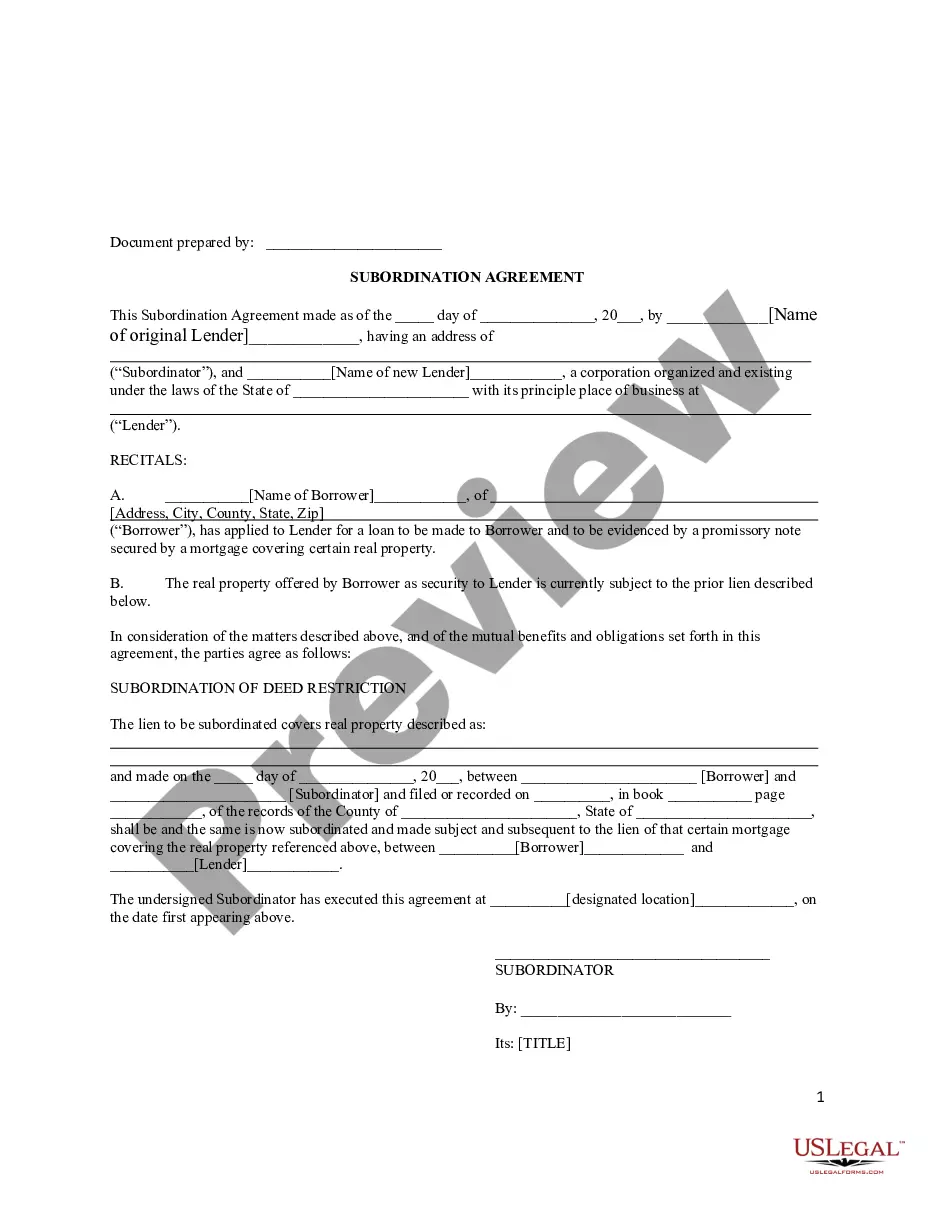

Idaho Subordination Agreement Subordinating Existing Mortgage to New Mortgage

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Subordination Agreement Subordinating Existing Mortgage To New Mortgage?

Choosing the best authorized papers design can be quite a have a problem. Obviously, there are a lot of layouts available on the Internet, but how can you get the authorized form you want? Make use of the US Legal Forms site. The assistance offers a large number of layouts, such as the Idaho Subordination Agreement Subordinating Existing Mortgage to New Mortgage, which can be used for enterprise and personal demands. All of the kinds are inspected by professionals and satisfy state and federal specifications.

If you are previously authorized, log in to your bank account and click on the Down load option to find the Idaho Subordination Agreement Subordinating Existing Mortgage to New Mortgage. Make use of your bank account to search throughout the authorized kinds you possess purchased previously. Visit the My Forms tab of the bank account and get yet another version of your papers you want.

If you are a whole new end user of US Legal Forms, listed below are easy guidelines so that you can follow:

- Initial, make certain you have selected the right form to your city/state. You are able to look over the form utilizing the Preview option and browse the form explanation to make sure this is the right one for you.

- In the event the form will not satisfy your requirements, utilize the Seach discipline to get the correct form.

- Once you are certain that the form is suitable, click on the Purchase now option to find the form.

- Choose the rates strategy you need and enter in the required info. Design your bank account and pay money for the transaction utilizing your PayPal bank account or Visa or Mastercard.

- Choose the submit file format and acquire the authorized papers design to your product.

- Complete, modify and print out and signal the obtained Idaho Subordination Agreement Subordinating Existing Mortgage to New Mortgage.

US Legal Forms is the greatest local library of authorized kinds for which you can find various papers layouts. Make use of the service to acquire skillfully-manufactured documents that follow state specifications.

Form popularity

FAQ

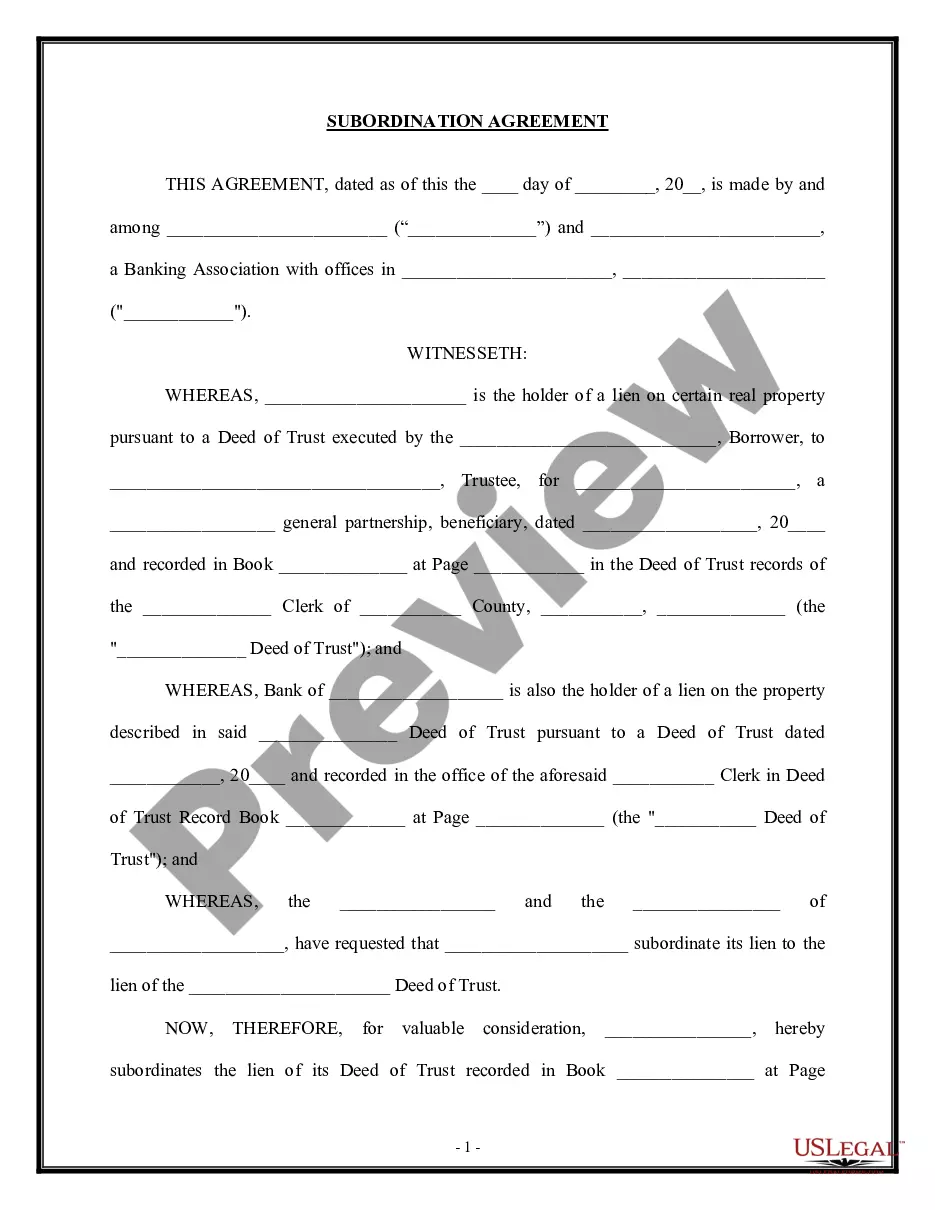

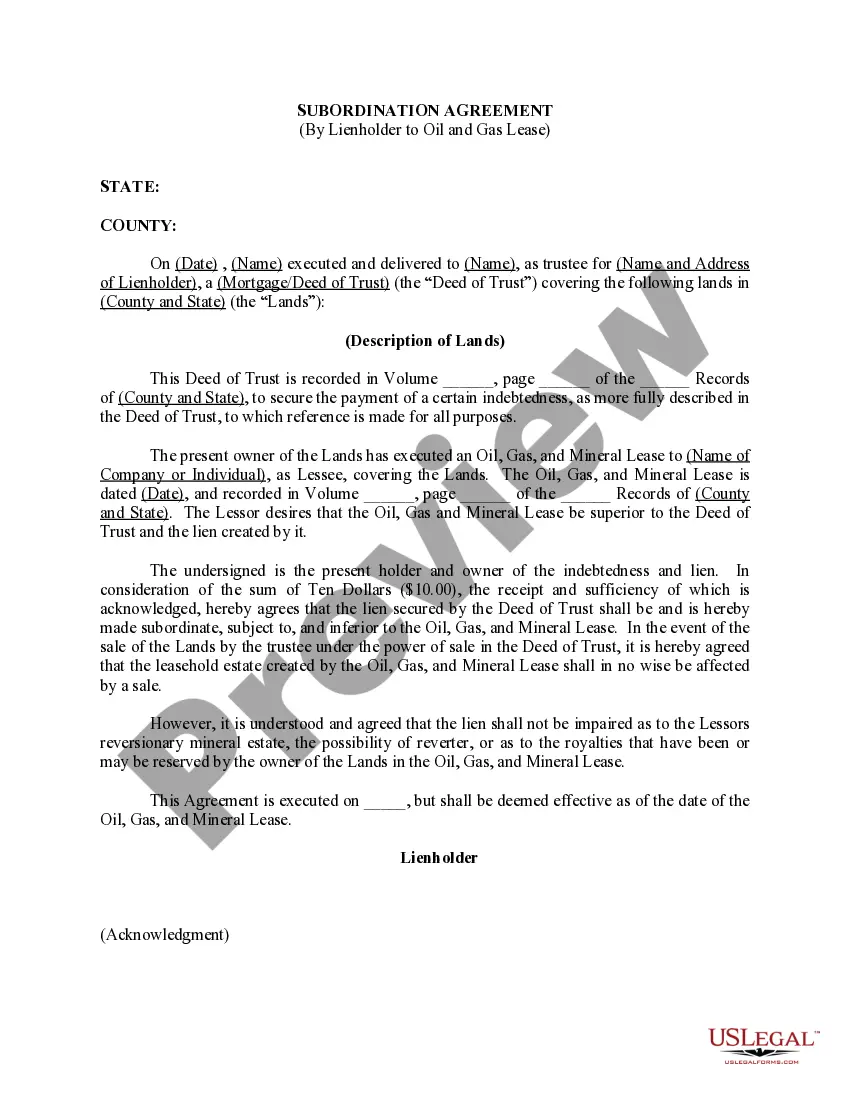

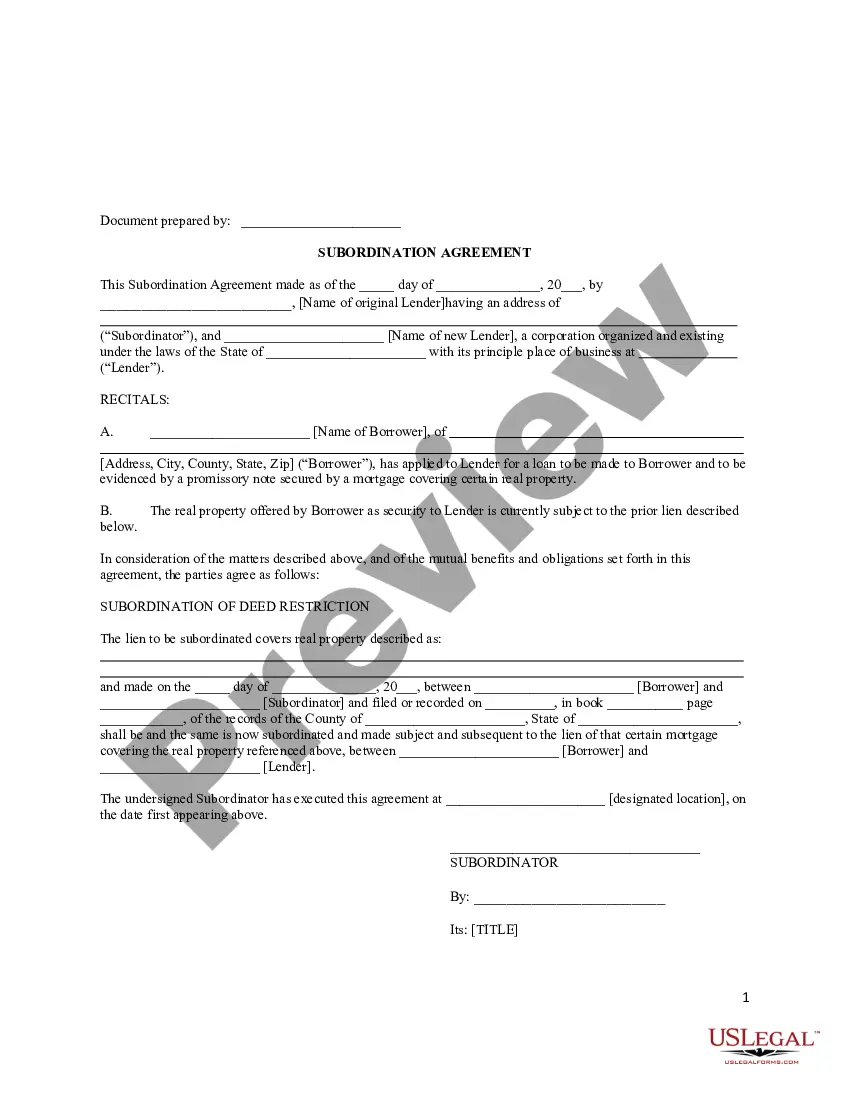

Example of a Subordination Agreement A standard subordination agreement covers property owners that take a second mortgage against a property. One loan becomes the subordinated debt, and the other becomes (or remains) the senior debt. Senior debt has higher claim priority than junior debt.

Getting A Second Mortgage A second mortgage will become a subordinate loan. If you repay the primary loan within the term of the second mortgage, the second mortgage can take its place as the primary loan.

Subordination is the act or process by which one person or creditor's rights or claims are ranked below those of others, dealing with the distribution priority of debts between creditors.

A subordination agreement must be signed and acknowledged by a notary and recorded in the official records of the county to be enforceable.

Subordination is a way of changing the priority of claims against a debtor so that one creditor or group of creditors (the junior creditor(s)) agree that their debt will not be paid until debts owed to another creditor or group of creditors (the senior creditor(s)) have been paid.

The creditor usually will require the debtor to sign a subordination agreement which ensures they get paid before other creditors, ensuring they are not taking on high risks.

Again, if you're refinancing your first mortgage and the property also has a subordinate mortgage, the refinancing lender will usually handle the process of getting the necessary subordination agreement. But you need to ensure that the required subordination agreement is completed before the new loan's closing date.

Many people have a subordinate mortgage in the form of a home equity line of credit or home equity loan. A subordinate mortgage is secured by your property but sits in second position, if you have a primary mortgage, for getting paid in the event you default.