Cash flow is the movement of cash into or out of a business, project, or financial product. It is usually measured during a specified, finite period of time. Measurement of cash flow can be used for calculating other parameters that give information on a company's value and situation. Cash flow can e.g. be used for calculating parameters:

To determine a project's rate of return or value. The time of cash flows into and out of projects are used as inputs in financial models such as internal rate of return and net present value.

To determine problems with a business's liquidity. Being profitable does not necessarily mean being liquid. A company can fail because of a shortage of cash even while profitable.

As an alternative measure of a business's profits when it is believed that accrual accounting concepts do not represent economic realities. For example, a company may be notionally profitable but generating little operational cash (as may be the case for a company that barters its products rather than selling for cash). In such a case, the company may be deriving additional operating cash by issuing shares or raising additional debt finance.

Cash flow can be used to evaluate the 'quality' of income generated by accrual accounting. When net income is composed of large non-cash items it is considered low quality.

To evaluate the risks within a financial product, e.g. matching cash requirements, evaluating default risk, re-investment requirements, etc.

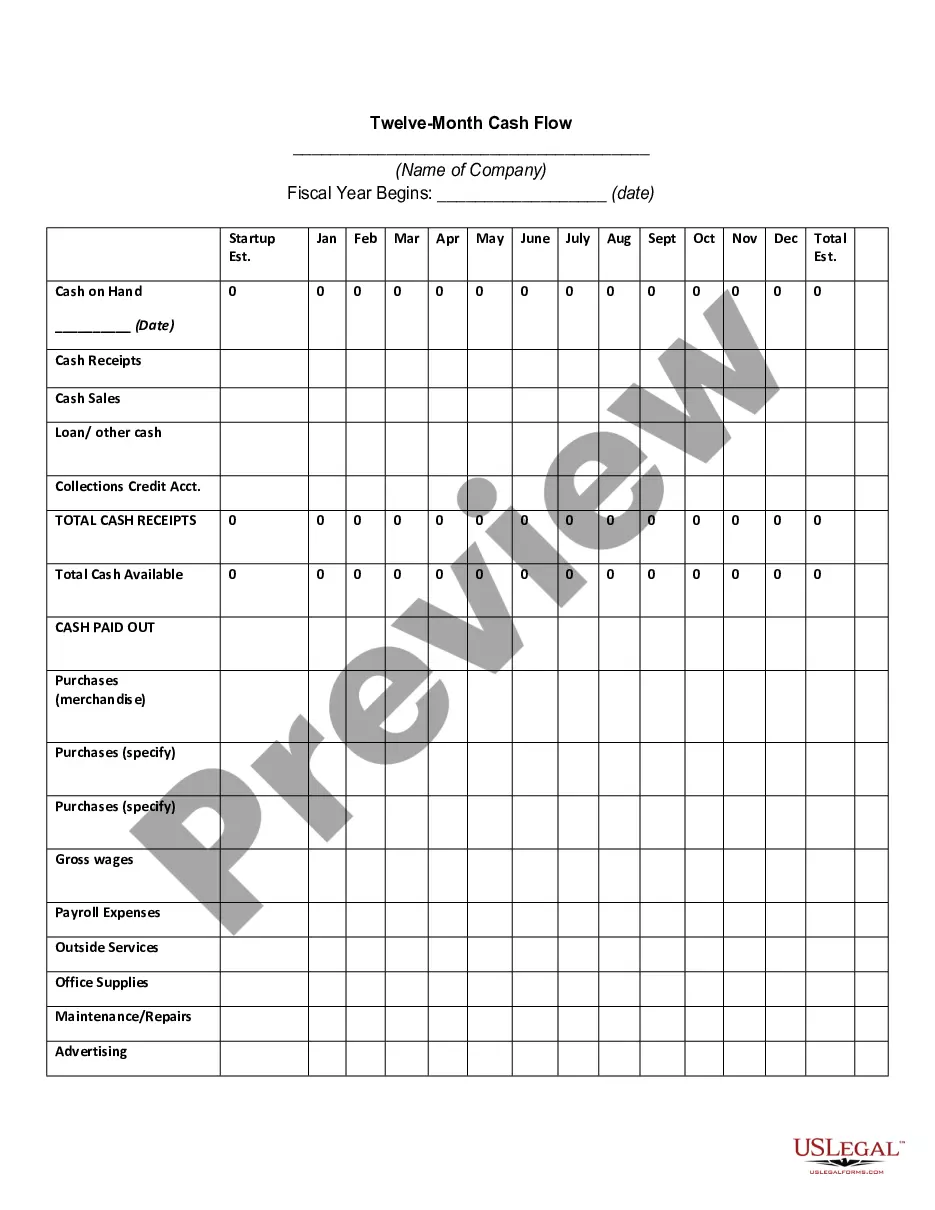

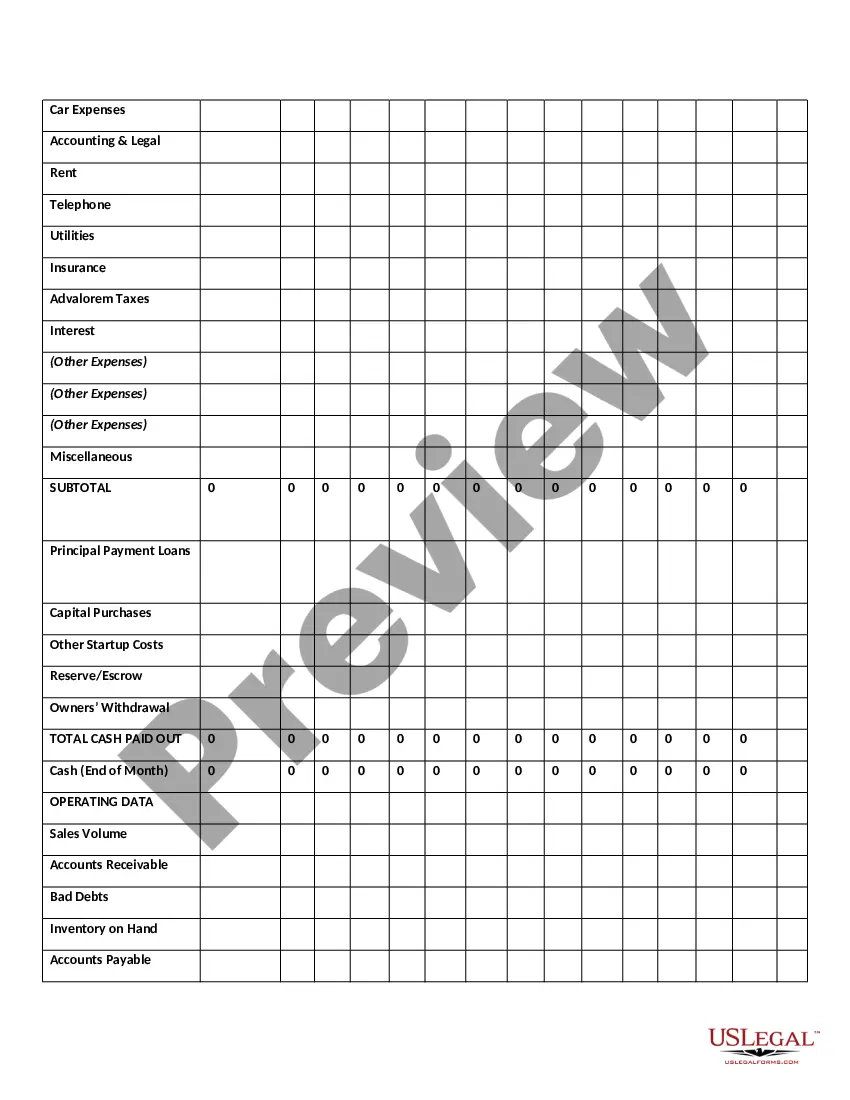

Idaho Twelve-Month Cash Flow is a financial statement that provides a detailed overview of the incoming and outgoing funds of a business in the state of Idaho over a twelve-month period. This financial document plays a crucial role in determining the financial stability and profitability of a business, helping entrepreneurs make informed decisions regarding budgeting, investment, and expansion strategies. Keywords: Idaho, twelve-month cash flow, financial statement, incoming funds, outgoing funds, financial stability, profitability, budgeting, investment, expansion strategies. Different types of Idaho Twelve-Month Cash Flow include: 1. Operating Cash Flow: This type of cash flow measures the cash generated or used by the regular operations of the business. It includes the revenue earned from sales, payments received from customers, and expenses related to operational activities such as wages, utilities, and raw materials. 2. Investing Cash Flow: Investing cash flow represents the cash inflows and outflows related to investments made by the business. This includes the purchase and sale of assets, such as property, equipment, stocks, and bonds. 3. Financing Cash Flow: Financing cash flow accounts for the cash inflows and outflows related to financial activities of the business. It includes funds obtained through borrowing, repayment of debt, and issuance or repurchase of company shares. 4. Net Cash Flow: Net cash flow is the difference between the total inflows and outflows of cash during the specified twelve-month period in Idaho. It provides a clear picture of the overall financial health of the business. 5. Positive Cash Flow: Positive cash flow occurs when the total inflows of cash exceed the outflows. This indicates that the business is generating sufficient revenue to cover its expenses and have surplus funds for reinvestment or expansion. 6. Negative Cash Flow: Negative cash flow arises when the outflows of cash surpass the inflows. This indicates that the business is experiencing financial difficulties, relying on external sources or loans to cover its expenses. 7. Projected Cash Flow: Projected cash flow is an estimation of the future cash inflows and outflows based on anticipated sales, expenses, and investments. This forecasting tool helps businesses plan and strategize effectively to achieve their financial goals. In conclusion, the Idaho Twelve-Month Cash Flow is a vital financial statement that provides a comprehensive overview of a business's financial activities in the state of Idaho. By considering different types of cash flows, entrepreneurs can analyze their business's performance, identify areas of improvement, and make informed decisions to ensure long-term financial stability and growth.Idaho Twelve-Month Cash Flow is a financial statement that provides a detailed overview of the incoming and outgoing funds of a business in the state of Idaho over a twelve-month period. This financial document plays a crucial role in determining the financial stability and profitability of a business, helping entrepreneurs make informed decisions regarding budgeting, investment, and expansion strategies. Keywords: Idaho, twelve-month cash flow, financial statement, incoming funds, outgoing funds, financial stability, profitability, budgeting, investment, expansion strategies. Different types of Idaho Twelve-Month Cash Flow include: 1. Operating Cash Flow: This type of cash flow measures the cash generated or used by the regular operations of the business. It includes the revenue earned from sales, payments received from customers, and expenses related to operational activities such as wages, utilities, and raw materials. 2. Investing Cash Flow: Investing cash flow represents the cash inflows and outflows related to investments made by the business. This includes the purchase and sale of assets, such as property, equipment, stocks, and bonds. 3. Financing Cash Flow: Financing cash flow accounts for the cash inflows and outflows related to financial activities of the business. It includes funds obtained through borrowing, repayment of debt, and issuance or repurchase of company shares. 4. Net Cash Flow: Net cash flow is the difference between the total inflows and outflows of cash during the specified twelve-month period in Idaho. It provides a clear picture of the overall financial health of the business. 5. Positive Cash Flow: Positive cash flow occurs when the total inflows of cash exceed the outflows. This indicates that the business is generating sufficient revenue to cover its expenses and have surplus funds for reinvestment or expansion. 6. Negative Cash Flow: Negative cash flow arises when the outflows of cash surpass the inflows. This indicates that the business is experiencing financial difficulties, relying on external sources or loans to cover its expenses. 7. Projected Cash Flow: Projected cash flow is an estimation of the future cash inflows and outflows based on anticipated sales, expenses, and investments. This forecasting tool helps businesses plan and strategize effectively to achieve their financial goals. In conclusion, the Idaho Twelve-Month Cash Flow is a vital financial statement that provides a comprehensive overview of a business's financial activities in the state of Idaho. By considering different types of cash flows, entrepreneurs can analyze their business's performance, identify areas of improvement, and make informed decisions to ensure long-term financial stability and growth.