This form is a generic example that may be referred to when preparing such a form for your particular state. It is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a form in a particular jurisdiction.

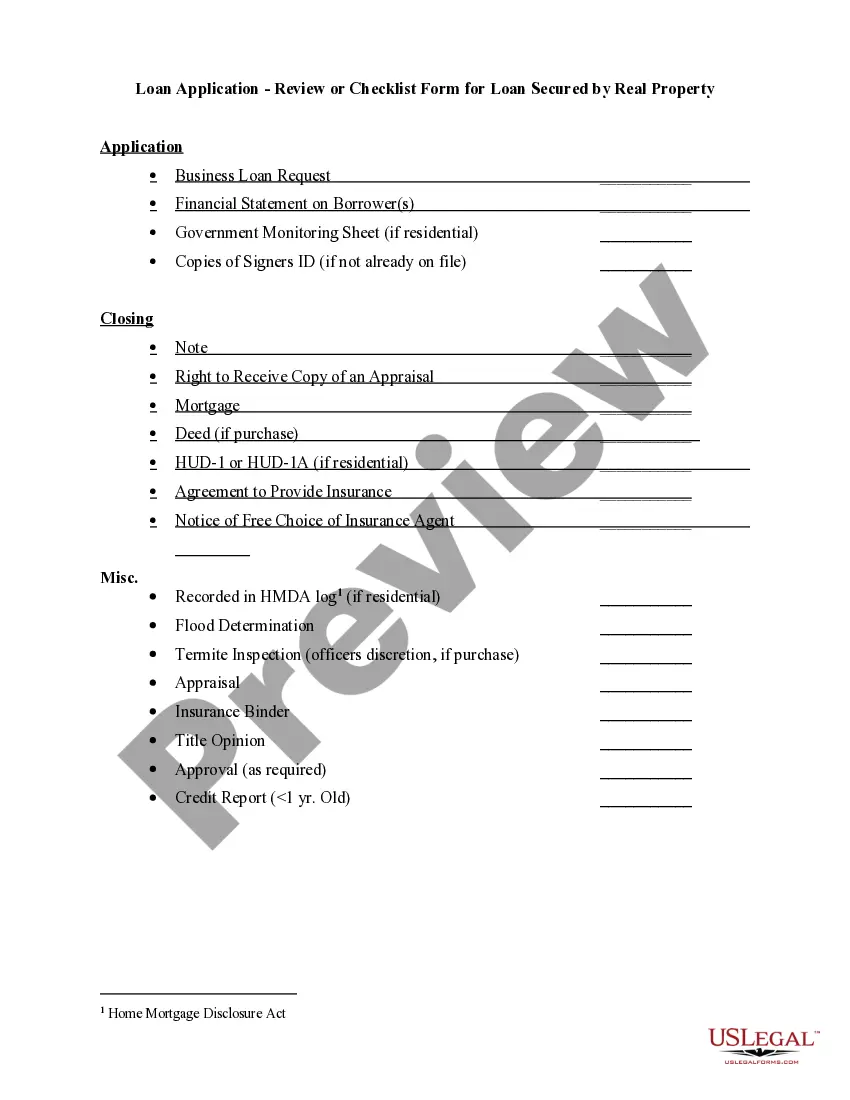

Idaho Loan Application - Review or Checklist Form for Loan Secured by Real Property

Category:

State:

Multi-State

Control #:

US-03039BG

Format:

Word;

Rich Text

Instant download

Description

How to fill out Loan Application - Review Or Checklist Form For Loan Secured By Real Property?

If you need to comprehensive, down load, or produce lawful document templates, use US Legal Forms, the greatest selection of lawful kinds, that can be found on the web. Use the site`s simple and easy practical research to get the files you will need. Various templates for company and personal reasons are categorized by categories and suggests, or keywords and phrases. Use US Legal Forms to get the Idaho Loan Application - Review or Checklist Form for Loan Secured by Real Property in just a number of mouse clicks.

In case you are previously a US Legal Forms buyer, log in to your account and then click the Down load option to find the Idaho Loan Application - Review or Checklist Form for Loan Secured by Real Property. You can even accessibility kinds you formerly downloaded inside the My Forms tab of the account.

If you work with US Legal Forms the very first time, refer to the instructions beneath:

- Step 1. Make sure you have chosen the form for the appropriate area/country.

- Step 2. Use the Review option to look through the form`s articles. Don`t forget to see the information.

- Step 3. In case you are not satisfied with all the kind, make use of the Look for discipline near the top of the screen to find other types in the lawful kind design.

- Step 4. Once you have discovered the form you will need, click the Get now option. Opt for the costs program you favor and include your references to sign up for an account.

- Step 5. Process the transaction. You should use your Мisa or Ьastercard or PayPal account to accomplish the transaction.

- Step 6. Choose the file format in the lawful kind and down load it in your gadget.

- Step 7. Comprehensive, revise and produce or signal the Idaho Loan Application - Review or Checklist Form for Loan Secured by Real Property.

Every single lawful document design you get is your own property permanently. You possess acces to every single kind you downloaded with your acccount. Select the My Forms section and pick a kind to produce or down load again.

Compete and down load, and produce the Idaho Loan Application - Review or Checklist Form for Loan Secured by Real Property with US Legal Forms. There are thousands of specialist and condition-certain kinds you can utilize for your company or personal needs.

Form popularity

FAQ

In California, loans can be secured by real property through a deed of trust. ingly, a deed of trust is a security instrument that functions like a mortgage.

Lenders require a few documents that can serve as proof of your identity and financial information to approve you for a loan. Some of the documents you'll be asked to provide include, copies of your state- or government-issued ID, copies of paystubs, tax returns or bank statements.

These documents are used by the lenders to evaluate whether or not they will provide you with a loan. Loan documents are necessary to initiate a loan approval process by a lender. Some documents that may be required are tax returns, bank statements, pay stubs, W2, and a proof of income.

What Is Collateral? Collateral in the financial world is a valuable asset that a borrower pledges as security for a loan. For example, when a homebuyer obtains a mortgage, the home serves as the collateral for the loan. For a car loan, the vehicle is the collateral.

Your income and employment history are good indicators of your ability to repay outstanding debt. Income amount, stability, and type of income may all be considered. The ratio of your current and any new debt as compared to your before-tax income, known as debt-to-income ratio (DTI), may be evaluated.

In California, loans can be secured by real property through a deed of trust. ingly, a deed of trust is a security instrument that functions like a mortgage.

Collateral loans come in many forms. For example, mortgages are collateral loans, and the real estate is collateral on the loan. The lender holds a lien on the mortgaged property, a mechanism that gives another entity conditional rights to your collateral if you default on the terms of the agreement.

Home equity loans for a paid-off house. Getting a loan on a house you already own lets you borrow against the value of your home without selling. The type of loan you'll qualify for depends on your credit score, debt-to-income ratio (DTI), loan-to-value ratio (LTV), and other factors.