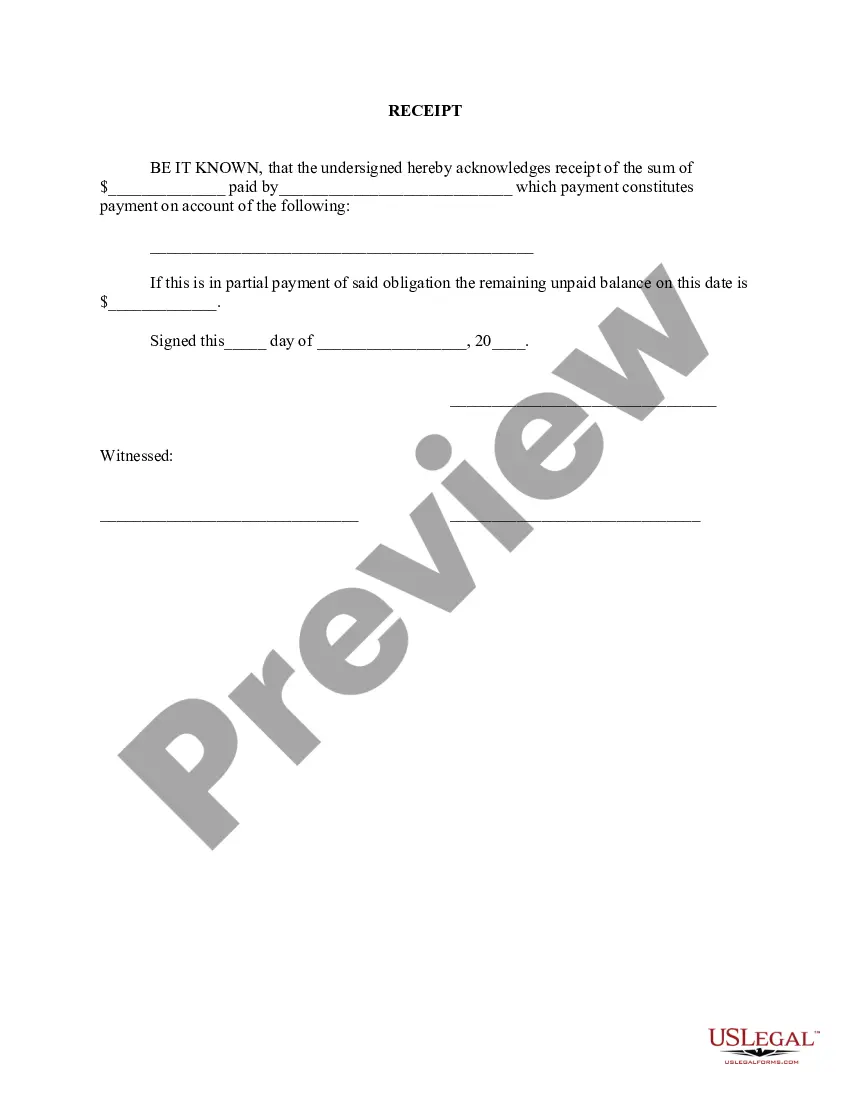

Idaho Receipt for loan Funds

Description

How to fill out Receipt For Loan Funds?

Finding the right lawful file template can be quite a struggle. Naturally, there are a lot of templates available online, but how can you get the lawful develop you need? Use the US Legal Forms internet site. The assistance gives 1000s of templates, such as the Idaho Receipt for loan Funds, which can be used for company and private needs. Each of the varieties are checked out by experts and meet up with federal and state requirements.

If you are presently signed up, log in in your accounts and click on the Acquire button to find the Idaho Receipt for loan Funds. Use your accounts to look throughout the lawful varieties you may have purchased earlier. Go to the My Forms tab of your accounts and have another version of your file you need.

If you are a whole new user of US Legal Forms, allow me to share easy recommendations that you can stick to:

- First, make sure you have selected the proper develop for your metropolis/area. It is possible to examine the form while using Review button and browse the form description to ensure this is basically the right one for you.

- In case the develop fails to meet up with your preferences, take advantage of the Seach field to discover the right develop.

- Once you are sure that the form would work, click on the Purchase now button to find the develop.

- Choose the costs prepare you need and type in the required info. Build your accounts and purchase your order making use of your PayPal accounts or credit card.

- Opt for the data file formatting and obtain the lawful file template in your gadget.

- Complete, change and produce and signal the received Idaho Receipt for loan Funds.

US Legal Forms is the largest catalogue of lawful varieties where you can discover various file templates. Use the company to obtain professionally-produced papers that stick to express requirements.

Form popularity

FAQ

Idaho Statutes 49-911. Visibility of reflectors, clearance lamps, and marker lamps.

(1) Every motor vehicle, trailer, semitrailer, and pole trailer, and any other vehicle which is being drawn at the end of a train of vehicles, shall be equipped with at least one (1) tail lamp mounted on the rear, which when lighted as required, shall emit a red light plainly visible from a distance of five hundred ( ...

(1) Every farm tractor and every self-propelled farm equipment unit or implement of husbandry not equipped with an electric lighting system shall at all times specified in section 49-903, Idaho Code, be equipped with at least one (1) lamp displaying a white light visible from a distance of not less than five hundred ( ...

(1) Every school bus shall, in addition to any other equipment and distinctive markings required by this title, be equipped with signal lamps mounted as high and as widely spaced laterally as practicable, which shall display to the front two (2) alternately flashing red lights located at the same level and to the rear ...

Reckless Driving § 49-1401(1). Essentially, if you are driving too fast and/or the officer thinks you are doing something dangerous, you can be charged with reckless driving. Reckless driving is a misdemeanor that carries a maximum sentence of six months in jail and a $1,000 fine.

(1) Any motor vehicle may be equipped and when required under this chapter shall be equipped with stop lamps on the rear of the vehicle which shall display a red or amber light, or any shade of color between red and amber, visible from a distance of not less than one hundred (100) feet to the rear in normal sunlight, ...

With the implementation of §49-303A Idaho Code, the driver license and/or privileges of minors under the age of 18 years may be suspended if he/she drops out of school. The minor may be reinstated at any time after he/she is once again in compliance and has paid the required reinstatement fee.

(1) The application of any person under the age of eighteen (18) years for any class D instruction permit, restricted driver's license, restricted school attendance driving permit, driver training instruction permit or driver's license shall be signed and verified before a person authorized to administer oaths by ...