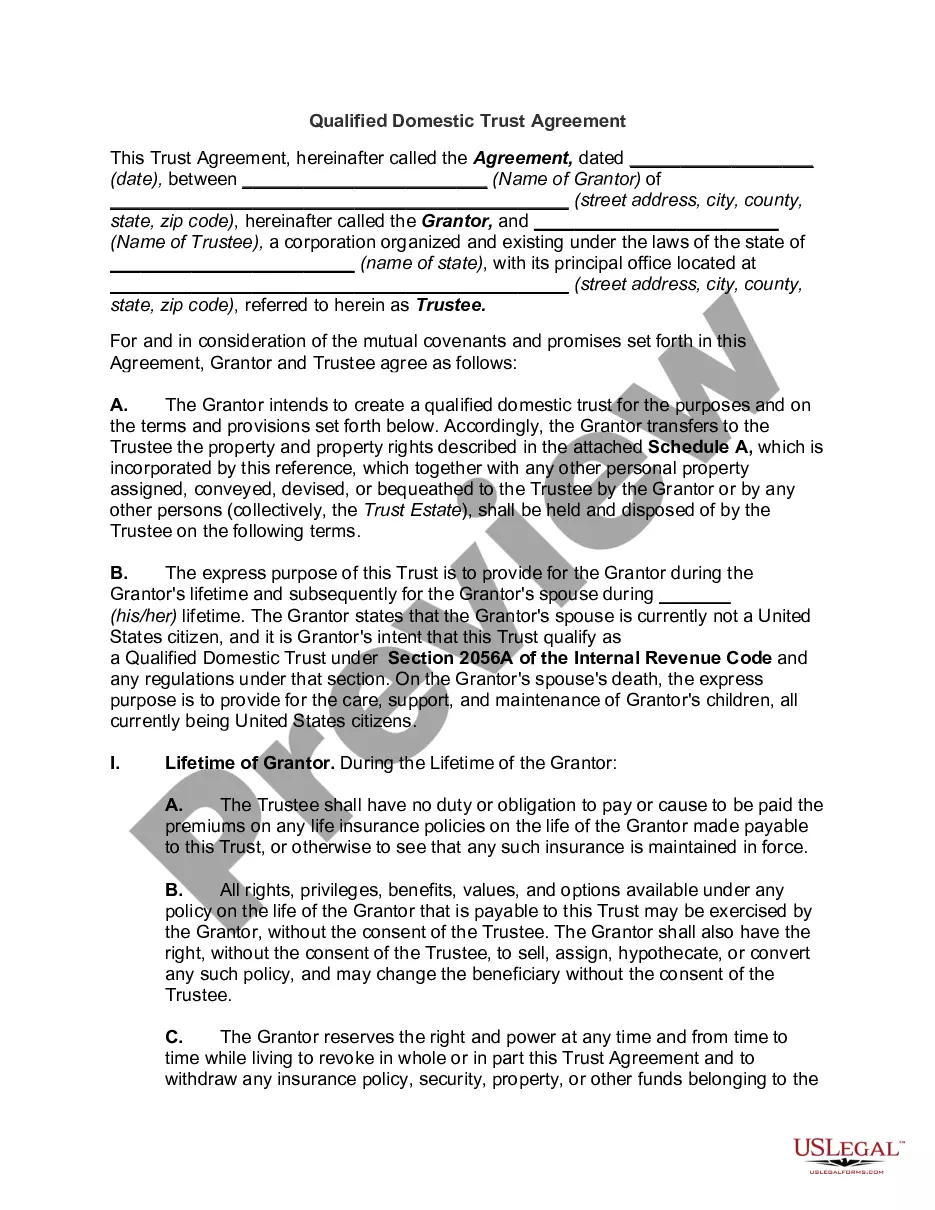

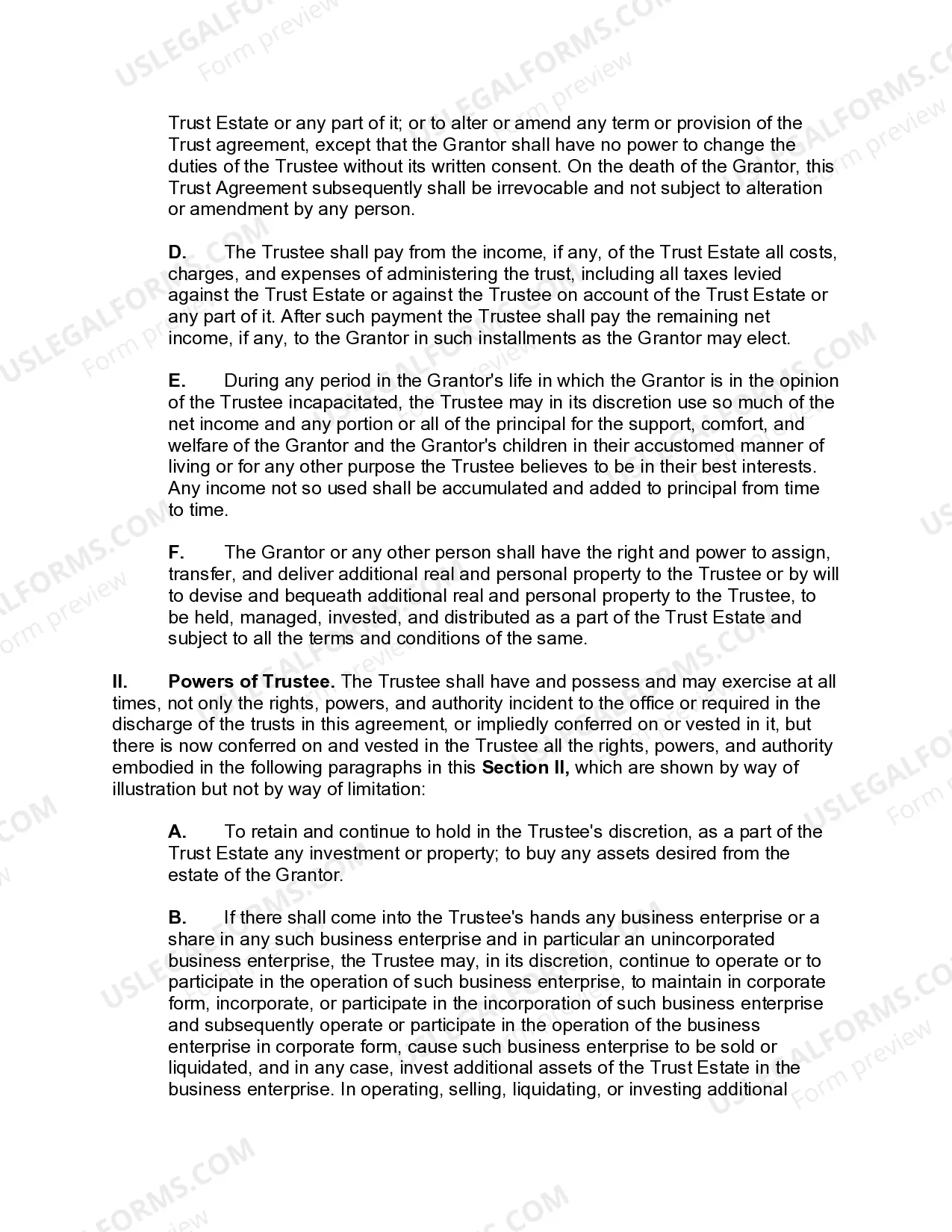

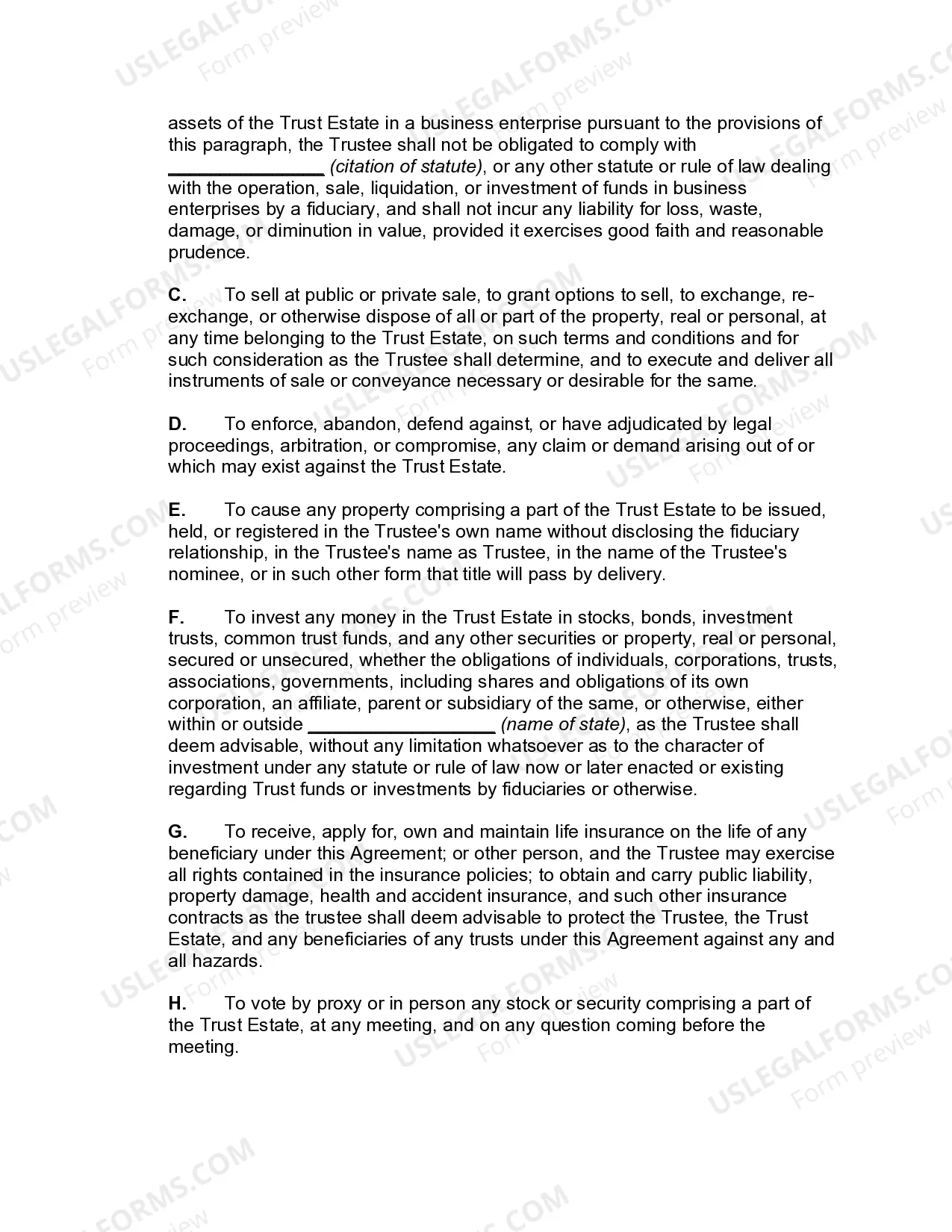

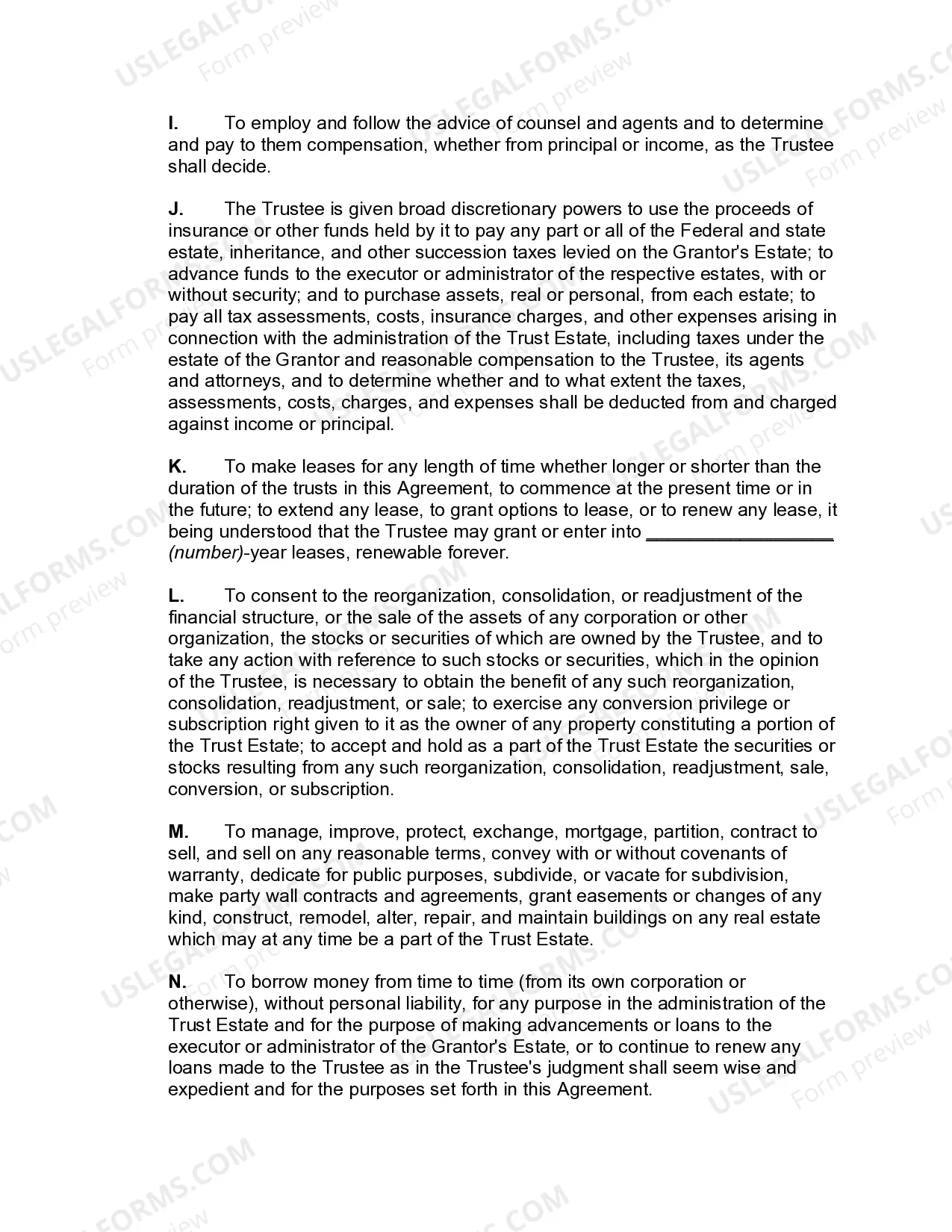

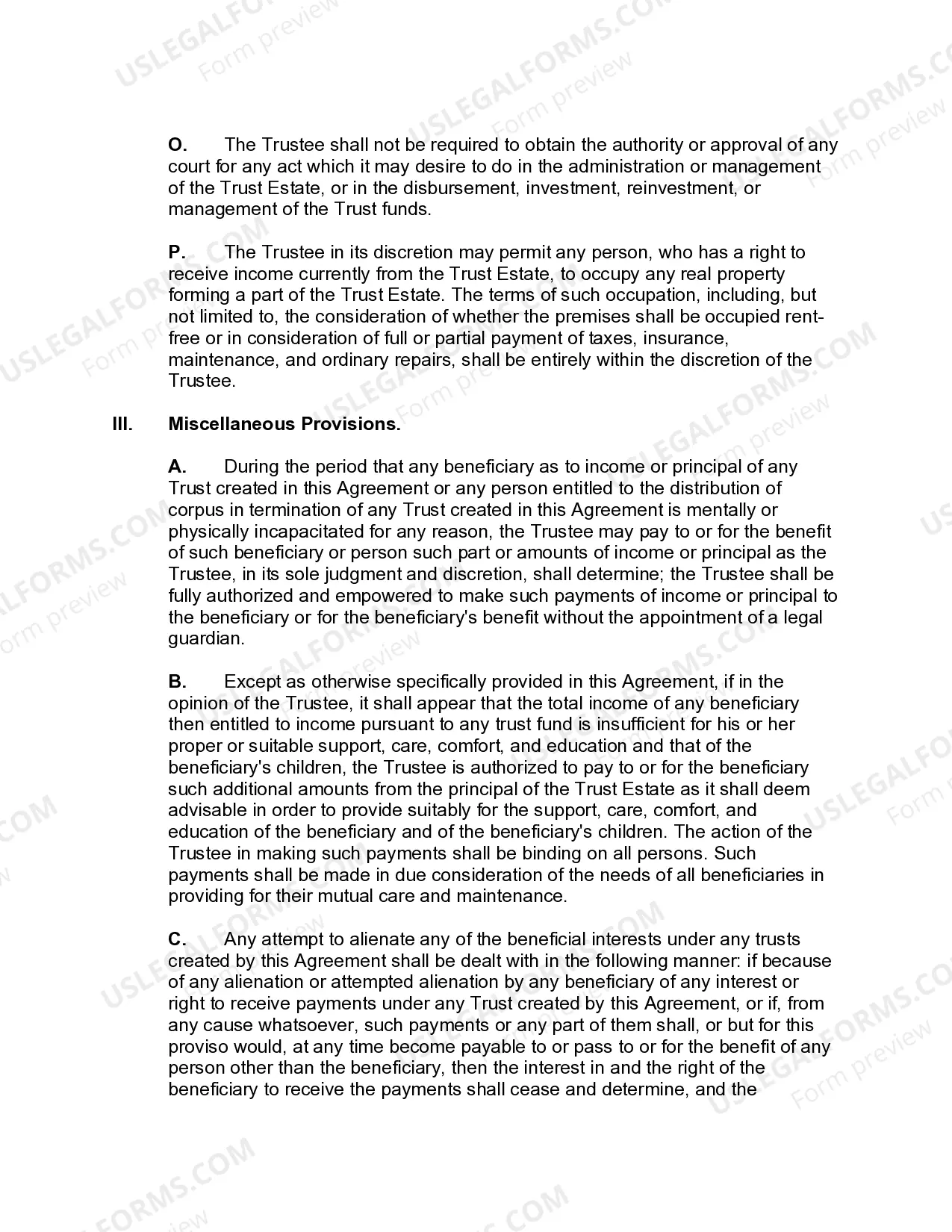

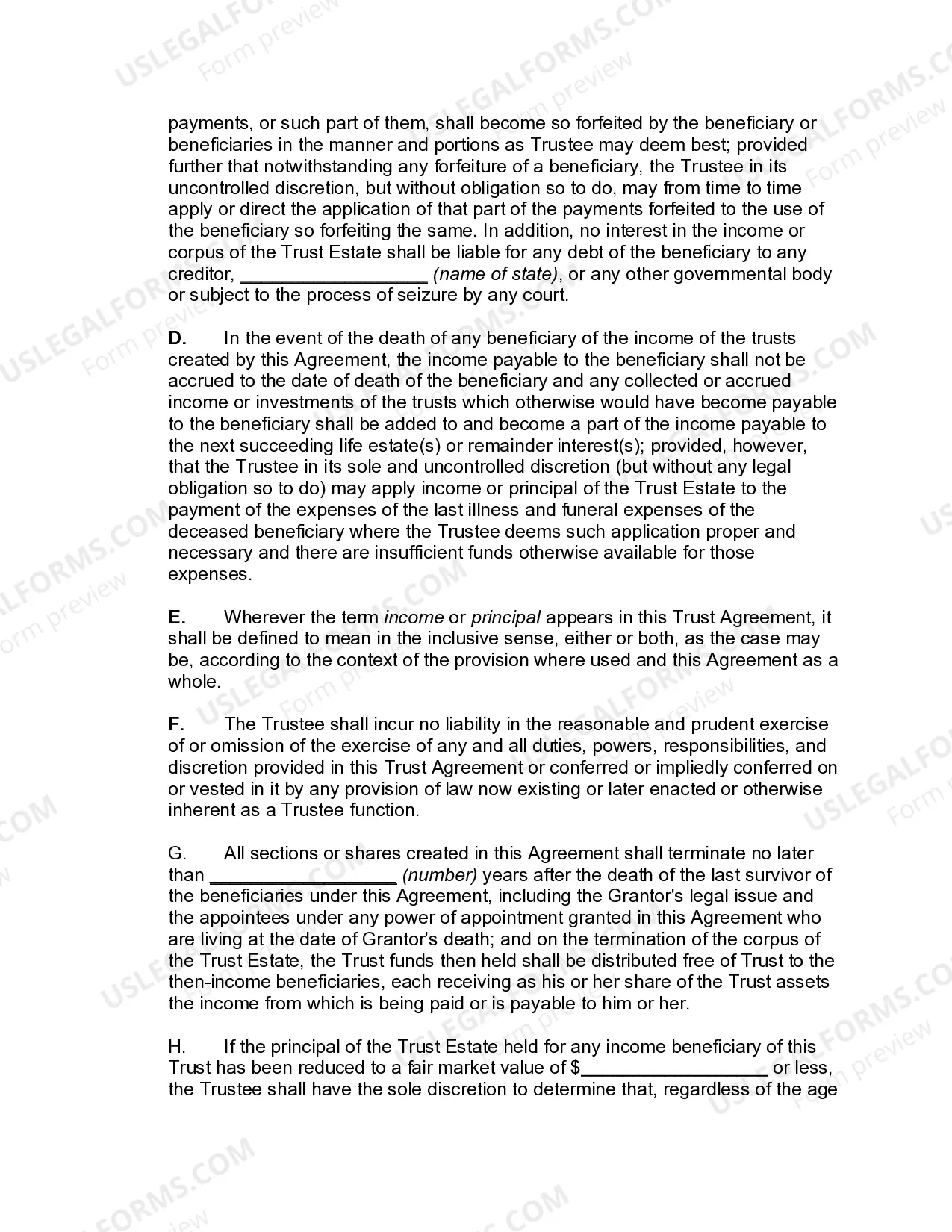

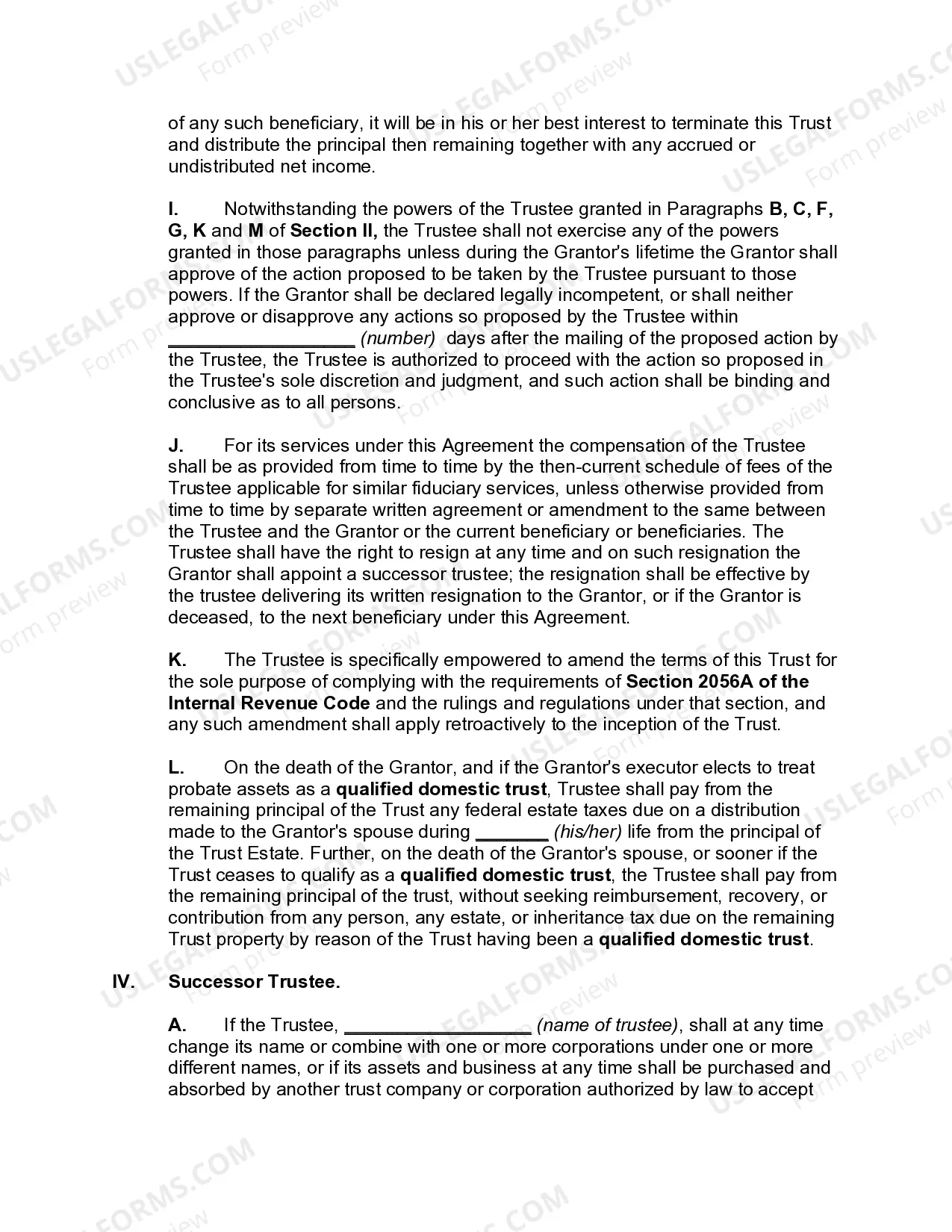

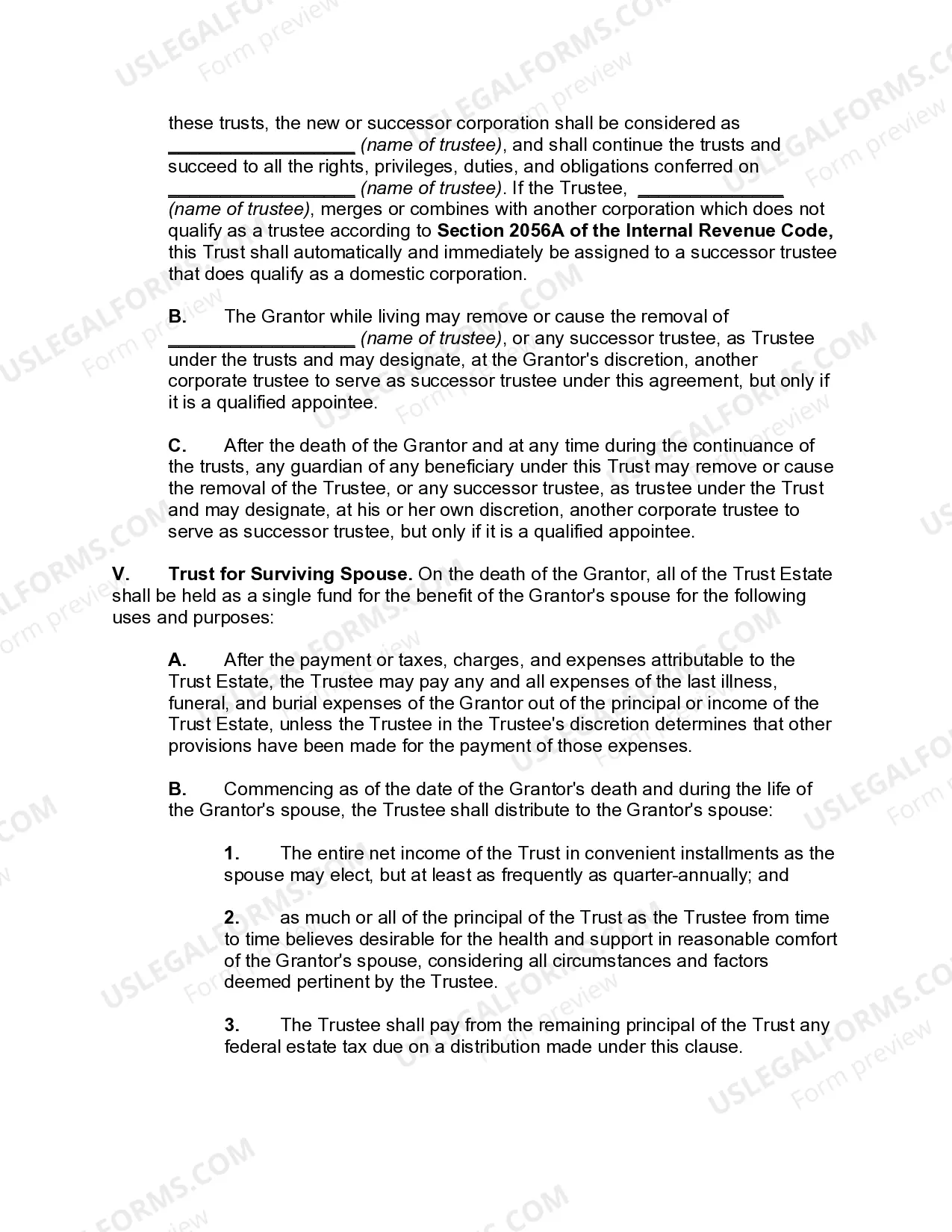

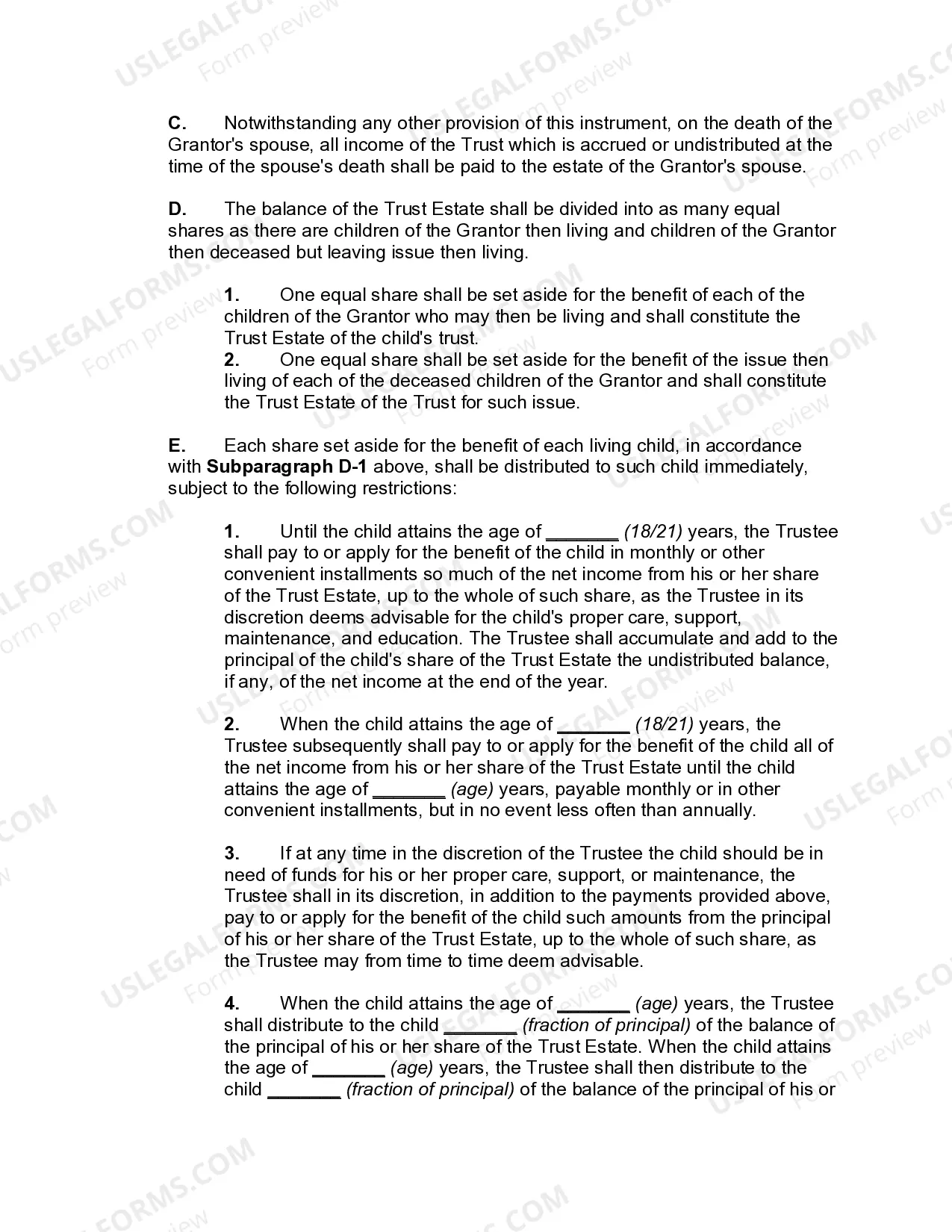

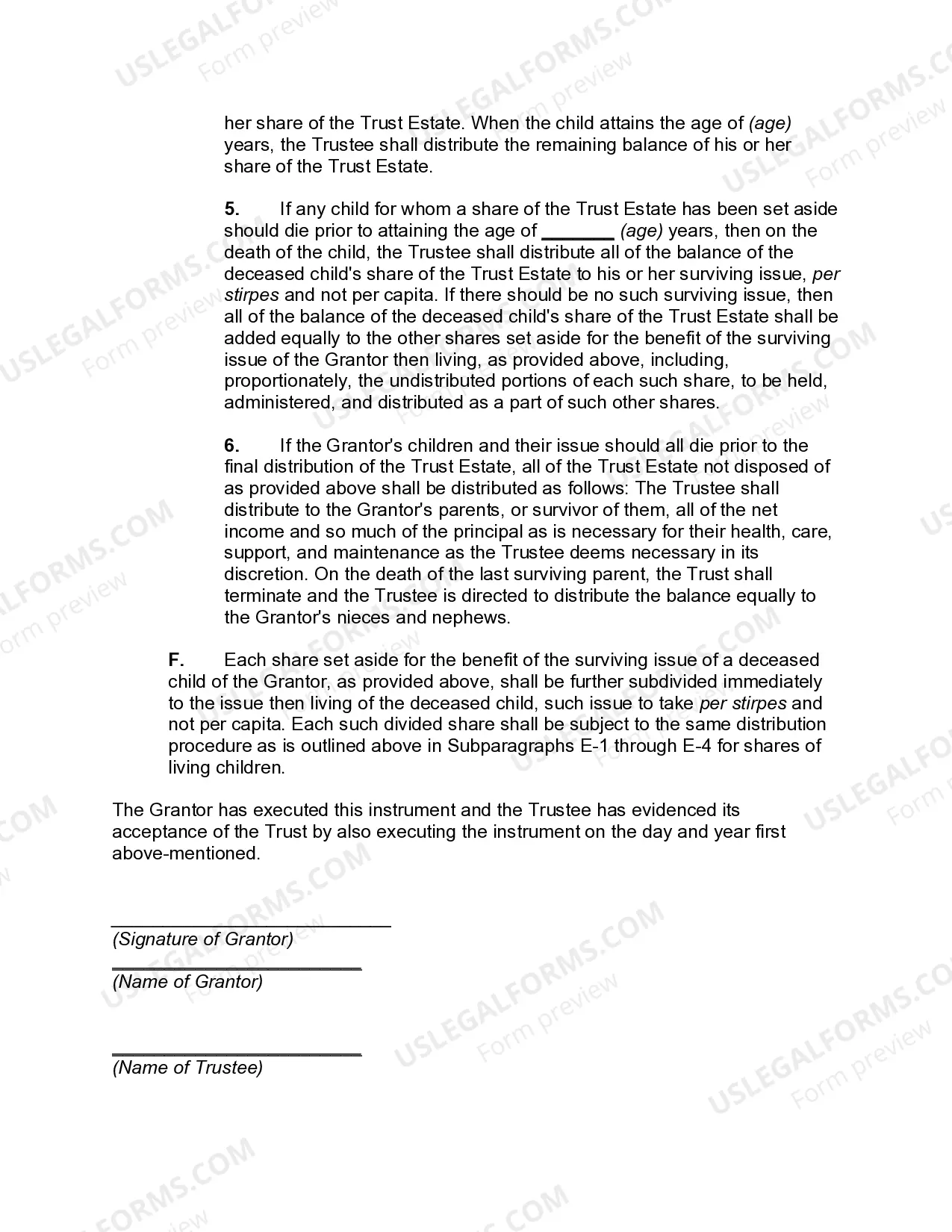

Idaho Qualified Domestic Trust Agreement, commonly known as an Idaho DOT Agreement, is a legal document used to facilitate the transfer of assets from a non-U.S. citizen to a Qualified Domestic Trust (DOT) in Idaho. A DOT is a special type of trust designed to ensure estate tax benefits for non-U.S. citizen spouses who inherit assets from their U.S. citizen spouses. The Internal Revenue Service (IRS) imposes certain restrictions and requirements on Dots to prevent the avoidance of estate taxes. Under a typical Idaho DOT Agreement, several important elements are included: 1. Granter: The party creating the DOT is known as the granter, who is usually the U.S. citizen spouse. 2. Trustee: A trustee is designated to manage the DOT and fulfill the legal requirements. The trustee can be an individual or a corporate entity. 3. Non-U.S. Citizen Spouse: The DOT is established primarily for the benefit of the non-U.S. citizen spouse, who will receive the income generated by the trust. 4. Estate Tax Planning: The primary purpose of an Idaho DOT Agreement is to minimize estate taxes. With proper planning, the assets transferred to the DOT are not subject to immediate estate taxes upon the U.S. citizen spouse's death. 5. Required Annual Distribution: The Idaho DOT Agreement must ensure that at least one trustee is a U.S. citizen or domestic corporation. It also mandates that the trust provides an annual distribution of income to the non-U.S. citizen spouse. 6. Estate Tax Liability: If the non-U.S. citizen spouse were to pass away, any remaining assets in the DOT would be subject to estate taxes. This is to prevent the assets from leaving the U.S. tax jurisdiction. In Idaho, there are no specific variations or different types of DOT agreements beyond the general DOT requirements set by the IRS. However, the specific terms and conditions of an Idaho DOT Agreement can be customized based on the unique needs and circumstances of the individuals involved. To summarize, an Idaho Qualified Domestic Trust Agreement is a legal tool used for estate tax planning purposes, providing benefits and protection for non-U.S. citizen spouses inheriting assets from U.S. citizens. By complying with the requirements of a DOT, individuals can manage their estate planning in a manner that ensures the preservation of assets and minimizes tax liabilities.

Idaho Qualified Domestic Trust Agreement

Description

How to fill out Idaho Qualified Domestic Trust Agreement?

Choosing the right legitimate file format can be quite a struggle. Needless to say, there are plenty of themes available on the net, but how do you find the legitimate kind you want? Use the US Legal Forms site. The support offers a huge number of themes, including the Idaho Qualified Domestic Trust Agreement, that can be used for enterprise and personal requirements. All of the types are inspected by pros and satisfy state and federal demands.

Should you be currently authorized, log in in your bank account and click on the Download switch to get the Idaho Qualified Domestic Trust Agreement. Make use of your bank account to appear through the legitimate types you possess bought formerly. Check out the My Forms tab of the bank account and get one more version from the file you want.

Should you be a new consumer of US Legal Forms, allow me to share basic recommendations for you to comply with:

- Initially, make sure you have selected the right kind for your personal metropolis/region. You may look through the form utilizing the Review switch and study the form outline to make sure this is basically the best for you.

- In case the kind will not satisfy your preferences, take advantage of the Seach industry to get the correct kind.

- When you are sure that the form is proper, click on the Buy now switch to get the kind.

- Choose the costs prepare you need and type in the essential details. Make your bank account and buy your order using your PayPal bank account or credit card.

- Pick the data file file format and down load the legitimate file format in your device.

- Comprehensive, revise and produce and sign the received Idaho Qualified Domestic Trust Agreement.

US Legal Forms will be the largest library of legitimate types for which you will find numerous file themes. Use the service to down load professionally-created paperwork that comply with condition demands.