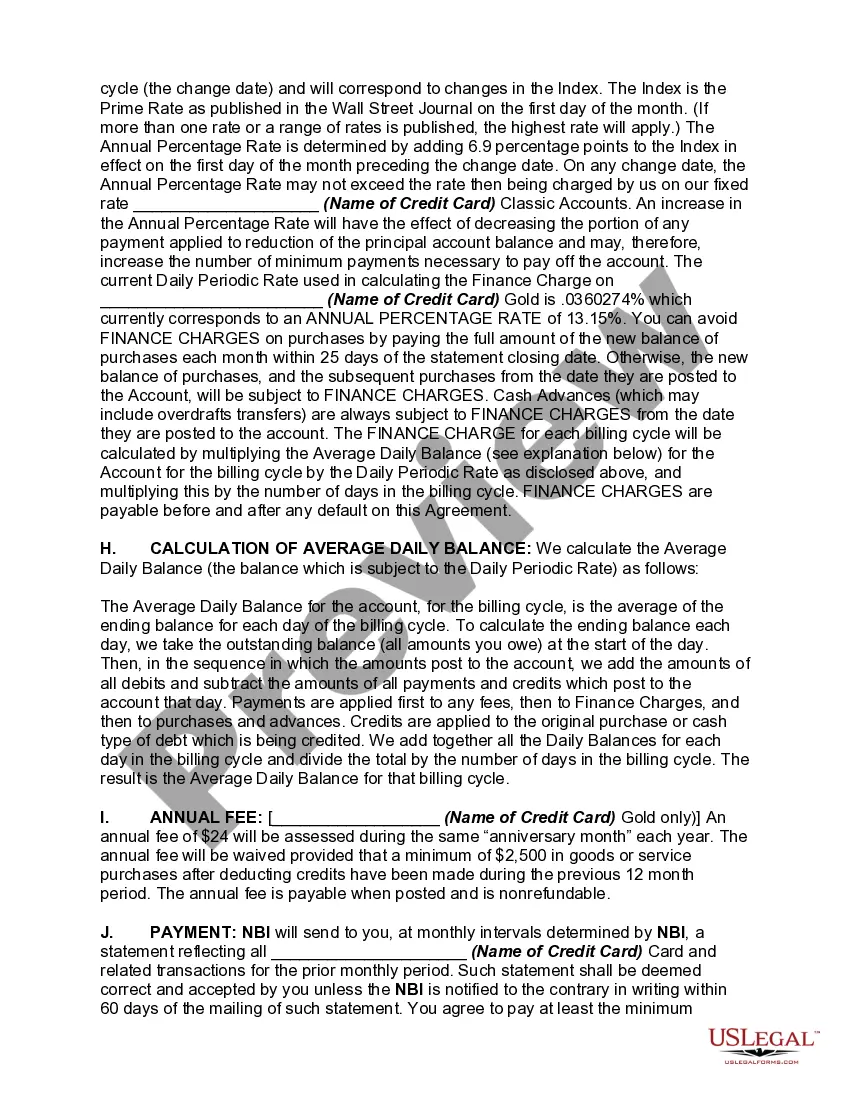

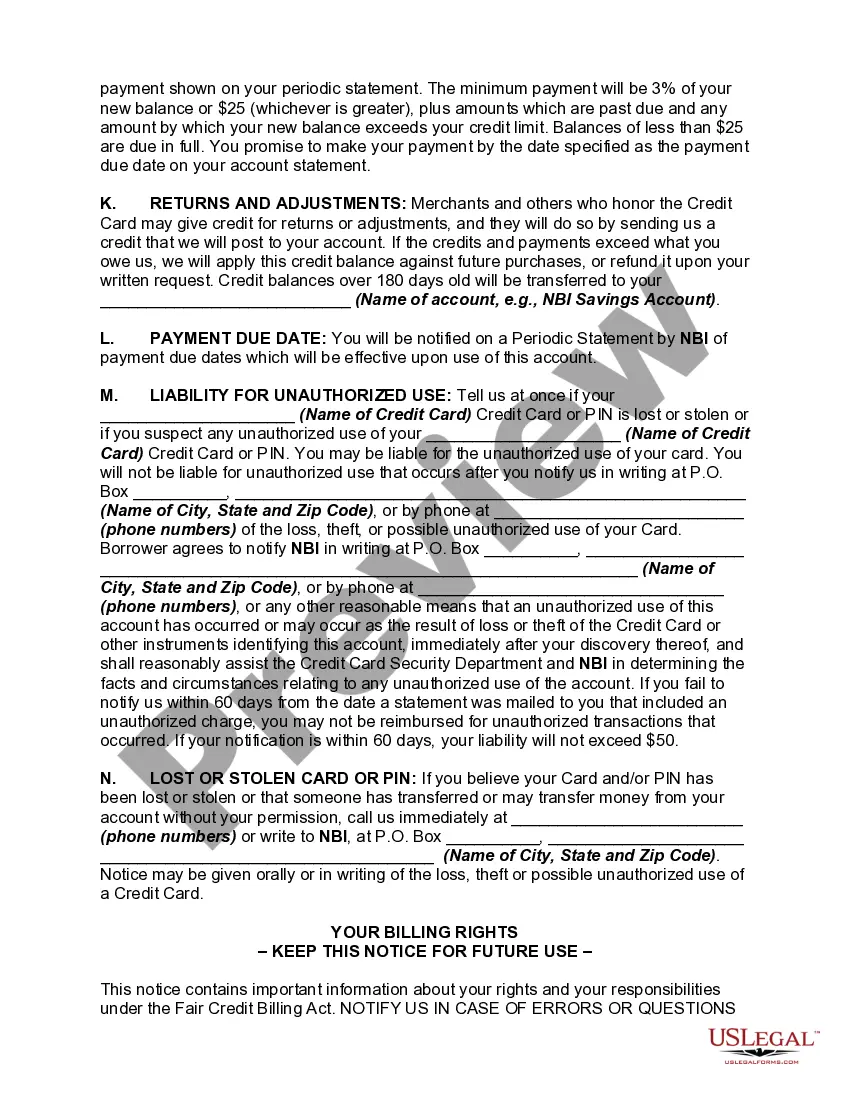

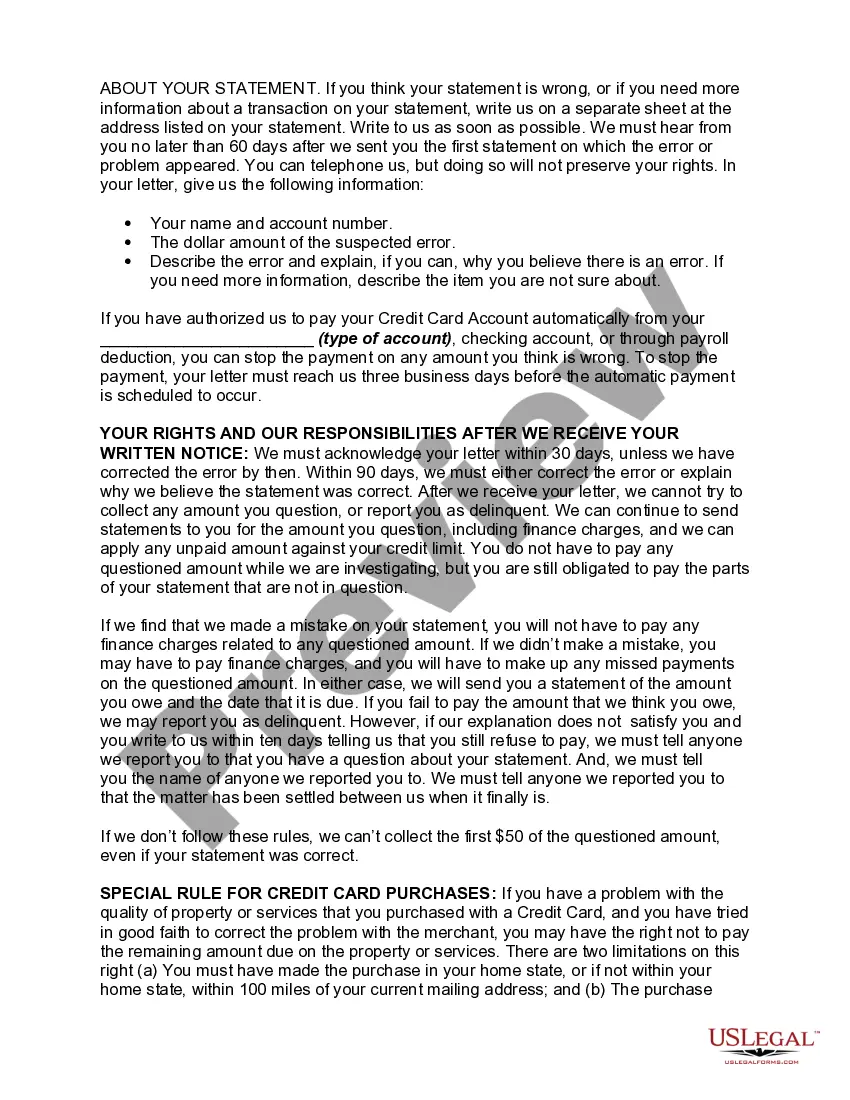

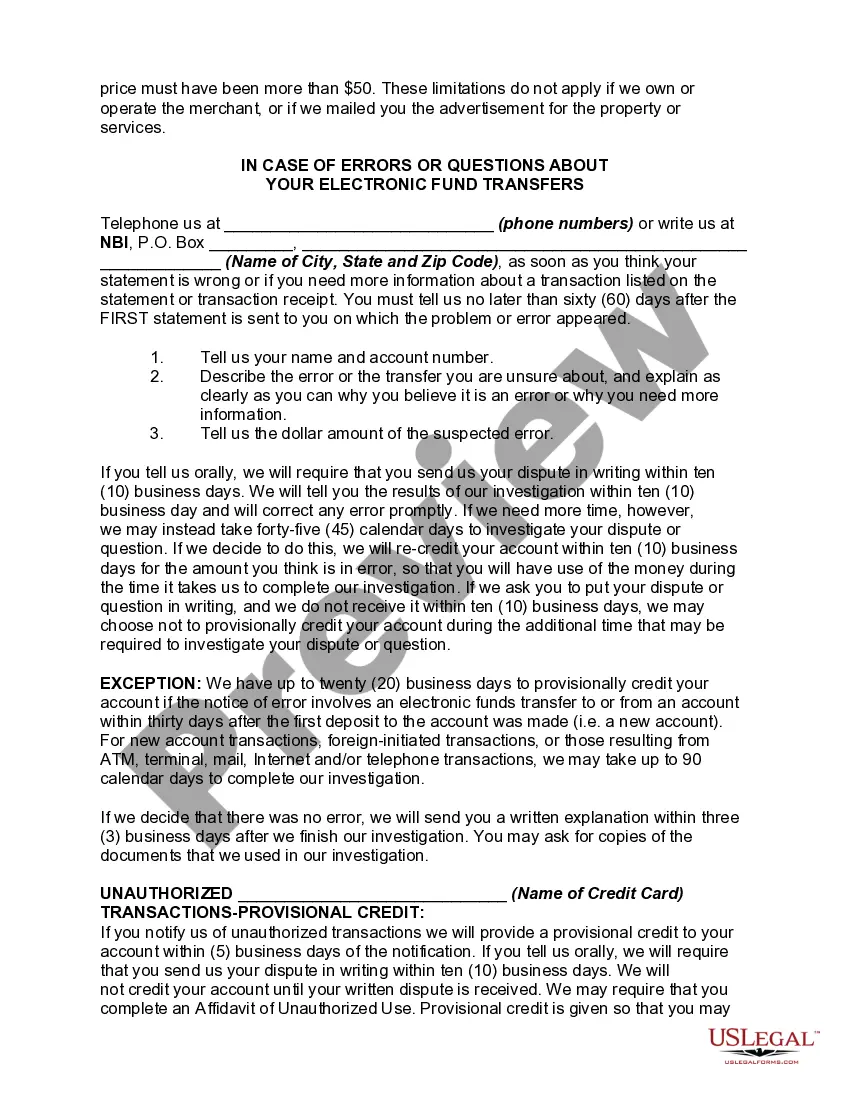

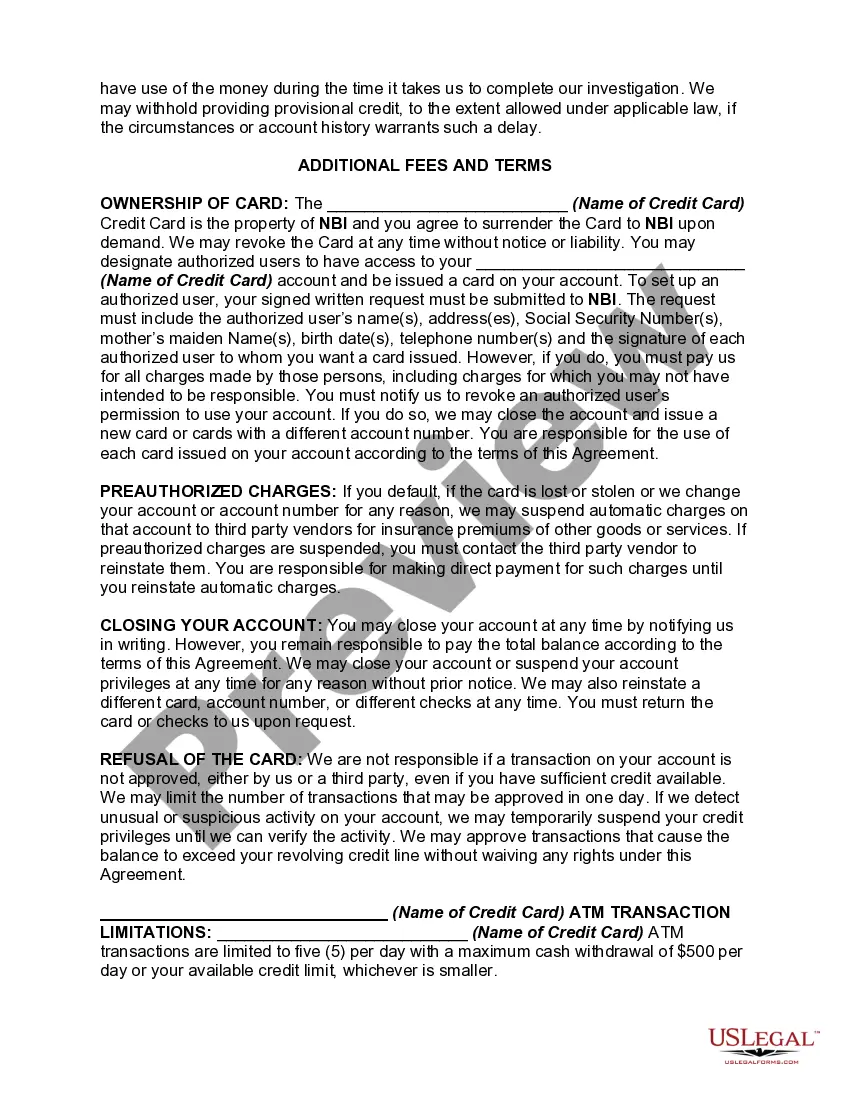

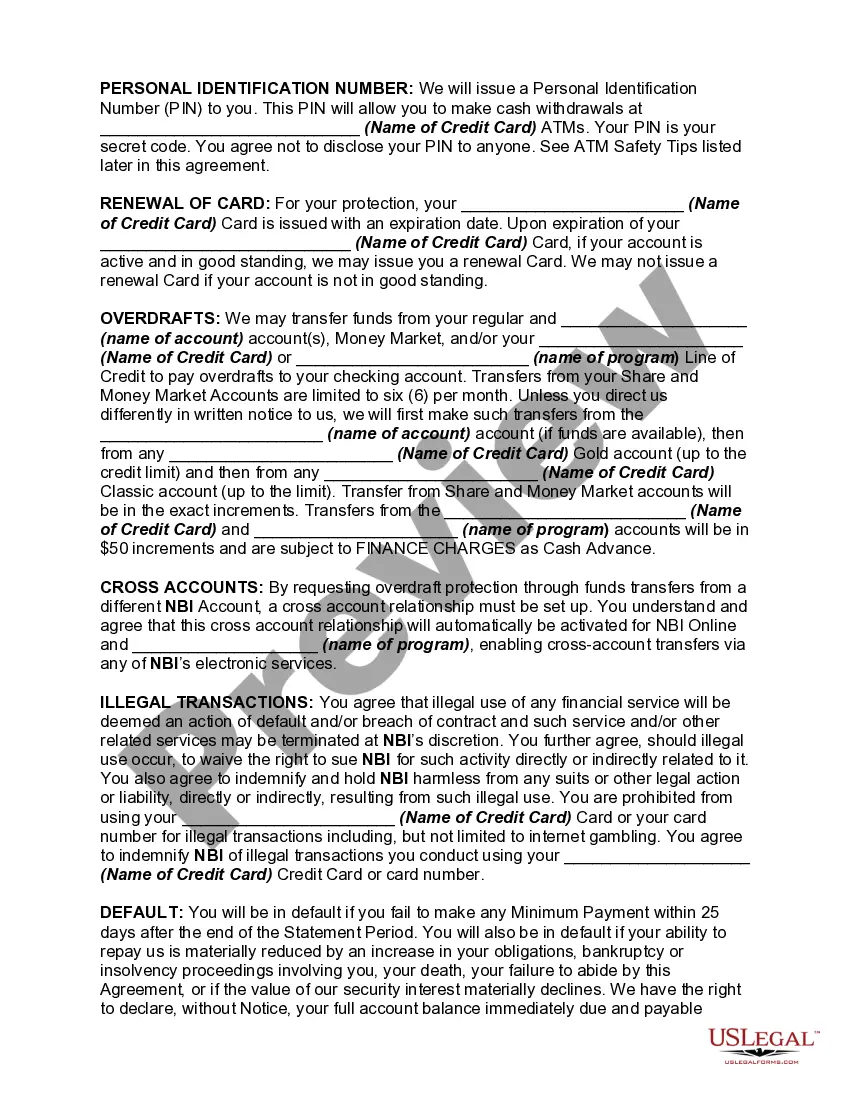

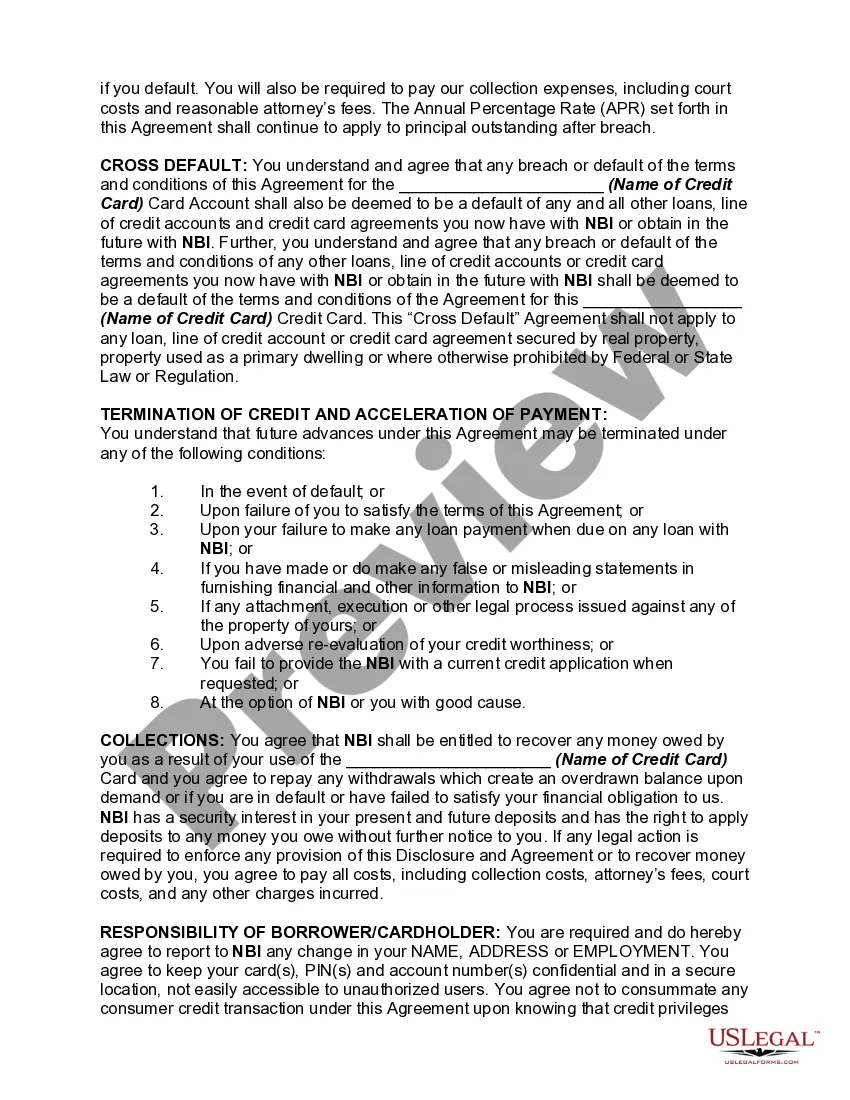

Idaho Credit Card Agreement and Disclosure Statement: A Comprehensive Overview The Idaho Credit Card Agreement and Disclosure Statement refers to a legal document that outlines the terms and conditions associated with credit cards issued within the state of Idaho. This agreement acts as a binding contract between the credit card issuer and the cardholder, detailing important information regarding the credit card's usage, fees, interest rates, and various terms. It serves to protect the rights and interests of both parties involved. The Idaho Credit Card Agreement and Disclosure Statement is designed to provide complete transparency and clarity to ensure cardholders fully understand the terms and conditions before initiating credit card usage. It includes relevant information such as: 1. Terms and Conditions: This section outlines the general rules and regulations governing the use of the credit card. It covers areas such as credit limits, cash advance availability, balance transfers, and the card's expiration date. 2. Annual Percentage Rate (APR): The agreement specifies the APR applicable to purchases made using the credit card. It may mention different APR's for purchases, cash advances, and balance transfers, each having their specific interest rates. 3. Billing and Payment Process: The document provides a detailed explanation of how billing cycles work, including the due dates for payments, minimum payment requirements, and late payment penalties. It also states how payment disputes and errors should be handled. 4. Fees and Charges: This section lists the various fees associated with the credit card, including annual fees, late payment fees, over-limit fees, and fees for cash advances or foreign transactions. Each fee's specific amount and conditions are disclosed, ensuring cardholders are aware of potential costs. 5. Credit Limit: The agreement mentions the credit limit placed on the cardholder, dictating how much can be charged on the credit card at any given time. 6. Grace Period: The grace period is the timeframe within which cardholders can avoid paying interest on their purchases if they pay their full balance on time. The specific length of the grace period is stated in the agreement. 7. Liability and Dispute Resolution: The agreement outlines the cardholder's liability for unauthorized transactions and describes the process for reporting fraudulent activity. It also clarifies how disputes between the cardholder and the credit card issuer should be resolved, such as through arbitration or mediation. Note: While there might not be distinct types of Idaho Credit Card Agreement and Disclosure Statements, specific financial institutions or credit card issuers may have their own customized versions tailored to their particular credit card offerings. Therefore, it is recommended to refer to the specific agreement provided by the issuing institution for precise details and terms related to a particular credit card. Ultimately, the Idaho Credit Card Agreement and Disclosure Statement ensures that both the cardholder and the credit card issuer have a clear understanding of their rights and obligations, promoting transparency, fair practices, and responsible credit card usage within the state of Idaho.

Idaho Credit Card Agreement and Disclosure Statement

Description

How to fill out Idaho Credit Card Agreement And Disclosure Statement?

If you want to full, down load, or produce legitimate file themes, use US Legal Forms, the largest collection of legitimate kinds, which can be found on-line. Utilize the site`s simple and easy practical look for to get the papers you want. Different themes for organization and specific reasons are sorted by classes and states, or keywords. Use US Legal Forms to get the Idaho Credit Card Agreement and Disclosure Statement in just a number of click throughs.

When you are already a US Legal Forms customer, log in in your bank account and click the Obtain option to have the Idaho Credit Card Agreement and Disclosure Statement. You can even access kinds you previously saved within the My Forms tab of your own bank account.

If you are using US Legal Forms for the first time, follow the instructions beneath:

- Step 1. Be sure you have selected the shape for the appropriate city/region.

- Step 2. Make use of the Preview method to examine the form`s articles. Don`t neglect to read through the outline.

- Step 3. When you are unhappy together with the form, make use of the Lookup discipline near the top of the monitor to get other types in the legitimate form format.

- Step 4. Once you have discovered the shape you want, click the Acquire now option. Select the pricing program you prefer and put your references to sign up for an bank account.

- Step 5. Approach the deal. You should use your Мisa or Ьastercard or PayPal bank account to complete the deal.

- Step 6. Pick the format in the legitimate form and down load it on your own system.

- Step 7. Total, edit and produce or indicator the Idaho Credit Card Agreement and Disclosure Statement.

Every single legitimate file format you acquire is your own eternally. You possess acces to each and every form you saved in your acccount. Select the My Forms section and pick a form to produce or down load once more.

Contend and down load, and produce the Idaho Credit Card Agreement and Disclosure Statement with US Legal Forms. There are millions of professional and condition-distinct kinds you may use for your personal organization or specific requirements.