Ideally, no distributions to the beneficiaries under the will should be make until the estate is closed and closing letters received from the Internal Revenue Service and the State Tax Commission if estate tax returns were filed. This is not always possible, particularly in light of the fact that it generally takes a minimum of nine months to get a closing letter from the IRS. Beneficiaries are usually not that patient. The earliest an executor can close an estate is after the time to probate claims has expired and no claims have been probated. This is generally possible in estates that don't require estate tax returns, particularly when surviving spouse is the sole beneficiary.

After the time for probating claims against the estate has expired and estate taxes have been paid, a partial distribution to the beneficiaries may be in order, particularly if there are no unpaid claims outstanding against the estate and the closing attorney is comfortable that the estate tax return will be accepted by the IRS as filed.

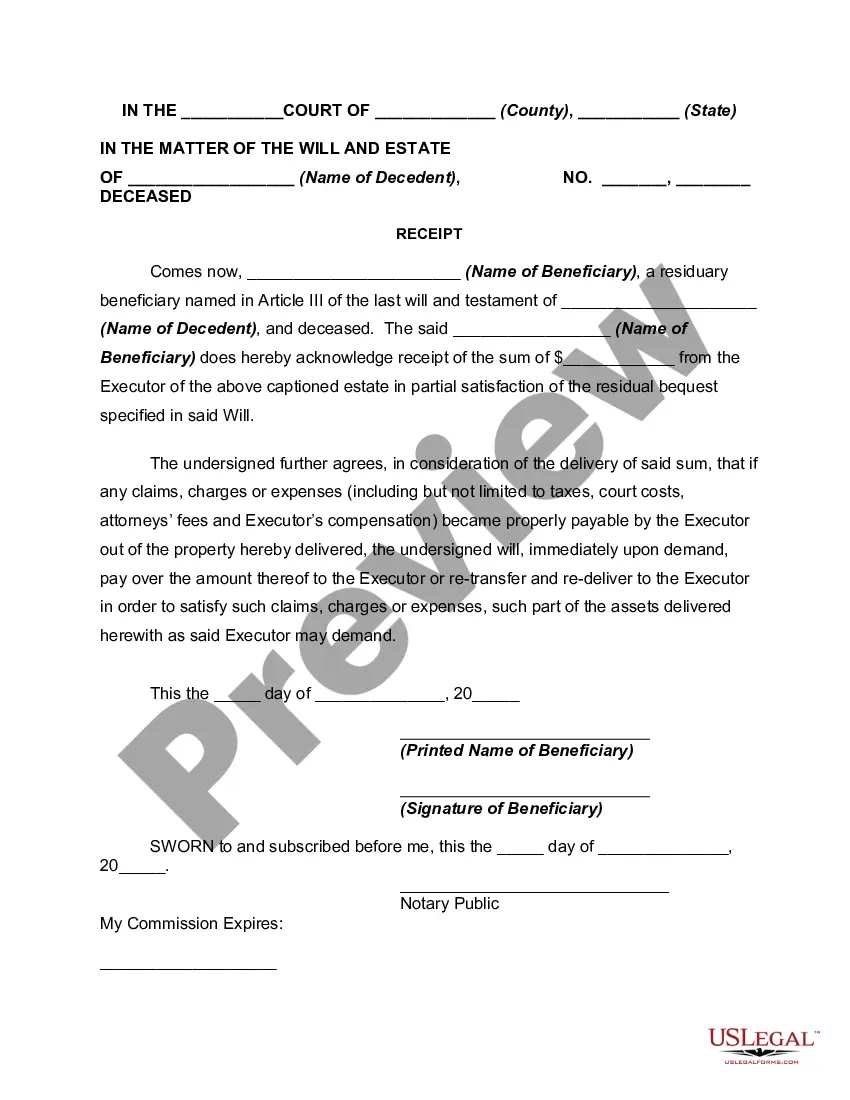

The Idaho Receipt of Beneficiary for Early Distribution from Estate and Indemnity Agreement is a legal document designed to outline the terms and conditions related to the early distribution of assets from an estate to a beneficiary. This agreement serves to protect both the estate and the beneficiary by establishing the responsibilities and rights of each party involved. Keywords: Idaho, Receipt of Beneficiary, Early Distribution, Estate, Indemnity Agreement There may be different types of Idaho Receipt of Beneficiary for Early Distribution from Estate and Indemnity Agreements, depending on the specific circumstances or preferences of the parties involved. Some possible variations of this document include: 1. Idaho Receipt of Beneficiary for Early Distribution from Estate and Indemnity Agreement — Minor Beneficiary: This agreement could be used when the beneficiary of the estate is a minor and requires additional safeguards and considerations. It would address legal aspects specific to minors, such as guardian appointment and management of funds until the beneficiary reaches legal adulthood. 2. Idaho Receipt of Beneficiary for Early Distribution from Estate and Indemnity Agreement — Inheritance Taxes: In cases where the estate is subject to inheritance taxes, this agreement might include provisions addressing the distribution of assets after accounting for tax obligations. It would outline how the beneficiary will receive their share while ensuring all tax liabilities are met. 3. Idaho Receipt of Beneficiary for Early Distribution from Estate and Indemnity Agreement — Contingent Beneficiary: If a beneficiary who is initially entitled to an early distribution becomes ineligible due to unforeseen circumstances, this agreement could be modified to accommodate a contingent beneficiary. It would define the conditions under which the contingent beneficiary would receive the distribution. 4. Idaho Receipt of Beneficiary for Early Distribution from Estate and Indemnity Agreement — Property Specific Distribution: In cases where the assets of the estate are diverse (e.g., real estate, financial accounts, personal property), this agreement could be tailored to address the particular distribution of specific assets to the beneficiary. It would outline the process for transfer of each designated asset. Overall, the Idaho Receipt of Beneficiary for Early Distribution from Estate and Indemnity Agreement provides a comprehensive framework for managing the early distribution of estate assets, prioritizing the beneficiary's interests while minimizing potential legal complications or disputes arising from the process.The Idaho Receipt of Beneficiary for Early Distribution from Estate and Indemnity Agreement is a legal document designed to outline the terms and conditions related to the early distribution of assets from an estate to a beneficiary. This agreement serves to protect both the estate and the beneficiary by establishing the responsibilities and rights of each party involved. Keywords: Idaho, Receipt of Beneficiary, Early Distribution, Estate, Indemnity Agreement There may be different types of Idaho Receipt of Beneficiary for Early Distribution from Estate and Indemnity Agreements, depending on the specific circumstances or preferences of the parties involved. Some possible variations of this document include: 1. Idaho Receipt of Beneficiary for Early Distribution from Estate and Indemnity Agreement — Minor Beneficiary: This agreement could be used when the beneficiary of the estate is a minor and requires additional safeguards and considerations. It would address legal aspects specific to minors, such as guardian appointment and management of funds until the beneficiary reaches legal adulthood. 2. Idaho Receipt of Beneficiary for Early Distribution from Estate and Indemnity Agreement — Inheritance Taxes: In cases where the estate is subject to inheritance taxes, this agreement might include provisions addressing the distribution of assets after accounting for tax obligations. It would outline how the beneficiary will receive their share while ensuring all tax liabilities are met. 3. Idaho Receipt of Beneficiary for Early Distribution from Estate and Indemnity Agreement — Contingent Beneficiary: If a beneficiary who is initially entitled to an early distribution becomes ineligible due to unforeseen circumstances, this agreement could be modified to accommodate a contingent beneficiary. It would define the conditions under which the contingent beneficiary would receive the distribution. 4. Idaho Receipt of Beneficiary for Early Distribution from Estate and Indemnity Agreement — Property Specific Distribution: In cases where the assets of the estate are diverse (e.g., real estate, financial accounts, personal property), this agreement could be tailored to address the particular distribution of specific assets to the beneficiary. It would outline the process for transfer of each designated asset. Overall, the Idaho Receipt of Beneficiary for Early Distribution from Estate and Indemnity Agreement provides a comprehensive framework for managing the early distribution of estate assets, prioritizing the beneficiary's interests while minimizing potential legal complications or disputes arising from the process.