Idaho Promissory Note - Long Form

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Promissory Note - Long Form?

Finding the appropriate legal document template can be a challenge.

Clearly, there are numerous templates available online, but how do you locate the legal form you require? Utilize the US Legal Forms website.

This service offers a vast array of templates, such as the Idaho Promissory Note - Long Form, which you can use for both business and personal purposes.

First, make sure you have selected the correct form for your city/state. You can preview the form using the Review option and read the form description to ensure it is suitable for you.

- All forms are reviewed by professionals and comply with federal and state regulations.

- If you are already registered, Log In to your account and click the Obtain button to access the Idaho Promissory Note - Long Form.

- Use your account to search for the legal forms you have previously purchased.

- Navigate to the My documents tab in your account to obtain another copy of the form you need.

- If you are a first-time user of US Legal Forms, here are some simple guidelines to follow.

Form popularity

FAQ

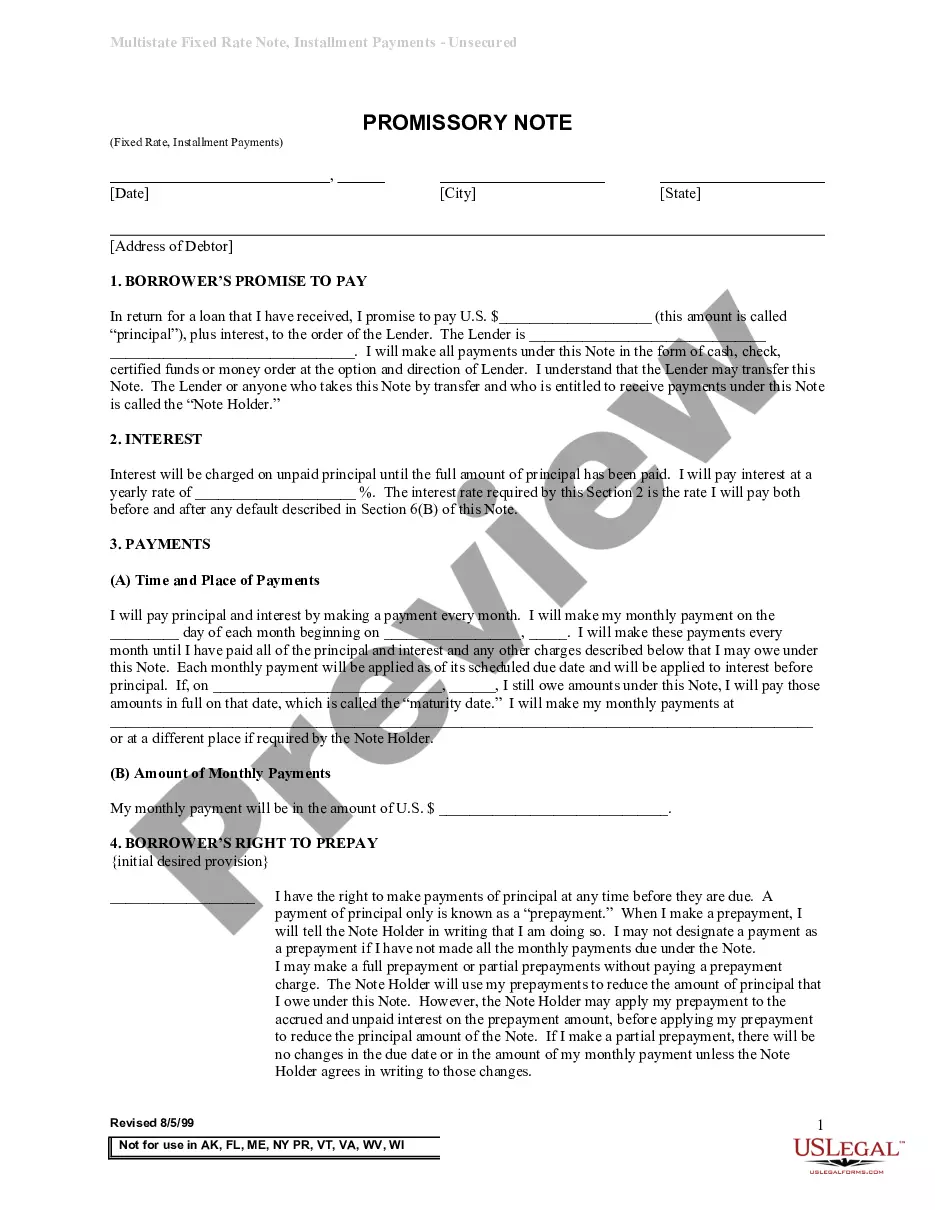

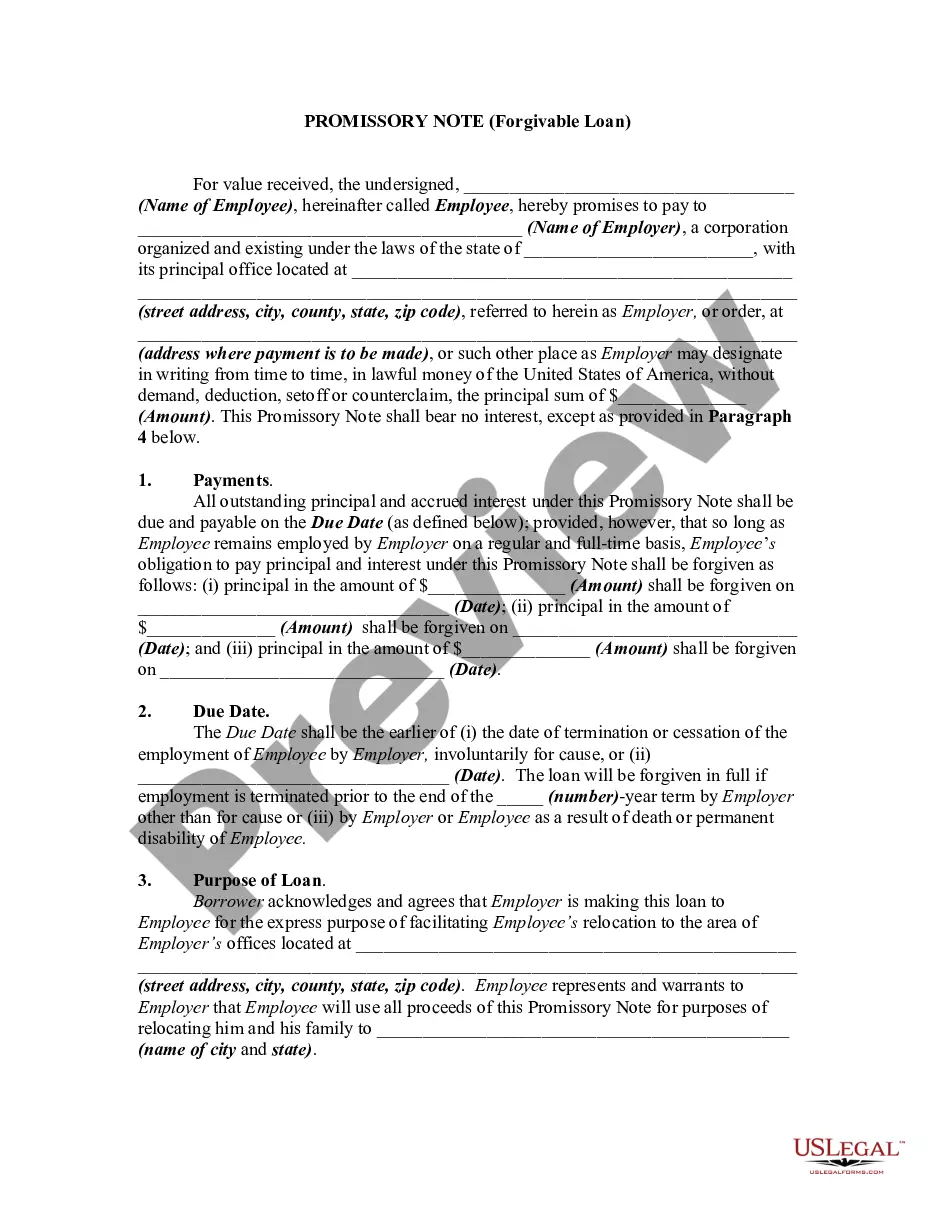

Filling out a promissory note involves writing down the names and addresses of both the borrower and lender at the top of the document. Next, state the amount borrowed, the interest rate, and the payment due date. It is also important to include any conditions or repayment terms that might apply. Explore the Idaho Promissory Note - Long Form on US Legal Forms for a convenient template to ensure accuracy.

To fill a demand promissory note, start by clearly labeling the document as a 'Demand Promissory Note.' Include the borrower's name and address, as well as the lender’s details. Specify the principal amount, interest rate, and any repayment terms. Make sure to sign and date the document to make it legally binding. For further assistance, consider using the Idaho Promissory Note - Long Form available on US Legal Forms.

The entry of the promissory note refers to the terms outlined within the document, specifying the agreement between the borrower and the lender. This includes the amount borrowed, interest rate, repayment schedule, and any other pertinent conditions. Your Idaho Promissory Note - Long Form should clearly detail these aspects for effective communication and record-keeping.

You typically do not need to file a promissory note with a governmental entity. Instead, you should keep it safe with your important documents. However, if you intend to enforce the note, it is wise to have it notarized and keep copies for both parties involved. Using the Idaho Promissory Note - Long Form can help streamline this process.

In Idaho, the maximum interest rate permitted is set by the state's usury laws, which generally cap it at 12% for most loans. However, if the parties to a promissory note agree on higher rates, it is crucial to ensure compliance with all applicable statutes. When creating an Idaho Promissory Note - Long Form, be vigilant about these limits and consider consulting services like US Legal Forms for accurate guidance.

A promissory note is generally a legally enforceable document as long as it meets necessary requirements and contains clear terms. Courts typically regard promissory notes as valid if both parties have agreed and signed. Therefore, when drafting your Idaho Promissory Note - Long Form, ensure it is comprehensive and well-defined to maximize enforceability and use helpful resources like US Legal Forms.

The length of a promissory note usually varies based on the agreement, but it can be as short as a few months or as long as several decades. However, state laws may impact the maximum allowable duration. When drafting your Idaho Promissory Note - Long Form, be sure to adhere to applicable regulations and outline your terms clearly for both parties.

Promissory notes can indeed be long term, depending on the agreement between the parties involved. While some notes may have short repayment periods, others, particularly in the case of loans for large amounts, often extend over many years. When creating your Idaho Promissory Note - Long Form, clearly state the duration to avoid confusion later on.

While you may not necessarily need a lawyer to create an Idaho Promissory Note - Long Form, consulting with one can provide peace of mind. A legal expert can help clarify terms and ensure compliance with state laws, preventing future disputes. For many, utilizing a reliable template from Uslegalforms offers a solid starting point, but having legal guidance can ensure all bases are covered.

The promissory note law in Idaho outlines the requirements for creating a valid note, including necessary disclosures and adherence to state regulations. An Idaho Promissory Note - Long Form must clearly state borrower and lender information, terms of repayment, and conditions for default. Being aware of these legal standards helps ensure your note is enforceable in a court of law. Comprehensive resources on Uslegalforms can guide you through these legal principles.